Consultation Paper on Revisions to the ITS on supervisory reporting (Commission Implementing Regulation (EU) 2024/3117) - Module on liquidity and asset encumbrance

The content on these interactive pages is provided for ease of reference and to assist in the reading and understanding of the Consultation Paper and it is not considered as the official version of such documents.

For the formal consultation papers and their components, please refer to the .pdf documents provided at the bottom of this page. In case of discrepancies between these interactive pages and the .pdf documents, the latter prevail as the authentic official versions.

Responding to this consultationPlease provide your responses by 10 July 2026 at 23:59 CEST via EU survey (Password for the survey: Reporting2026). Late responses will not be considered. |

1.Background and rationale

1.1 Objectives and underlying context for the proposed amendments to Liquidity and Asset encumbrance reporting

- The proposal for amending the current reporting frameworks with respect to Additional liquidity monitoring metrics (ALMM) and Asset Encumbrance (AE) templates is driven by a series of identified needs and factual evidence derived from supervisory lessons learned in recent years and market developments.

- The 2023 events and market turmoil have highlighted the need to collect additional/more frequent information to analyse the liquidity situation of EEA institutions and cope with the complexity of the macroeconomic environment. In this context the EBA engaged to assess further the need to amend/complement the existing regulatory reporting as already pre-empted in the EBA reports on the LCR and NSFR implementation in EU[1].

- Currently there are series of non-ITS data collections at national level that are mature and stable enough to benefit from integration and harmonisation at EEA level. A proliferation of different liquidity templates across different countries originates from the attempts to address needs not covered by the ITS (e.g. ECB, NCAs, JSTs and SRB are currently requiring banks to report additional liquidity data, on top of the ITS, following different frequencies (from daily to yearly), different formats (very heterogeneous templates, sometimes asking for ITS-like data) and under different reporting assumptions.

- Empirical evidence from ad-hoc collections run at national level by several supervisory authorities (e.g. the SSM weekly liquidity data collection, IT, AT) have showed that a higher reporting frequency allows supervisors to gather valuable insights on the liquidity profile and vulnerabilities of supervised institutions, relevant for both ongoing supervision and potential stress situations; necessary data to monitor a fast-moving risk like liquidity, both in terms of frequency and content.

- In striking the balance between the need for simplification and the supervisory needs, the current ITS has been reviewed and further integrated, leading to a streamlining of the reporting requirements. The existing templates on - Asset Encumbrance (AE), ALMM and LCR - have been scrutinised in terms of “must have” and “nice to have” data. In particular, the “least used templates” identified already in the Cost of Compliance report of the EBA have been analysed and proposals for streamlining and decommissioning have been made, following the report’s Recommendation number 14.

- While LCR and NSFR reporting are supporting supervisors to monitor institutions’ compliance with the prudential requirements, the ALMM and AE reporting frameworks have been considered to allow for the right format to implement the identified needs of the authorities in terms of data and liquidity analysis. As it will be explained in the next sections, the EBA has considered various options to integrate the data needs of supervisors into the current reporting frameworks and has balanced costs and benefits in coming up with the current proposals which are now put for consultation to better understand the feasibility of the proposal and get a clearer view on the costs and benefits.

- The EBA has always aimed at fostering a regulatory framework that is proportionate, effective and efficient while ensuring that the supervisory authorities will have access to data on a “need to have” basis to fulfil their mandates. The amendments proposed in this draft ITS have been developed with this in mind.

1.2 Proportionality, relevance and facilitation of institution’s compliance

- The EBA has always aimed at fostering a regulatory framework that is proportionate and efficient while ensuring that the supervisory authorities will have access to data on a “need to have” basis to fulfil their mandates. The amendments proposed in this draft ITS have been developed keeping in mind:

- The maintenance of a proportional reporting framework: proportionality with respect to the size of the institutions (Large, Medium (other than large and SNCI) and SNCI) already present in the ALMM and AE reporting is maintained and enhanced[2]. Some of the additional data needs identified: such as more granularity of downgrade triggers, behavioural information, enhanced reporting on counterparties is targeting just Large Institutions.

- Maintenance of a relevant reporting framework: most of the amendments proposed reflect lessons learned from the supervisors’ experience with the currently reported data in analysing the liquidity position of institutions and in addition reflect additional data needs coming from market developments. This ensures that the reporting framework to assess institution’s liquidity position remains relevant.

- The full set of information proposed for amendments by competent and resolution authorities was scrutinised and reduced to ensure only the “need to have” data points are included in the reporting requirements. A series of templates and data points have been eliminated or streamlined providing further guidance in the instructions.

- Facilitate institution’s compliance: explanations and reporting examples to clarify and support a uniform understanding of the reporting expectations have been provided as well as guidance on data lineage between Asset Encumbrance templates on assets and collateral received and the counterbalancing capacity section of the ALMM. In addition, a series of existing Q&As have been reviewed and guidance has been reflected directly in the instructions; the definition of concepts used across ALMM and AE frameworks has been clarified and aligned.

Least used templates and scrutiny of data use

- In the EBA’s Cost of Compliance Study[3], a series of templates from the Asset encumbrance and Additional liquidity monitoring metrics frameworks have been identified as “least used templates” – defined as templates that are very burdensome to be produced by institutions and may be less used on the authority’s side. Recommendation 14 requires the “Review of the scope of application, the reporting frequency and/ or the content of the reporting requirements identified as least important and least frequently used by data recipients”.

- Since 2023, the ALMM and AE reporting frameworks are reported with enhanced proportionality[4]. In the current review of the ITS, further scrutiny on the data usage was performed, resulting in a series of simplifying measures:

- Supervisor’s experience with using Template C 70.00 Roll-over of funding, has been very limited in terms of analysis performed. For this reason, it is proposed that this template should be discontinued.

- Given the proposed changes to the AE framework, some of the information currently covered in F 32.03 will be redundant while the rest of the information is not seen as a “need to have” for supervisors. It is proposed that this template should be discontinued.

- Template F 34.00 (contingent encumbrance) has been of limited use to supervisors, given its complexity to be filled in and the hypothetical nature of the information, making it difficult for authorities to assess its accuracy and draw conclusions on the information sent. It is therefore proposed to be discontinued.

- The Cost of compliance study also identified F 33.00 (maturity data) and F 35.00 (covered bonds issuances) to be part of the “least used” templates. Authorities have closely reassessed the rational of having these templates and their use in practice and have concluded that they should be kept for medium and large institutions, while for SNCIs it is proposed that they are exempted from reporting F 35.00 template.

- In particular F 33 (maturity data) template:

- It is highly valuable for controlling collateral availability and analysing the refinancing capability of banks.

- It is useful to have an assessment about the maturity of encumbered assets for having a better understanding of the Credit Institutions strategy in funding.

- The evolution of the maturity data can provide information about the credit institutions’ maturity transformation and the management of the asset side of the balance sheet. This information cannot be found elsewhere.

- In particular F 35 (covered bonds issuances) template:

- It is very important for the analysis and monitoring of such instruments (in many cases it is complemented with further details at national level).

- It is used to assess compliance with Article 129 of the CRR and perform impact assessments (e.g. respond to COMM’s call for advice (CFA) on the EU covered bond framework)

- Given the peculiarity of these instruments in the EU, and their relative novelty in Europe, this template is deemed very relevant

- Additional proposals are put forward for simplification in the area of liquidity and Asset encumbrance, balancing the costs and benefits of reporting this data. The objective is to reduce the reporting burden to institutions while at the same time making sure authorities have the minimum necessary data to fulfil their mandates:

- On the LCR, the template that is targeted for simplification is template C 75.01 on Collateral swaps. The proposal for simplification is to exempt: SNCI from reporting this template and for Large and Medium-sized institutions, introduce a quarterly reporting as opposed to monthly and no reporting in significant currency. To note that the changes to reporting are with no prejudice to the correct calculation of the LCR, in line with the regulation.

- exemption of SNCI from reporting C 71.00 template;

- exemption of medium-sized institutions from reporting template C 69.00;

- exempting SNCI from reporting templates F 32.04. as a result, SNCIs would only report the F 32.11 and F 32.12 templates from the AE module;

- exempt medium-sized institutions from reporting F 36 templates

- As part of the ongoing simplification efforts aimed at reducing reporting burden and implementation costs, with respect to template C 67.00 institutions that are SNCIs are invited to provide feedback on (i) the costs associated with implementing the proposed changes to the template, (ii) the costs if the data would be requested instead outside of supervisory reporting by supervisors when needed, (iii) any challenges linked to its production, and (iv) alternative sources from which the underlying information could be reliably retrieved.

- In addition to the least used templates and other burden reduction and proportionality proposals mentioned above, other information from the existing templates is proposed to be discontinued, as explained in the amendments for each template. Such information was deemed not to fulfil the “need to have” criteria.

