Consultation Paper on Revisions to the ITS on supervisory reporting (Commission Implementing Regulation (EU) 2024/3117) - Module on FINREP

The content on these interactive pages is provided for ease of reference and to assist in the reading and understanding of the Consultation Paper and it is not considered as the official version of such documents.

For the formal consultation papers and their components, please refer to the .pdf documents provided at the bottom of this page. In case of discrepancies between these interactive pages and the .pdf documents, the latter prevail as the authentic official versions.

Responding to this consultationPlease provide your responses by 10 July 2026 at 23:59 CEST via EU survey (Password for the survey: Reporting2026)

Please provide your responses to IFRS 18 related questions affecting templates (F 02.00, F 16.01, F 16.02, F 16.03, F 16.04, F 16.04.1, F 16.05, F 16.06, F 16.07, F 45.02, F 45.03, F 20.03 and the related instructions by 10 May 2026 23:59 CEST via EU survey (Password for the survey: Reporting2026). Late responses will not be considered. |

1 Background and rationale

- In accordance with CRR Article 430 (3)(4), the reporting on financial information (Finrep) applies to credit institutions required to prepare their consolidated financial statements in accordance with International Financial Reporting Standards (IFRS) as endorsed by the EU, as well as to credit institutions required by supervisors to use IFRS endorsed by the EU for the determination of own funds and to investment firms subject to Article 4 of Regulation (EC) 1606/2002. The EBA originally chose to base the reporting of financial information (Finrep) on accounting standards to achieve efficient regulation by aligning supervisory reporting of financial information with accounting standards. Therefore, Finrep needs to be reviewed whenever the underlying international accounting standards adopted in accordance with Article 6(2) of Regulation (EC) 1606/2002 are updated.

- In April 2024, the International Accounting Standards Board (IASB) issued ‘IFRS 18 - Presentation and Disclosure in Financial Statements’, which supersedes the accounting standard ‘IAS 1 -Presentation of financial statements’. IFRS 18 introduces a defined structure for the statement of profit or loss, where the items are classified into three new main categories (operating, investing and financing) with the aim of increasing comparability and transparency of entities’ performance reporting. The new IFRS 18 standard has been endorsed by Commission Regulation (EU) 2026/338, and it will be applicable for reporting periods beginning on or after 1 January 2027.

- Following the issuance of IFRS 18, changes are therefore required to the existing Finrep reporting templates and related instructions for IFRS reporters to harmonise Finrep with IFRS 18 and avoiding different/double reporting requirements with institutions’ public financial statements.

- While Finrep reporting remains aligned as much as possible with the relevant accounting standards, in accordance with CRR Article 430(5), ITS also requires the necessary information to obtain a comprehensive view of the risk profile of institutions’ activities and a view of systemic risks posed by institutions to the financial sector or the real economy. As a result of that, some parts of the Finrep framework need to be reviewed to address evolving supervisory needs, including monitoring emerging risks, and incorporating improvements in reporting templates and instructions based on the experience with data quality and feedback received by the stakeholders through the single rulebook Q&A mechanism.

- In summary, this Consultation Paper proposes amendments of Finrep reporting due to the IFRS 18 implementation, as well as other changes driven by the evolving supervisory data needs in accordance with CRR Article 430(5) and by the Commission’s goal of reducing costs associated with reporting requirements.

- The first reporting reference date is expected to be 30 September 2027. However, a shorter consultation process with an earlier first reporting reference date is planned for the Finrep templates mainly affected by the IFRS 18 implementation (i.e. F 02.00, F 16.01, F 16.02, F 16.03, F 16.04, F 16.04.1, F 16.05, F 16.06, F 16.07, F 45.03, F 20.03). Indeed, the endorsed version of IFRS 18 has the same first application date of IASB’s IFRS 18 (i.e. 1 January 2027). Consequently, it is important that the publication of the final version of the IFRS 18-mainly affected templates occurs enough months in advance before the IFRS 18’s first date of application, to avoid any double/different reporting requirements with the institutions’ public financial statements. The enforcement of the temporary use of these templates until they are formally adopted by the EU Commission will be set out in an EBA Decision, which will also specify the first reference and remittance dates and the related technical package (Data Point Model, Taxonomy, validation rules) of these templates.