Simplification - discontinuation of national ad-hoc collections with a “regular nature”

- A series of non-ITS collections (ad-hoc collections with “regular nature”) have been developed by some authorities, requesting information on behavioural flows, such as, for instance, by Italy, Austria, Ireland and SSM.

- With the proposal for the development of an EU level template to capture the behavioural flows (e.g see proposed information covered in C 66.02 template), authorities’ needs for the ad-hoc national data collections will be reassessed, with a view of reducing the reporting burden to the institutions, avoid duplications and redundancy.

- In addition, as a result of limitations in the current AE ITS template, SSM and other National Competent Authorities have, over the years, developed their own collateral templates to address the gaps not covered by the ITS AE template (and to receive the data at higher frequency: weekly or daily). Such collections should be decommissioned and/or simplified following the implementation of the changes proposed in the AE framework.

- The development of EU level templates would support the principle of maximum harmonisation and simplification, reducing the burden for the institutions by the discontinuation of the ad-hoc collections with “regular nature”, providing for transparency, comparability and standardisation of the data to be reported.

Points for semantic integration – concept’s definitions

- The draft ITS has been revised to ensure concepts are semantically integrated and uniquely defined, trying as much as possible to align definitions and avoid redundancies stemming from unjustified “similar but not the same definitions” concepts.

- To offer clarity to the institutions a stock take of concepts used across ALMM and AE frameworks was conducted. As part of the process, some needed improvements (missing definitions, same definition but different wording) have been identified, and concepts have been assessed for possible alignment.

- As a way forward the instructions of ALMM and AE have been amended and a list of concepts used in these frameworks and their definition has been provided in the form of a table in the ALMM instructions. The same table is referenced in the AE instructions. Wherever such concepts are to be used in the ALMM and AE framework, they should be understood within the meaning indicated in the table while the repetition of these definitions at the level of rows/columns was deleted.

- While it is not yet covering all concepts, this table of concepts and associated definitions represents a good starting point for ensuring concepts will be unambiguously uniquely defined across frameworks in the future, with further enhancement of this list to be done in a progressive manner and alignment between ALMM and AE concepts and other supervisory and resolution reporting, where needed, to be done once those other frameworks will be amended.

- The overview of concepts and their definition was not meant to change the meaning of those concepts used so far in reporting, but to ensure their definitions are clear and aligned in wording everywhere where they are used in ALMM and AE. However, some more complex cases have been identified, and definitions were considered for alignment (e.g. definition of deposits).

Revision of Q&As and improvements to reporting instructions

- The EBA Single Rulebook Q&A tool allows institutions, supervisors, and other stakeholders to request clarifications on CRR/CRD requirements, including liquidity and asset‑encumbrance reporting. With the current ITS revision, the EBA streamlined and simplified reporting instructions to improve clarity and reduce ambiguity, incorporating guidance from previous Q&As and adjusting it where needed. Embedding these clarifications directly into the framework reduces reliance on ad‑hoc interpretations and supports more consistent and accurate reporting across the EU.

- The revised Q&As will be archived once the amended ITS enters into force. The annex to this report lists the Q&As affected and the proposed way forward (Section: Overview of revised Q&As).

1.3 Supervisors’ need for more frequent information to assess the liquidity risks

- Unlike other risks a bank faces, liquidity risk is considered a fast-paced one because it can escalate rapidly, often in response to market sentiment or external shocks. Additionally, in today's interconnected financial markets, liquidity issues can spread swiftly from one institution to another, leading to systemic risks. The speed at which liquidity crises can unfold necessitates that banks continuously monitor their liquidity positions and have robust contingency plans in place to respond to sudden changes in their liquidity needs. Similarly, supervisors need access to information to ensure institution’s act accordingly.

- “The banking turmoil of March-May 2023 was the most significant system-wide banking stress since the Great Financial Crisis in terms of scale and scope”[5]. In response to the crisis, regulatory bodies emphasized the need for enhanced data collection and analysis to better assess liquidity risks. The events of 2023 demonstrated that timely and accurate data is crucial for authorities to monitor liquidity positions and respond effectively to emerging risks, ensuring the stability of the financial system.

- The need for more frequent data has also been identified and brought into discussion by other groups at international level. The BCBS report to G20 Finance Ministers and Central Bank Governors “The 2023 banking turmoil and liquidity risk: a progress report” emphasizes how “[…] the frequency of monitoring can be increased both during times of stress (for example to daily or even intra-day monitoring) and business as usual times (e.g. weekly liquidity monitoring), given possible negative signalling effects or other challenges of ramping-up reporting requirements in moments of stress”, while “monitoring can leverage on different sources of information and high-frequency da-ta, complementing the normal supervisory reporting”. In particular, the report, by elaborating on the extent to which “the frequency and scope of reporting are important features” concludes that “it should be noted that the Basel monitoring tools could be even more effective where they: (a) are rigorously used by supervisors via the calculation of dedicated indicators; (b) are reported with a higher reporting frequency during BAU for institutions with a structural high-risk liquidity profile; (c) are additionally applied to individual entities of banking groups; …”.

- Past crisis and, more recently, the 2023 market turmoil, highlighted the inadequacy of a monthly and quarterly frequency for fast-moving risks like liquidity. During the turmoil, supervisors faced significant delays in accessing critical liquidity data, forcing them to rely on daily calls with bank treasurers and non-standardized internal reports. Against this background, several Competent Authorities[6] decided to introduce their own liquidity templates at national level to support their needs to monitor the liquidity situation and interact with the institution on a more frequent basis (as opposed to having to wait for up to 50-60 days to receive banks' updated profiles under the current ITS framework).

- This increased frequency has been deemed necessary by several Competent Authorities to monitor rapid changes in liquidity buffers, funding structures, and intra-month funding volatility, enabling a more proactive and forward-looking supervisory approach. These set of more frequent reporting has been proven invaluable in addressing the challenges posed by a rapidly evolving financial landscape, where declining liquidity buffers, the rise of non-bank financial intermediaries, accelerating digitalization, and instant payments create new uncertainties for banks in estimating cashflows and managing central bank reserves. The higher frequency of reporting has provided supervisors with critical tools to effectively monitor and manage risks in several key areas, such as for instance the timely detection of liquidity trends, the composition and evolution of funding concentration, banks’ operational readiness, ability to re-hypothecate collateral, and access to both central bank funding and private markets.

- Nonetheless, the introduction of new ad-hoc reporting has added heterogeneity in the reporting demands faced by institutions across authorities: each following different frequencies (from daily to yearly), different formats (heterogeneous templates, sometimes asking for ITS-like data) and under different reporting assumptions.

- Under Article 104(1)-point j of the Directive 2013/26/EU(CRD), competent authorities have the power to “impose additional or more frequent reporting requirements, including reporting on own funds, liquidity and leverage;”. The EBA has, however, taken note that the current heterogeneous application has led to increased burden to institutions and inefficiencies in the reporting process. Therefore, the EBA has amended the current reporting requirements for ALMM and AE having in mind the authorities’ need for flexibility to request the data needed on a more frequent basis while in the same time benefiting of harmonized and standardized formats, definitions and processes at EEA level.

- In this respect, the proposed amending ITS in the area of ALMM and AE is supporting supervisors in getting access to information on a more frequent basis, while reducing the reporting burden for the industry by means of defining harmonized and standardized information that could be required with a higher frequency ( as allowed under Article 104(1)-point j of the Directive 2013/26/EU(CRD)). The decommissioning of several ad-hoc national reporting will reduce the costs and increase transparency and certainty to both authorities and institutions.

1.4 Resolution authorities need for data to perform liquidity analysis

- Resolution authorities are leveraging on the EBA ITS on reporting to perform their Business as Usual (BaU) analysis with respect to the liquidity situation of the institutions and there is no other regular liquidity specific reporting from the institutions to resolution authorities. Prudential reporting, defined and used by supervisory authorities is also shared and used by resolution authorities (as an example of integrated reporting where the same data collection is used for different means), including the amendments to this draft ITS.

- Resolution authorities however expect to obtain liquidity specific information from institutions in times of crisis, in the run-up to a crisis and for testing exercises that would assess the ability of the banks to submit the data during a crisis. Depending on the nature of the crisis, (for example, in the banking union), data is requested with a daily frequency, with the possibility to request specific data points more frequently, e.g. to be better able to monitor very fast deposit outflows.

- Data needed by resolution authorities in such situations would also likely be different to a certain extent from data needed in BaU conditions.