1.1 Simplification and proportionality

- One of the main drivers of the Finrep review is simplification and proportionality to contribute to the overall objective of reducing institutions’ reporting costs.

- The simplification proposal set out in Finrep aims at striking a right balance between keeping information that are essential for conducting an effective supervision and deleting information that are deemed highly complex and granular by the industry.

- Keeping this objective in mind, the simplification proposal set out in Finrep has been developed based on different inputs: i) the list of templates considered as less relevant for day-to-day use as identified under Recommendation 14 of the EBA Study of the cost of compliance with supervisory reporting requirements (Report eba/rep/2021/15)[1]; (ii) feedback received from the Competent Authorities (CAs) and the EBA Staff using the data; (iii) data on the ‘usage’ of the templates provided by the ECB/SSM; (iv) feedback received by the industry in response to the last summer’s ECB stock-take .

- Based on these inputs, the proposed simplification measures are modulated in accordance with the relevance of the information and move in different directions: i) reduction of data points and templates, ii) frequency and scope adjustments, iii) introduction of greater proportionality, notably for SNCIs, iv) integration and streamlining of separate data collections (in particular, EU-wide stress testing) into Finrep. More in detail, the proposed simplification measures are the following:

- deleting templates that are mostly unused by supervisors, or the content of which mostly overlaps with other reporting requirements avoiding requesting duplicate information from institutions. In particular, the proposal envisages the deletion of the following templates:

- template F 06.01 ‘Breakdown of loans and advances other than held for trading, trading or held for sale assets to non-financial corporations by NACE codes’ (and the corresponding template F 20.07.01 ’Geographical breakdown by residence of the counterparty of loans and advances other than held for trading to non-financial corporations by NACE codes’) since the information on the breakdown by NACE codes will be covered by the ESG reporting framework;

- templates F 11.3, F 11.03.1 on non-derivative hedging instruments information under IFRS and NGAAP, considering its low usage at SSM level;

- template F 13.2.1 ‘Collateral obtained by taking possession during the period [held at the reference date]’, considering the less supervisory relevance of this information in comparison with the information on collateral stock included in template F 13.03.1;

- template F 21 ‘tangible and intangible assets: assets subject to operating lease’, whose information subject to a threshold is moved in template F 42 ‘Tangible and intangible assets: carrying amount by measurement method’, with an annual frequency.

- template F 23.01 ‘Loans and advances: Number of instruments’, considering the low usage at SSM level;

- template F 23.03 ‘Loans and advances collateralised by immovable property: Breakdown by LTV ratios’, given that similar information is already required in template F 18.02 ‘Commercial Real Estate (CRE) loans and in the new proposed collateral template F 37.00;

- template F 23.05 ‘Loans and advances: Collateral received and financial guarantees received’, given that similar information is required in templates F 13, F 18 and in the new proposed collateral templates F 37 and F 48;

- template F 23.06 ‘Loans and advances: Accumulated partial write-offs’ considering its low usage at SSM level;

- template F 24.02 ‘Loans and advances: Flow of impairments and accumulated negative changes in fair value due to credit risk on non-performing exposures’, given that most of non-performing exposures are generally classified in stage 3 under IFRS 9, for which the information is reported in the template F 12.01 ‘Movements in allowances and provisions for credit losses’.

- template F 24.03 ‘Loans and advances: Write-offs of non-performing exposures during the period on write-offs during the period’, considering the low usage at SSM level; however the information on debt forgiveness is moved in template F 24.01 ‘Loans and advances: Inflows and outflows of non-performing exposures’.