- While the scope of the data needed for resolution purposes (resolution groups) remains different from the scope needed by supervisory authorities (liquidity sub-groups), and the frequency with which this data is needed would be different, an alignment between the concepts defined when collecting this data with the concepts defined in the draft EBA ITS, where possible, would already provide great benefits to both authorities and institutions by ensuring:

- a common understanding of reporting requirements – standardised definitions for both institutions and among authorities

- lower costs by reusing infrastructure and data analysis

- increased data quality

- Therefore, resolution authorities would be expected to make use of the EBA ITS and reuse concepts as much as possible when setting up their specific collections. Due to the difference in scope between resolution and supervisory authorities, the need for resolution authorities to request data for scopes not defined for the ITS will continue to exist.

1.5 Proposed content amendments to ALMM

- From a format perspective, the 3 annexes referring to the instructions for the ALMM templates have been consolidated into a single document. The annexes remain separated, therefore references to their numbers or points will remain the same, it is only their location into one single document that has changed to simplify the process of reviewing the documents and ensure they can be easily retrieved.

- At the beginning of the document, the overview of concepts defined has been added, as explained in Section Points for semantic integration – concept’s definitions.

C 66.01 - Maturity ladder

- The sections below are detailing on the proposed changes to template C 66.01 and the rationale behind including them:

Additional granularity in the weekly bucket “from 7 to 14 days”

- As the recent financial turmoil revealed, for a fast-moving risk like liquidity a daily view on the liquidity position of the banks is needed to anticipate potential short-term drops. This is even more important during crisis times, when authorities need to forecast the exact point in time when the bank will potentially fail.

- The proposal is to add additional daily buckets to the template, ensuring consistency between the maturity ladder in business-as-usual and in crisis situations, allowing therefore banks to rely on the same template without having to upscale their infrastructures when entering a crisis. In addition, while longer time buckets are also relevant, the core of the supervisor’s analysis focuses on the banks’ liquidity position till 1-year buckets. Therefore, more granular information in the near horizon is deemed very important.

- It is expected that institutions already have this information in their systems to prepare for the current reporting in C 66.01, therefore the effort is considered minimal comparing to the need for this data by supervisors.

Inclusion of the Initial stock information on inflows and outflows

- In the current C 66.01 template, the "Initial Stock" column is greyed out in the inflows, outflows and contingencies sections, and only required to be reported in the counterbalancing capacity section. Although, under very specific circumstances (e.g. operations that do not have amounts that are not part of the initial stock, such as interest and fees, in the cash flow projections) the initial stock may correspond to the sum of inflows and outflows, such cases are relatively uncommon. This situation justifies the inclusion of a dedicated column to explicitly represent the initial stock.

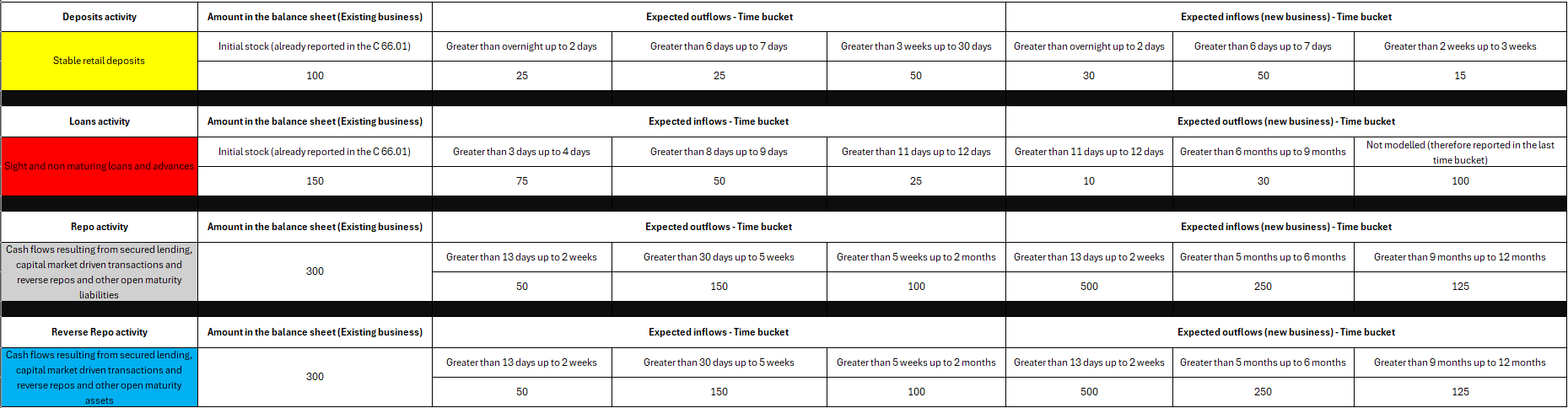

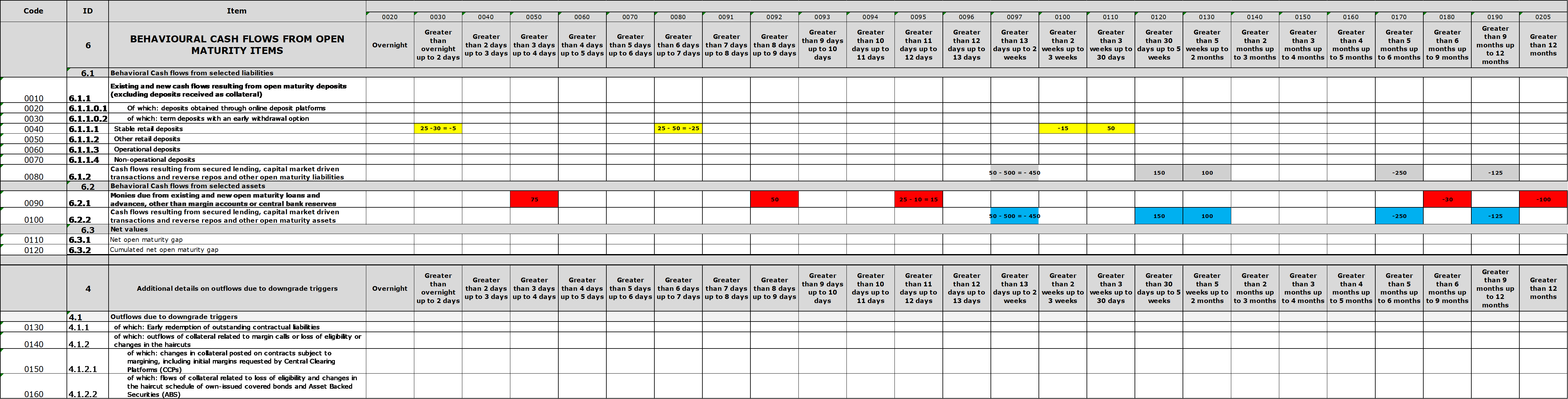

- Cash flow projections also include fees and interest paid or received on each operation or contract. These components shall not be considered part of the stock. Furthermore, for items 1.2 (Liabilities resulting from secured lending and capital market-driven transactions) and 2.1 (Monies due from secured lending and capital market-driven transactions), negative outflows are reported as inflows and vice versa. For example, in the case of forward starting repos, the initial transaction is reported as an inflow, while the repayment is shown as a positive outflow. As a result, the initial stock for repos cannot be derived by simply summing the subsequent outflows in the same row. In Section 3.4, Example 1 offers a more detailed explanation through the illustration of the reporting of a repo transaction.

- Since the initial stock must be reported differently depending on the specific item (i.e. carrying amount, market value, or nominal amount), the applicable reporting criteria for each item have been clarified in the instructions. It should be noted that this does not represent a change in the approach compared to the current template, but rather a clarification deemed necessary to prevent any misunderstanding regarding the amounts to be reported in this column, particularly in light of its expanded scope).

- On the other hand, the need for ungreying Section 4 of the template, has been assessed and not considered necessary as it is expected that the initial stock will be equal to the sum of the outflows.

Open maturity column ungreyed for secured lending and capital market driven transactions

- The Open Maturity column has been ungreyed for rows 0065 to 0257 and 0390 to 0580 to enable clear differentiation between open maturity items and those with actual overnight maturities in the case of secured lending and capital market-driven transactions. This change was implemented following supervisory lessons learned and reveal the need to capture the volume and nature of these open maturity transactions. Such granularity is particularly relevant in the context of developing the behavioural template, where understanding the maturity structure of transactions is essential for accurate risk assessment and liquidity profiling.

- The instructions have been clarified to specify that open maturity repos, reverse repos and similar transactions must be reported under the "of which: open maturity items" column as well, to distinguish them from actual overnight repos and reverse repos.

Excess operational deposits

- The current structure of template C 66.01 does not include a dedicated row for excess operational deposits as defined in Article 27(4) of Delegated Regulation (EU) 2015/61. As a result, it is not possible to distinguish these amounts, which are “non-operational deposits due to exceeding the amount required for the provision of operational services” from other “non-operational deposits”.