- template F 25.03 ‘Collateral obtained by taking possession classified as Property Plant and Equipment (PP&E)’. The information on the stock of the collateral obtained classified as PP&E is moved in template F 25.02 ‘Collateral obtained by taking possession: Type of collateral obtained’.

- template F 30.02 ‘Breakdown of interests in unconsolidated structured entities by nature of the activities’, considering its low usage at SSM level, its inclusion in the list of least used template of the the EBA Study of the cost of compliance, and the maintenance of basic information on interests in unconsolidated structured entities in template F 30.01;

- template F 31.02 ‘Related parties: expenses and income generated by transactions with’, considering its low usage at SSM level, its inclusion in the list of least used template of the the EBA Study of the cost of compliance, and the maintenance of basic information on amounts payable to and amounts receivable from related parties in template F 31.01;

- template F 40.02 ‘Group structure: "instrument-by-instrument" and other control relationships’ considering its low usage at SSM level and its inclusion in the list of least used template of the the EBA Study of the cost of compliance;

- template F 41.02 ‘Use of the Fair Value Option’ considering its low usage at SSM level.

- template F 43.00 ‘Provisions’ considering its low usage at SSM level and the inclusion of similar information in institutions’ public financial statements, although the accounting scope of consolidation may differ from the prudential one. However, the information on provisions for pending legal issues and tax litigation and other type of provisions relevant for the calculation of own fund requirements for operational risk are moved in ad-hoc rows of template F 02 ’Statement of profit or loss’;

- templates F 44.01 ‘Components of net defined benefit plan assets and liabilities’ and F 44.02 ‘Movements in defined benefit obligations’, considering their inclusion in the list of least used template of the the EBA Study of the cost of compliance and the fact that the information can be easily obtained by the institutions’ public financial statements. Indeed, the information corresponds to the requirements of IAS 19, and it has an annual frequency like the institutions’ public financial statements, although the accounting scope of consolidation may differ from the prudential one;

- template F 45.01 ‘Gains or losses on financial assets and liabilities designated at fair value through profit or loss by accounting portfolio’ considering that the information is mostly covered by template F 16.05 ‘Gains or losses on financial assets and liabilities designated at fair value through profit or loss by instrument.

- template F 47.00 ‘Average duration and recovery periods’ considering its low usage at SSM level.

- restructuring and dropping some details, especially in NPL templates, with the aim of avoiding requesting similar information in different Finrep templates, while focusing more on the supervisory needs:

- templates F 07.01 and F 07.02 on ‘financial assets subject to impairment that are past due’ are revamped by focusing only on the essential information on loans and advances (rows 0120, 0170, 0180 and rows from 0200 to 0310) and dropping the information on debt securities, given that the information on past due breakdown of template F 18.00 may be used as ‘proxy’ of the information of templates F 07;

- in templates F 09.01.1 and F 09.01 on off-balance sheet exposures, the information on non-performing exposures is dropped considering that similar information is available in template F 18.00;

- in template F 15.00 ‘Derecognition and financial liabilities associated with transferred financial assets’, the breakdown is simplified by focusing only on the accounting portfolios;

- in templates F 22.01 and F 22.02 on ‘fee and commission income and expenses and the assets involved in the services provided’, the breakdowns are simplified by eliminating some details per specific fee and commission categories;

- in templates F 23.02 ‘Loans and advances: Additional information on gross carrying amounts’ and F 23.04 ‘Loans and advances: Additional information on accumulated impairments and accumulated negative changes in fair value due to credit risk’, the information on loans measured at cost or at amortised cost is dropped since it should mostly overlap with the information of the total of loans and advances also reported in these templates.

- in template F 24.01 ‘Loans and advances: Inflows and outflows of non-performing exposures’, some detail information (of which rows) within the inflows and outflows is dropped.

- in the template F 25.01 ‘Collateral obtained by taking possession other than collateral classified as Property Plant and Equipment (PP&E): Inflows and outflows’, the information on ‘time passed since recognition in balance sheet’ is dropped, while it is kept for the stock of collateral obtained by taking possession in template F 25.02 ‘Collateral obtained by taking possession: Type of collateral obtained’.

- in template F 26.00 ‘Forbearance management and quality of forbearance’, the detail information on 'Gross carrying amount of non-performing forborne loans and advances that failed to meet the non-performing exit criteria' is dropped;

- in template F 30.01 ‘Interests in unconsolidated structured entities’, the information on fair value of liquidity support drawn is dropped since the information is similar to the one on liquidity support drawn reported in the same template;

- in template 41.01 ‘Fair value hierarchy: financial instruments at amortised cost’, the granularity of information on the level 3 fair value is reduced by requiring the values only for debt securities measured at amortised cost or cost. On the other hand, the frequency of this template is increased from annual to quarterly, as specified below under the paragraph on ‘other adjustments’ to Finrep.

- reducing the frequencies where the information is still considered as relevant for supervisors, but it is not generally used in day-to-day supervisions. In particular:

- the frequency of template F 13.3.1 ‘Collateral obtained by taking possession accumulated’ is reduced from quarter to semi-annual, considering the generally low variability of this information;

- the frequency of template 15 ‘Derecognition and financial liabilities associated with transferred financial assets’ is reduced from quarter to annual;

- the frequency of templates 17 ‘Reconciliation between Accounting and CRR scope of consolidation: Balance Sheet’ is reduced from quarterly to semi-annual;

- the frequency of template 30.01 ‘Off-balance sheet activities: Interests in unconsolidated structured entities’ is reduced to from semi-annual to annual;

- the frequency of template F 31.01 ‘Related parties: amounts payable to and amounts receivable from’ is reduced from semi-annual to annual;

- the frequency of the information on assets subject to operating lease moved in template F 42 is reduced from quarterly to annual.

- increasing proportionality for reporting of information on derivatives (templates F 10 and F 11) and on geographical breakdowns (templates F 20), given that the information is extensively used for supervisory analysis, but the templates are generally deemed highly complex and burdensome by the industry:

- in templates F 10 and 11 on derivatives, the introduction of proportionality for small and non-complex institutions (SNCI) aims at alleviating their reporting costs linked to the granularity of the information requested. The relative threshold for SNCI is built on the basis of the one provided by the CRR (Article 4 (145)(e)) to facilitate the monitoring by institutions;

- in templates F 20 on geographical breakdown, the introduction of an additional layer of proportionality to group all exposures lower than 1% towards countries under the z-axis ‘Other countries’. A specific question is included in this consultation to know whether the proposal may effectively help alleviate institutions’ reporting costs.

- introducing a ‘core and supplement approach’, as suggested by the 2021 EBA Cost of Compliance report. In accordance with this approach, the templates currently included in Part 1 of Finrep with the exceptions of templates F 15 and 17 and including templates F 20 and F 22 are proposed to be the ‘core part’ (applicable to all institutions), and the rest of the templates in Parts 2, 3 and 4 with the exceptions of templates F 20 and F 22 and including templates F 15 and 17 are proposed to be reported by institutions other than SNCI (‘supplement part’).

- integrating other reporting in Finrep and discontinuing ad-hoc data collection. Specifically, data points to meet the EU-wide stress testing data needs would be added, notably in templates F 16.03 on gains or losses on trading financial activities, F 16.08 on other administrative expenses, F 44.04 on staff expenses and including new templates F 49.01, F 49.02 and F 50.00 for credit risk and market risk stress test purposes respectively. The proposed changes are further explained in the separate CP on stress test data needs. Moreover, the inclusion of the information on ‘overlays’ in template F 12.01 allows to get information relevant for supervision as further explained in the paragraph below on ‘Other adjustments’ and at the same time it will allow to discontinue a corresponding ECB ad-hoc data collection to significant institutions. In addition, the adjustments to the columns of template F 44.04 on staff expenses allow to be aligned with the respective Pillar 3 disclosures information and, at the same time, a corresponding ECB ad-hoc data collections to significant institutions will be discontinued.