- Therefore, a new row—'Excess Operational Deposits'—has been added to separately identify such deposits. Currently they are reported as part of the “non-operational deposits rows” which are also being adjusted as excess operational deposits will no longer be reported here (rows 0300 to 0340). This addition aligns with the reporting structure of template C 73.00, facilitating comparability and analysis within the 30-day window.

- This approach is considered a balanced compromise between reporting burden and the needs of data users. Institutions should already have this information, and the additional reporting effort is limited to including it in a distinct row.

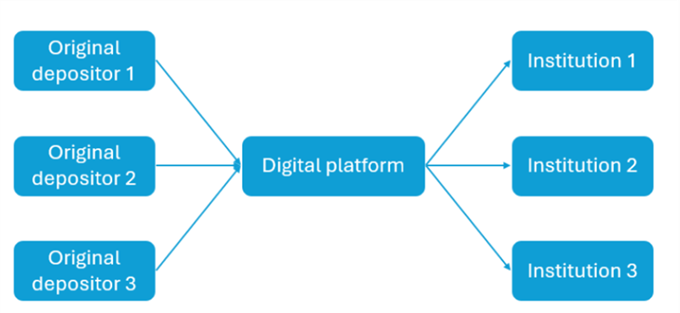

Deposits collected via online third-party platforms

- Recent trends show how an increasing number of credit institutions are relying on online third-party platforms to collect deposits. Specifically, such platforms effectively constitute virtual marketplaces where clients can choose to open sight or term deposits with credit institutions. In a similar vein, credit institutions are increasingly relying on structures where online brokers collect deposits from clients and place them among pre-defined partner credit institutions in the form of fiduciary deposits or invest the liquidity into qualifying money market funds.

- Such practice allows credit institutions to broaden and diversify their clients without having to set up an expensive IT infrastructure. At the same time, such deposits are expected to be less sticky compared to traditional deposits.

- In the current ITS such deposits are reported within the aggregated item related to deposits (i.e., item 1.3) but cannot be identified separately. In line with the market dynamics described in the previous paragraph and considering the potential liquidity risks associated with this type of deposits, it is proposed that such deposits be reported separately.

- Deposits where the ultimate original depositor is a financial customer shall not be included in this row, as doing so could result in the reporting of interbank funds, which would undermine the purpose of this row.

- The definition included in the instructions emphasizes the following important points. Specifically, institution shall report in that row:

a. deposits obtained through pure digital platforms whose purpose is solely to facilitate the transfer of funds as intermediaries, and

b. deposits obtained via an institution or a financial institution in accordance with Article 4(1)(26) of the CRR whose model is based on transfer of the funds obtained from original depositors to other pre-defined credit institutions.

Intra-group funding - FX Swaps

- To effectively perform their supervisory responsibilities, competent authorities require appropriate tools to monitor intragroup liquidity flows. A significant portion of these flows may, and often does, originate from foreign exchange (FX) swaps. Under the current reporting framework, template C 66.01 captures intragroup cash flows related to items 1.1, 1.2, 1.3, 2.1, 2.2.3, and 2.6, thereby excluding cash flows arising from FX swaps (specifically items 1.4 and 2.3). This omission prevents competent authorities from obtaining a comprehensive view of intragroup cash movements, particularly in relation to significant currencies, and may hinder the accurate assessment of liquidity risk within banking groups.

- Institutions typically manage liquidity in a single currency using foreign exchange (FX) swaps. However, in the absence of detailed information, the principal amount of a leg denominated in a specific currency may not be visible to supervisory authorities. Furthermore, institutions often manage liquidity centrally at the group level, to the greatest extent possible, which frequently involves the use of intragroup FX swaps. Under the current reporting template, such transactions cannot be distinguished from others. In certain cases, these intragroup flows represent a significant portion of the total transactions in a given currency, thereby hindering the accurate assessment of intra-group interconnectedness.

- Given the above arguments, in order to address the identified data gap, new rows named “Of which: Intragroup or IPS” have been added to items 1.4 and 2.3 in template C 66.01.

Negotiable certificates of deposit and commercial papers

- Certificates of Deposit (hereinafter CDs) and Commercial Papers (hereinafter CPs) are unsecured short-term instruments issued by banks for collecting liquidity. CPs are technically short-term debt but, unlike other bond issuances, they rarely trade in secondary markets given their short maturity and reliance on programmes that facilitate rolling over issuance and investment. CDs are negotiable instruments that fulfil similar economic functions as time deposits, but their design is like that of securities. In practice, as CPs, also CDs rarely trade on secondary markets and investors tend to hold CDs to maturity. Banks can issue both negotiable and not-negotiable[7] CDs and CPs.

- It is important to distinguish, especially in crisis, among sources of funding with heterogeneous characteristics which might result in different outflow rates. Having a higher granularity allows to identify banks’ reliance on different funding instruments and verify potential heterogeneity in the underlying roll-over assumptions.

- The current version of the maturity ladder does not provide a sufficiently granular representation of these instruments when they are negotiable, thereby impairing the ability of supervisory authorities to conduct a comprehensive assessment of institutions' liquidity profiles. Therefore, including an additional row for negotiable certificates of deposit and commercial paper as a detail of unsecured bonds due would allow for the direct identification of these items when they are negotiable, which has been highlighted as the most relevant from a supervisory perspective. Furthermore, instructions have been amended to clarify that non-negotiable certificates of deposit and commercial paper should be reported in the corresponding breakdown of Section 1.3

Contingencies

- A clarification has been incorporated into the contingencies section to ensure that all contingent outflows are reported, irrespective of any contractual provisions governing their withdrawal by the counterparty. Accordingly, this new paragraph highlights that institutions must report all contingent outflows without considering specific contractual conditions that might otherwise restrict such outflows.

- This clarification does not introduce a new reporting approach for this row. However, it has been deemed a valuable addition to enhance clarity regarding reporting expectations and to prevent any potential misinterpretation of that relevant section

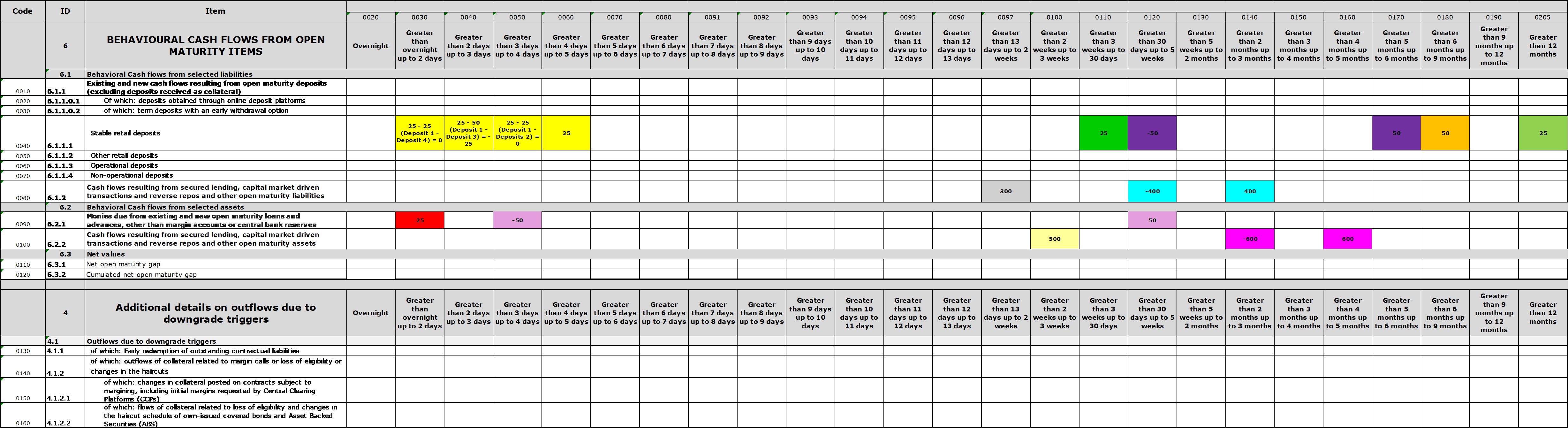

Additional details on the Outflows due to downgrade triggers section

- As part of template C 66.01, all institutions are required to report, in Section 4 – Contingencies, row 1140, the outflows resulting from downgrade triggers. These represent the impact of a material deterioration in the institution’s credit quality, corresponding to a three-notch downgrade in its external credit assessment. Currently, the instructions do not address the scenario of multiple credit ratings, which may result in different interpretations. For example, one institution might consider only the highest rating available, while another may adopt a more conservative approach by using the lowest. However, all available ratings could potentially influence the calculation of these outflows. Accordingly, a clarification has been provided to prevent any potential misinterpretation of the information required in this row.