- revamping the structure of the templates and related instructions with the aim of helping users read and navigate across templates, legal references and instructions. Notably, after this public consultation, the templates and the related instructions will be grouped into modules in relation to the different topics. The new index will include all the relevant information (core/supplement, frequency, proportionality) for each template and an ad-hoc Excel file will include all the legal references per template, row, column to facilitate the identification of the relevant information. The instructions will be reshaped by renumbering and putting the paragraphs in the right order in line with the templates. Indeed, in this consultation, the instructions to new templates have been put in the end in order not to change the numbers of the existing paragraphs and the references in the columns and rows of all the templates.

1.2 Rationale and content of reporting changes topic by topic

1.2.1 IFRS 18: implementation in Finrep

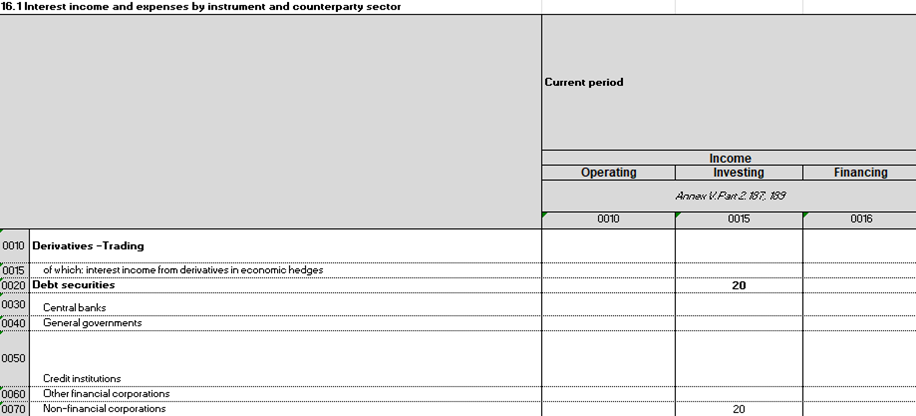

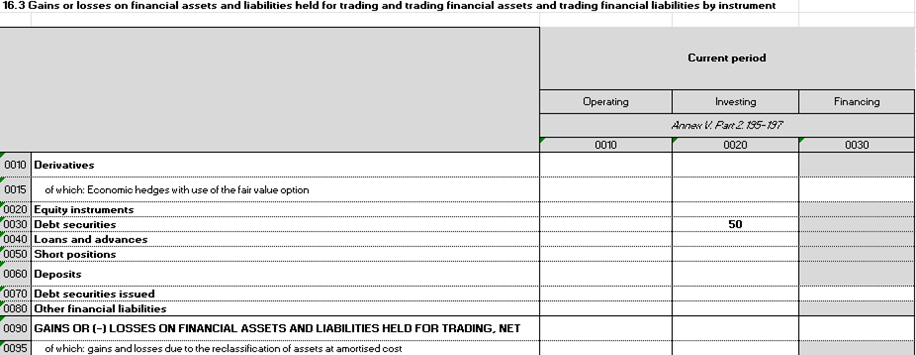

IFRS 18: new banks’ structure of statement of profit or loss

- In April 2024, the IASB issued the accounting standard IFRS 18 'Presentation and Disclosure in Financial Statements', which replaces IAS 1 with a focus on the Statement of profit or loss. The new standard has been endorsed by Commission Regulation (EU) 2026/338 and it will apply for reporting periods beginning on or after 1 January 2027. The aim of the new standard is to increase comparability of the financial performance of similar entities, especially in relation to the definition of 'operating profit or loss’.