- Furthermore, the instructions have been clarified regarding the circumstances under which a downgrade triggers a margin call, specifying two distinct cases:

(i) when the downgrade results in the requirement for additional collateral to meet margining requirements, and

(ii) when it leads to a reduction in the liquidity value of own-issued Covered Bonds or Asset-Backed Securities (ABS).

- These amounts must be included as part of the cumulative amount reported in template C66.01.

- Additionally, it is proposed that large institutions shall report the more granular information separately. In this respect, detailed rows have been added in template C 66.02 (to avoid creating a new template), in addition to the aggregated value which will continue to be reported in C 66.01. This ensures both aggregate and detailed visibility of the impacts caused by such downgrades.

- It should be noted that these clarifications do not alter the nature of the information reported in this row but rather aim to ensure consistency in the interpretation and expectations regarding the data to be provided.

Retained Own issuances from another member of the same group

- Instructions have been amended to allow institutions to include in the initial stock of counterbalancing capacity also the retained own issuances that are eligible and available for use as central bank collateral that constitute retained own issuances from another member of the same group as such assets may – economically – constitute a valid source of liquidity, especially since the assets are central bank-eligible.

- For example, an individual credit institution, which belongs to a broader banking group, can include in its initial stock of counterbalancing capacity (CBC) covered bonds that constitute retained own issuances from another member of the same group and that the reporting credit institution received as collateral via an intra-group repo, as long as these are central bank eligible.

Memorandum Items

- Given the proposed amendments to the ALMM, specifically the introduction of the new template C 66.02 (as explained in the next section) applicable to large institutions, in order to avoid double reporting, information on behavioural flows will be discontinued from template C 66.01.

- With the overall aim of reducing the reporting burden and balancing the costs and benefits, medium institutions and SNCI will also be exempted from reporting the behavioural flows information.

- Accounting for the proposed amendments to the ALMM and AE reporting framework, in particular amendments to templates F 32, certain rows within this section may, to some extent, be subject to double reporting (“similar but not identical information”). This includes HQLA central bank eligible – Tradable assets and Assets reported in 3.6 that are non-HQLA central bank eligible. Depending on the final version of the proposal, the reporting requirements may be streamlined to eliminate any potential for double reporting.

Further amendments and enhancements based on Q&As and users feedback

- As part of the broader revision of this template, it has also been considered appropriate to incorporate clarifications from several Q&As. In particular, some important changes are:

- a new point has been added to the general instructions to clarify the treatment of commodities—specifically gold—for the purpose of separate significant currency reporting.

- instructions have been amended regarding the treatment of retail term deposits with an early withdrawal option and to explicitly clarify the treatment of wholesale term deposits with an early withdrawal option, particularly in light of the scope of the new template C 66.02.

- point 12(c) of the general instructions has been refined in line with feedback received from data users. The amended paragraph specifies that it applies to committed facilities without a defined maturity, addresses the treatment of non-business days, and outlines the expected relationship between columns 0020 and 0025 regarding the amounts reported.

- The definition of “encumbered assets “has been amended in order to clarify the reporting of assets used in “non-mandatory overcollateralization within a collateral pool. In addition, another paragraph has been included explaining the expected treatment of assets that do not qualify as counterbalancing capacity at the reference date but would qualify as such at a later point in time.

- These enhancements aim to clarify reporting expectations, provide clearer guidance to institutions, and reduce the overall reporting burden by improving consistency and minimizing ambiguity.

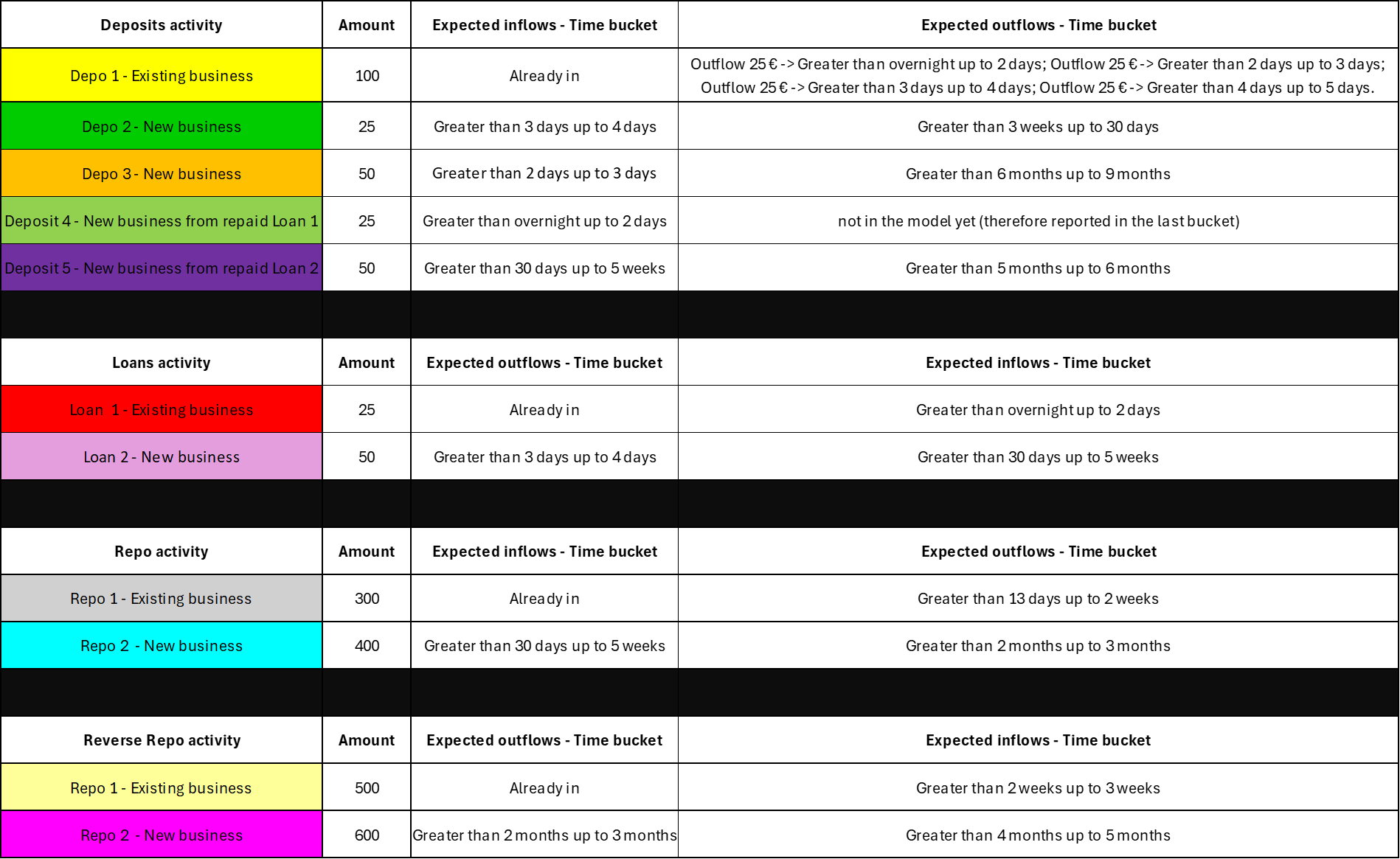

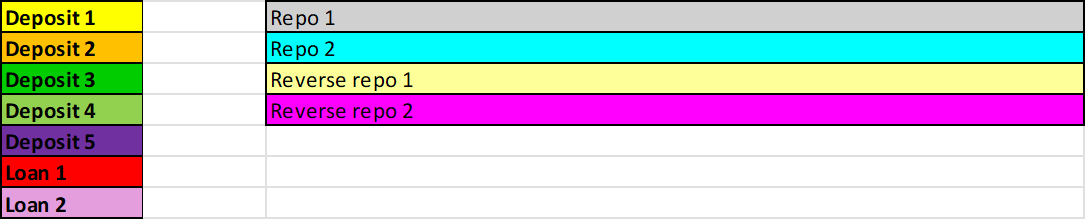

C 66.02 - New template - Behavioural information maturity ladder and details on downgrade triggers

- A new template is proposed to be introduced that would capture the behavioral information of the “open maturity items” reported in C 66.01. This information is proposed to be collected just from Large institutions.

- Current ITS regulatory reporting does not accurately reflect banks' real Net Liquidity Position, mainly since banks are required to report i). all sight deposits, ii). retail term deposits with an early withdrawal option within the following 30 calendar days where there is no material penalty in accordance with point (b) of Article 25(4) of Delegated Regulation (EU) 2015/61 and iii). wholesale term deposit outflows with an early withdrawal option regardless of any penalties as open maturity items in the C 66.01 template. For open maturity items banks are asked to report the relevant cashflows in column 0025, which is a breakdown of column 0020, in C 66.01, which can be deemed very unrealistic.

- As a matter of fact, sight deposits, for instance, are not expected to be withdrawn in significant amounts in a business-as-usual situation. As already mentioned in the previous paragraph, sight deposits are also reported in column 0025 “of which: open maturity items”, which does not accurately reflect banks’ real net liquidity position in the respective time buckets. In this respect, it is worth noticing that even in the Liquidity Coverage Ratio, which can be considered a stressed metric, retail sight deposits receive a run-off rate between 5% and 20%. Among open-maturity items, sight deposits generally represent the most relevant source of funding for banks, often used also to finance medium and long-term activities, which makes it crucial for banks to define reliable roll-over assumptions for outflows based on different counterparties’ behaviour.

- One of the main objectives of this template is therefore to monitor the expected stability of open maturity deposits, as reflected in institution-internal behavioural models. At the same time, regulators need to check if inflows resulting from open maturity activities enhance funding resources and to assess the relevant banks’ behavioural assumptions. In this respect, supervisors’ estimation of the liquidity position of the banks should leverage on more realistic assumptions, taking into account the historical cashflow rates observed by the banks, the internal behavioural models and their own estimations. Furthermore, such a template would align the supervisors’ available data with banks’ internal maturity ladder, which is used to steer the banks liquidity position, thus contributing to the harmonization of the reporting practices (data for reporting vs data used for internal purposes).

Rationale for capturing assumptions about new businesses

- Unlike the open maturity items that are expected to be reported in C 66.01, according to the existing business, in template C 66.02 institutions are also required to include the “new business” in their projections. New business should encompass both cashflows from new clients and new cashflows from existing clients.

- The following points underline the necessity of including new business assumptions in a behavioral template:

- Realistic representation of the evolution of the initial stock of certain items of the current C 66.01: in a business-as-usual scenario, an institution, in its liquidity needs projections, includes both existing and new business.

- Back testing opportunities: As the behavioural cashflows present a realistic evolution of the balance sheet position, the estimated evolution for the respective time bucket can be used to cross check the initial stock reported at future dates, which would provide supervisors with valuable insights on the accuracy of banks’ assumptions.

- Further details and enhanced granularity as compared with information required in the funding plans reporting: A more granular, realistic and short-term representation of the new business evolution in the C 66.02 would also provide supervisors with the possibility to receive more frequent information on the funding plan of institutions and assess their ability to execute it.

Second round effects

- In view of the objective to enable the supervisor to obtain the banks’ treasury perspective, where institution-internal behavioural maturity ladders provide for the consideration of n-round transactions (with those being understood as cashflows deriving from new business), those are also to be reported in this template accordingly. The aim of the template is to project the volume (stock) of open maturity items at time T by assuming the individual cash in- and outflows from both existing and new business activities for each individual time bucket.

Back testing

- As one of the main objectives of a behavioral template is to estimate the evolution of relevant balance sheet items, the accuracy of such estimations can be challenged and back tested.

- At reference date T the contractual maturity ladder C 66.01 shows the volume of open maturity items in column 0025. At the same reference date T, the behavioral maturity ladder C 66.02 shall display the projected cashflows of the volume of the respective open maturity items for each time bucket. The open maturity “stock” at time T in the C 66.01 together with the cashflows in each individual time bucket, should project the evolution of open maturity items in each individual time bucket. At another reference date T+1, the projected evolution (cashflows) in C 66.02 can be back tested with the open maturity column 0025 in C 66.01. The back testing is also relevant with respect to the underlying assumptions of institutions. If the assumptions of institutions are too optimistic or too conservative, back testing is a reliable tool to identify such deviations from the actual evolution in C 66.01.

Frequency

- The monthly frequency has been chosen, to account for frequently updated modelling assumptions by treasury departments and/or ad-hoc decisions. Therefore, a quarterly frequency will not be sufficient as the underlying assumptions and expected cashflows will be outdated and the monitoring including back testing of the reported figures will most likely not be accurate.

Empirical evidence and experience from ad-hoc collections

- As some authorities are already collecting behavioral information, the EBA proposal in setting up the template leverages on the lessons learned and evidence provided by those CA with respect to their ad-hoc collections: such information was deemed to be essential for supervisors, offering valuable insights:

- Possibility to monitor the actual liquidity position of the institution based on the more realistic Treasury’s assumption. This approach enables supervisors to follow the net liquidity position that is used internally by institutions for steering purposes.

- Understanding what the institution plans to do by considering also new business assumptions and not only the evolution of existing funding sources and assets.

- The reported figures can be used for stress-testing purposes and to challenge these numbers, back-testing can be used to identify whether the assumptions by the institutions were accurate.

- Integrating a behavioural template into the ITS, will help to support the aim of maximum harmonisation and simplification in the reporting universe. Eventually such integration will lead to a discontinuation of non-ITS reporting on behavioural information.

- With this consultation paper, the EBA is seeking views from the institutions on their ability to provide this data to meet the supervisor’s expectations and to gather additional views on the costs and benefits of having this information defined in an harmonised way at EEA level.

Additional details on the Outflows due to downgrade triggers section

- As explained in the section on C 66.01, Large institutions shall report granular information on downgrade triggers part of template C 66.02 (to avoid creating a new template).

C 67.00/01 - Concentration of funding by counterparty

- Information in template C 67.00 was streamlined with the main objectives of:

- ensuring best practices in reporting, such as to define atomic concepts for product type and counterparty sector reporting options;

- filling in data gaps by enhancing the scope of reporting and requesting additional detailed information.

Increase in the number of counterparties to be reported – just for large institutions

- Supervisors’ experience using the data collected so far on the funding from the top 10 counterparties has shown that it does not provide a complete view on the level of concentration of funding sources, amongst others, the three potential major funding sources: deposit, repurchase agreements and intra-group funding. The extension of the reporting obligations to the top 30 counterparties would allow to complete the analysis on Large Institutions counterparties concentration. Considering the principle of proportionality, additional information is proposed to be collected only from Large Institutions.

- In the case of Large institutions, the scope of reporting was increased from the top 10 counterparties to the top 30 counterparties. This has led to the need to define a separate template to be reported by Large institutions (C 67.01), although, in terms of content, the two templates are fully aligned. That means that all the changes to reporting requirements made to template C 67.00 (which will continue to be reported by medium institutions and SNCIs) and explained in this consultation paper are also valid for template C 67.01.

- A detailed overview of the content changes brought to C 67.00 and reflected also in the new template C 67.01, and the rationale behind including them are:

Removal of the 1% threshold

- Under the current situation, institutions report only those counterparties from which they receive funding in proportion of more than 1% of their liabilities. Greater granularity provided by the removal of the 1% threshold would support the supervisory assessment of potential funding concentrations by sector and geography. As the 2023 bank turmoil[8] has shown, the ability to identify and monitor potential funding concentrations beyond the single counterparty is relevant both under business as usual and during periods of stress. The deletion of the threshold would allow a view on sectorial concentration in addition to individual counterparty concentration (e.g. “x” number of counterparties in the top 10 as part of the same industry).

- This more granular view on the concentration risk would answer to ILAAP requirements as regards the identification of concentration risk in the funding providers.

Additional granularity for the counterparty sector

- Following the current instructions, institutions shall report the “Issuer sector” in line and with the granularity of the sectors defined in FINREP, Annex V to the EBA IT solutions. It is proposed that a more granular split is provided for “Other financial corporations”. The split of the information ensures that each option is a disjoint set (each sector entity would fit only one option).

- This additional information will provide a clearer view on banks’ exposures to different non-bank financial institutions (NBFI) sectors. This is of particular importance as past analyses performed by ESAs have shown that there is a high interconnection between non-bank financial institutions and the banking sector[9]. As these sectors are regulated under different regimes and may have different reactions in time of crisis (e.g. pension fund reactions to the “Uk mini budget”[10]) the breakdown of sectors will allow for more detailed analysis for financial stability purposes, particularly when it comes to contagion analysis.

| Current “counterparty sector” | Proposed options in the amended template for “issuer sector” |

|

|

|

|

|

|

| Other financial corporations will be split into the categories below:

|

|

|

|

|

- In addition, the higher granularity for “other financial institutions” would align with granularity requested for other reporting of counterparty sectors. E.g. in the large exposure reporting, investment firms are reported separately under the “Sector of the counterparty” and “Insurance, reinsurance and pension funding, except compulsory social security” are flagged as part of the NACE code in the same template. In addition, it is currently proposed (EBA/ITS/2025/04) to extend the Z02.00 to include a breakdown for Insurance firms and pension funds, a distinction already in place for SRB Liability Data reporting.

Reporting of values for “sector” and “residence” for connected clients

- Current reporting instructions mention that “For groups of connected clients, no sector shall be reported.” Instructions have been amended to include guidance to the institutions on how the columns should be reported, avoiding gaps in the data reported. In the cases where the group of connected clients does not have a parent, the counterparty that shall be reported shall be the sector/residence of the individual entity, which is considered by the institution as the most significant within the group of connected clients.

Refinement of the instructions for the product type and intra-group funding

- The current instructions for product type combine information on the product with information on the counterparty sector and intra-group exposures. It is proposed to streamline the information for the product type and make it more efficient for reporting purposes by:

- removing information on the counterparty from this column (as this information would already be reflected in the counterparty sector column) and by

- removing information related to intra-group exposures (and inclusion of an additional column that would capture this information).

- In addition, the current pre-defined list of “Product Type” is enhanced to capture additional product types given that:

- As per the current instructions, deposits other than retail deposits are classified as wholesale funding which does not allow competent authorities to have a detailed view on the different components of deposits.

- The same holds true for retail deposits which are currently included in “Other funding products”.

- The SFT reporting covers only repurchase agreements to be reported, while the full set of SFT products would be relevant to be captured.

- The updated instructions provide an exhaustive list of “Product type” displaying the types of deposits in a distinct product type. The instructions would be finetuned by adding 2 sub-types to the existing list of the 8 product types listed in the instructions: Deposits and Monetary policy operations. The current categories UWF (unsecured wholesale funding obtained from financial customers including interbank money) and UWNF (Unsecured wholesale funding obtained from non-financial customers) would be merged into one category UWF (Unsecured wholesale funding).

- By requesting the types of deposits separately, the terms “other than deposits” would be added in the Unsecured Wholesale Funding. Similarly, the “e.g., retail funding” in the Other Funding Products would be deleted.

- As explained in the section above, to stream-line reporting requirements, the intra-group funding would be identified in a separate column of the template. Instructions have been enhanced to request institutions not to group the intra-group funding at the level of each entity, in order to assess counterparty exposure within the institution.

- The split of the information ensures that each option related to the product type is a disjoint set (each product would fit only one option).

| Current C67 template | Proposed options in the new C67 template |

|

Institutions shall report all types of funding received from monetary policy operations, irrespective of the instruments and/or product types. |

|

Financial customers/ non-financial customers relate to the type of counterparties and not the product type. |

| |

|

|

|

|

|

|

|

|

|

|

|

- Examples on how to report C 67.00/01 with the old reporting and the new proposal are provided in Section 3.4.

Removal of column “National Code”

- To align with the supervisory reporting practices, whenever the “LEI code” is available, institutions are required to report it. This information should be enough for authorities to properly identify the institution and is therefore unnecessary that the national code is also reported.

Removal of reference to Finrep value

- Current reporting instructions included that there should be an equivalence between the data reported in the Finrep and the C 67.00. Based on past EBA Q&As (2015_2365 ,2023_6956), it was identified that due to different reporting dates, netting rules, consolidation scopes, this equivalence is not always possible. As part of this ITS update, it is proposed to delete the paragraph in order to avoid any unnecessary ambiguities. The Q&A will be archived.

C 68.00 - Concentration of funding by Product Type

- Changes are made to this template with the objective of enhancing the view on the products that are used for funding by requiring:

- additional granularity on the structure of deposit funding and wholesale funding and

- to fill in some data gaps by adding information on capital instruments and central bank funding.

- Concepts have been aligned with the definitions used in the other templates of ALMM.

- The following sections will explain why these additional data requirements turned out to be necessary for supervisors in assessing institutions’ funding risk resulting from its concentration of funding.

Extension of retail funding

- Authorities deem it important to receive full visibility on the institutions’ deposit funding. Hence, one additional row on the retail deposit funding is added to the template. The information on the carrying amount, weighted original and residual maturity for retail deposits is useful for competent authorities to spot the dependency on this type of funding.

Breakdown of term deposits

- Experience with the data reported has shown that instructions need to be enhanced to ensure a harmonised reporting approach regarding term deposit breakdowns. It is proposed to add a more granular view in the template for retail term deposits that are not withdrawable within the following 30 days by differentiating based on the cause. The two additional rows refer to Article 25(4) of Delegated Regulation (EU) 2015/61, of which point (a) determines retail deposits that are not withdrawable within 30 days according to contractual arrangements and point (b) which includes all retail term deposits for which a material penalty upon early withdrawal is defined.

- The split between retail term deposits that are withdrawable or not within 30 days is needed to get a full picture of the structure of these deposits.

- The additional information on term deposits helps supervisors in understanding the structure of the institutions’ deposits. Also, for analysing the risk of outflows of deposits it is valuable to differentiate term deposits by their contractual agreements and to know about the maturity structure and the Deposit Guarantee Scheme (DGS) coverage of these deposits. Furthermore, periods of higher interest rates showed that retail term deposits may be an important funding source.

Breakdown by deposit size

- The new version of the template splits retail deposits by size, for which the carrying amount and the weighted maturities are requested, providing an extended picture of the structure of deposit funding : e.g. changes over time in the deposits buckets can provide a direct view on bank’s deposits allocation: either a lot of small single depositors or fewer large deposits.

- It is required to report the deposit size on a per client basis. The banking turmoil in 2023 underlined the importance of monitoring high volumes of deposits from single depositors. These rows complement information from template C 67.00/01, by providing information on the part of funding stemming from such high-volume depositors and the underlying maturity structure.

Introduction of higher granularity for the wholesale funding and addition of the “intra-group or IPS” column

- The current split between secured and unsecured wholesale funding is maintained, however the underlying granularity was enhanced to focus on the most important sources of founding.

- Some rows have been relabelled to ensure consistent naming conventions across the ALMM and AE templates.

- The current version of the template requires to submit data regarding “loans and deposits from Intragroup entities” and “financial liabilities other than derivatives and short positions from intra-group entities” which is essential to monitor. There could be also capital items which are intragroup funding which is essential to be monitored given that intra-group funding concentration could increase banks vulnerabilities and exposures to idiosyncratic stress situations.

- For this reason, a column dedicated to “intragroup or IPS funding” has been added to the template, ensuring a more efficient representation of the data requirements. The content and label of this column have been aligned with C 66.01, where both intra-group and IPS funding is seen as equally important. The two rows requested in the current version of the template: “loans and deposits from intragroup entities” and “financial liabilities other than derivatives and short positions from intragroup entities” can be deleted as the corresponding amount would be available by means of the newly added column.

Inclusion of certain Capital Items

- The new C 68.00 shall include information on capital instruments: Additional Tier 1 items except preferred shares (AT1) and Tier 2 items (T2).

- The total amount of capital items is currently reported on a yearly basis in the funding plan and on a quarterly basis in capital reporting and the NSFR. The inclusion of the capital items information in the C 68.00 will cater for a comprehensive view on the entire funding structure of banks while also providing unique information on the original and residual weighted maturity of AT1 and T2 items, and on the Intra-group funding part, which are not retrievable elsewhere. Given their relevance in the funding structure of a bank and considering the prominent role played by their spread when monitoring market perception, it is important to have them reported separately within the template C 68.00.

- The data on capital items are particularly relevant when assessing the interdependence between liquidity and solvency, banks’ funding needs and the MREL requirements. The inclusion in C 68.00 allows to benchmark banks across this dimension, including the volume and residual weighted maturity which cannot be retrieved elsewhere.

- To be noted that by introducing separately the category of capital items, other rows of the templates would need to be adjusted content-wise, as compared to the current version, to avoid double reporting (some information related to capital items, that was before reported in the wholesale funding part, would now need to be reported in the new section).

Central bank funding

- Despite being one of the most important sources of funding, the current version of the C 68.00 template does not require banks to provide information on their central bank funding. One argument for the inclusion of central bank funding is the expectation for SSM institutions’ that they should consider refinancing operations provided by central banks as part of their day-to-day liquidity management. Additionally, incorporating the central bank funding into the C 68.00 allows for coherent alignment with the annual funding plans reporting where such funding is reported.

- The template is enhanced with information on all funding provided by a central bank in the European Economic Area to a reporting entity incorporated in the European Economic Area. This can concern the following two cases:

i. An institution or a subsidiary of a European Economic Area institution having access to European Economic Area Central Bank funding

ii. a subsidiary of a non-European Economic Area institution established in the European Economic Area having access to European Economic Area Central Bank funding

- One additional row reveals which part of the EEA funding is obtained from the Euro system including funding from the European Central Bank. and another row the funding from a central bank from outside the European Economic Area is introduced. An example for the reporting of these rows is provided in the examples’ section.

Amount not covered by Deposit Guarantee Scheme (DGS)

- The column on “Amount not covered by a Deposit Guarantee Scheme in accordance with Directive 2014/49/EU or an equivalent deposit guarantee scheme in a third country” is not necessary for data collection purposes as the amount not covered by DGS can be retrieved by subtracting the amount covered by DGS (current column 0020) from the carrying amount received (column 0010). Therefore, we ask for feedback regarding the burden created by deleting or keeping this column. The proposal is for this column to be deleted.

C 69.00 - Prices for various lengths of funding

- Regarding C 69.00, changes to the content are proposed making sure that the reporting framework remains relevant for supervisory authorities, given supervisory experience with the data reported. The granularity of the products, labels and definitions have been aligned with the rest of reporting requirements in ALMM.

- The overall objective of the template and in particular the focus on new funding remains unchanged. The main changes to the content are as follows:

Focus on Deposits

- The current version of the C 69.00 template requests the prices only for retail funding, not differentiating between deposits or bonds. To allow the identification of the evolution of the pricing for retail deposits and align with the structure of the information from the other templates, it is proposed to introduce the retail deposit as a distinct reporting item. Retail deposits are of particular interest to supervisors as they make up most of the funding for retail banks. In addition, changes in price sensitivity of retail customers may indicate the stickiness of the retail customers compared to other sources of retail funding.

- In addition, the evolution of prices of the non-financial corporates deposits is also important. Such deposits tend to be priced off benchmark rates and tend to be more volatile. Changes in their cost of funding, including by material currency, may allow supervisors to better identify when banks are overpaying on non-financial corporates deposits to obtain/defend funding or potentially experiencing funding stress in a significant currency.

Information on preferred/non-preferred bonds

- The current version of the C 69.00 template requires the prices for Senior unsecured securities in an aggregated row. The proposal is to split the information into 2 rows and focus on: Senior preferred bonds (SP) and Senior non-preferred bonds (SNP) to collect more granular and targeted data on the prices of unsecured wholesale funding. This split is very relevant as the senior non-preferred bonds might be more price sensitive. Given that only new funding is reported, this split is essential to accurately reflect the distinct risk profiles and market dynamics of these instruments. Also, market conditions can play a critical role in influencing the magnitude of the price differential between SP and SNP.

Information on Repurchase agreements

- The current version of the C 69.00 template requires only Covered bonds and ABS under the secured funding, while Repurchase agreements could represent an important part of bank’s secured funding as well and the evolution of their prices should be reported and followed by supervisors.

Inclusion of certain Capital Items

- The new C 69.00 shall include information on the capital items such as: Additional Tier 1 instruments (AT1) (except preferred shares), and Tier 2 instruments (T2). AT1 are currently reported on a yearly basis in the Funding Plan and on a quarterly basis in Capital reporting and the NSFR. The change would provide a comprehensive view of the prices of new funding by banks, while also providing unique information on a more frequent basis to monitor potential price increases in AT1 issuances and earlier warning on a price of funding deterioration. AT1 and T2 instruments can be considered as subordinated form of funding. Given their relevance in the funding structure of a bank and considering the prominent role played by their price when monitoring market perception, it is important to have them included within the template C 69.00. As in C 69.00 only new AT1 and Tier 2 issuances are to be reported, the initial maturities not eligible were greyed.

- Data on equity, except AT1 considered equity, was not added as their price is unknown when paid in and this funding tends to be rarely new. However, AT1 (except preferred shares) was added even if considered equity under FINREP as prices of all types AT1 are relevant for supervisors. In the past, a potential increase in the price of new unsecured wholesale funding could thus be due to the subordination of AT1 and not a change in market perceptions.

- To be noted that by introducing separately the category of capital items, other rows of the templates would need to be adjusted content-wise, as compared to the current version, to avoid double reporting (some information related to capital items, that was before reported in the wholesale funding part, would now need to be reported in the new section).

Changes in the label of the columns and the addition of another column

- In order to provide clarity also at template level, the labels of the columns have been updated showing the interval for which the length of funding is considered. This represents no change in the content, as the instructions had already reflected these requirements. Adding the clarification in the labels will also align with the format used for C 66.01 and C 66.02 templates.

- In addition, a new column has been added to capture the funding period of 10 years or more. Current instructions requiring for funding above 10 years not to be reported were amended to better reflect the funding profile of banks issuing long-term.

Replacement of spread with Interest rate

- Supervisory experience with the data currently reported in C 69.00 requiring institutions to report the spreads of funding using benchmark rates or swap curves, has shown that the comparison across banks is not reliable given the fact that banks can use highly different methodologies and choices, particularly:

- Some banks do not use a Swap curve per currency, instead they use the swap curve of another significant currency (e.g., EUR) and add the FX rate which is a spot rate which do not take into consideration macroeconomic perspectives.

- Some banks do not use swap curves and apply the same Benchmark rate (e.g., Euribor 3 months) for all maturities (buckets), in these cases, the price for maturity transformation would be included in the spread.

- In both instances, supervisors cannot be certain about the approach banks applied.

- A spread with an unknown benchmark/swap rate has proven to be a black box for supervisors as they cannot know if changes are due to changes in the benchmark rate or interest rate. Since it is not known when and how much of the funding was obtained, it is not possible to calculate the applicable reference rate in the retrospective. In times of stable reference rates and flat benchmark curves, this is no major issue, since the likelihood of picking the appropriate reference rate value is higher. However, in times of greater volatility and sloped benchmark curves, the likelihood of a supervisor guessing the appropriate reference curve/rate decreases. This makes the data quality conditional on the volatility of reference rates and slope of the benchmark curve. Therefore, not as reliable.

- Given the above, the proposal put forward in this CP is to request that the interest rate is reported instead of the spread enabling more comparability across institutions and allowing the identification of spreads by supervisors, if needed, by subtracting the relevant benchmark/swap rates. Requiring that the interest rate is reported will therefore:

- reduce complexity minimising the data quality issues related to the fact that benchmark rates may be unavailable.

- no more need for reference rates in the calculation of the reported information (interest rates).

- the ease to report interest rates would remove other data quality issues linked to the usage of the benchmark rate of another currency.

- reporting heterogeneities are likely to be higher for spreads than interest rates, as banks have to make additional choices during the computation.

- Regarding the definition of the interest rate to be reported:

- for capital market instruments the price (interest rate) should be the annual return a credit institution provides over the term to maturity of capital market instruments, encompassing both interest payments and principal. The price should be expressed as an annual percentage rate. This constitutes an effective interest rate.

- for other types of funding, the price (interest rate) will be the annualised agreed rate (AAR) as defined in Annex I of Reporting Scheme For Monetary Financial Institution INTEREST RATE STATISTICS of REGULATION (EU) No 1072/2013 OF THE EUROPEAN CENTRAL BANK of 24 September 2013 concerning statistics on interest rates applied by monetary financial institution. This constitutes a nominal interest rate.

- The annualised interest rates add more comparability and simplification, however by definition the interest rates between deposits and capital market instruments are not fully comparable as costs and other effects are not included in both.

- The choice to differentiate between the price of funding for market funding and other types was made to have a simple calculation for other types of funding and to have the needed granularity to take into account the divergence in the way bond holders get remunerated. Supervisors can thus trackmore accurately the price of market funding while banks will not be burdened by monitoring the full cost of for example deposit taking (such as costs associated to brand image etc).

- The options above were selected as requesting the full price of every type of funding on a monthly basis was perceived as an outsized burden to banks and would result in reporting errors as banks would struggle to measure the full price monthly for non-market funding.

- The current Funding Plan reporting (2B: Pricing) requires the reporting of the Yield/cost without explicitly clarifying in the instructions if it should correspond to an Effective or Nominal interest rates. However, Yield/cost imply an effective interest rate so C 69.00 will now be closer aligned to the Funding Plan Instructions.

C 71.00 Concentration of counterbalancing capacity by issuer

- Instructions related to the counterparty sector have been amended to align with the changes made for C 67.00.

- In addition, column 0090 was deleted and replaced by a new column “Value after haircut” aligning the information requested with the changes proposed for the Asset encumbrance framework, as explained in the section below.

1.6 Amendments to Asset encumbrance framework

Development and evolution of AE templates

- The European Systemic Risk Board (ESRB) Recommendations on Funding of Credit Institutions, published in February 2013, recommended European Banking Authority (EBA) to develop reporting and disclosure requirements in relation to asset encumbrance and closely monitor institutions’ asset encumbrance evolution[11]. In response to these recommendations, the Capital Requirements Regulation (CRR) mandated the EBA to develop reporting standards that would provide greater transparency regarding asset encumbrance. To fulfil this mandate, the EBA introduced the Asset Encumbrance ITS reporting templates (F32, F33, F34, F35, and F36) in December 2014, in line with Article 100 of the CRR. These templates require institutions to report to their competent authorities the level of repurchase agreements, securities lending, and all other forms of asset encumbrance, at least in aggregate terms. The aim was to ensure a standardized approach to capturing and reporting such information within the EEA banking sector.