- IFRS 18 introduces a defined structure for the statement of profit or loss, which is composed of five categories, three of which are new – operating, investing, financing, and of mandatory subtotals. IFRS 18 sets out detailed requirements for entities to classify the items among these categories.

- IFRS 18 takes into account the specific characteristics of entities whose main business activities are providing financing to customers and/or investing in assets (retail and investment banks) by requiring classifying additional income and expenses in the ‘Operating category’ that would otherwise be classified in the investing or financing categories.

- Following the new standard, each bank shall assess, based on its specific facts and circumstances, whether its investments in financial or non-financial assets represent its main business activities or not and it shall classify accordingly the income and expenses in the three new categories (operating, investing and financing).

- The operating category shall include all the income and expenses related to the main business activities of the institution.

- The investing category includes income and expenses relating to investments in assets that are not considered as main business activities, as well as the results of associates, joint ventures and unconsolidated subsidiaries accounted for using the equity method (IFRS 18.55(a)).

- The financing category includes income and expenses from liabilities arising from transactions that do not involve only the raising of finance (IFRS 18.59(b); IFRS 18.61; IFRS 18.B53-B54), like interest expenses on lease liabilities, the increase in the discounted amount of a provision arising from the passage of time, net interest expense (income) on a net defined benefit liability (asset) applying IAS 19.

- Regarding the income and expenses from cash and cash equivalents and from liabilities arising from transactions that involve only the raising of finance, IFRS 18 allows banks to classify them outside the operating category, provided that these income and expenses do not relate to the bank’s main business activity of providing financing to customers. However, in case of a retail and investment bank which also invests in financial assets as main business activity, all income and expenses from cash and cash equivalents and from financing liabilities are presumably classified in the operating category.

- IFRS 18 provides also guidance for the classification of income and expenses arising from hybrid contracts, income and expenses arising from derecognition and changes in classification, foreign exchange differences, and gains or losses on derivatives and hedging instruments. In such circumstances, the general principle is the classification of the income and expenses in the same category of the income and expenses to which they refer. For banks, this implies that most of these items should be classified in the operating category.

- IFRS 18 eventually provides for two new mandatory subtotals on the face of Statement of profit or loss: ‘operating profit or loss’ and ‘profit or loss before financing and income taxes’. However, the latter shall not be presented if a bank chooses to classify income and expenses from all financing liabilities in the operating category (IFRS 18.73 and IFRS 18.BC189). Additional items and subtotals can be included if such presentations are necessary for a primary financial statement to provide a ‘useful structured summary’ of the institution’s income and expenses (IFRS 18.24).

Proposed changes to the Finrep templates

- The Finrep statement of profit or loss is reshaped with the aim of minimizing the impact of the IFRS 18 implementation by requesting, to the extent possible, the same level of information as today, while ensuring a standardised presentation for all banks. To this end the main business activities of an investment and retail bank are considered as benchmark for reshaping the statement of profit or loss, in line with the IFRS 18 Illustrative Example II-4 ‘Statement of profit or loss for an entity that is an investment and retail bank that invests in financial assets as a main business activity and provides financing to customers as a main business activity’ (IFRS 18, IE 13).

- Following the benchmark model of a retail and investment bank, the income and expenses related to investments in subsidiaries, joint ventures and associates, investments properties and other non-financial assets (different from property, plant and equipment) are moved in the investing category.

- In the operating category, the content and the labels of some items are reviewed to clarify that they only include income and expenses related to the main business activities of an investment and retail bank.

- In the investing category, the income or expenses are grouped in the following new items: i) ‘Income or (-) expenses on investments in subsidiaries, joint ventures and associates’; ii) ‘Income or (-) expenses on investment properties and other non-financial assets’, and iii) ‘Income or expenses on investing financial assets’. The first two items mainly bundle income and expenses moved from the operating category, while the latter is added to deal with any (rare) situation where a bank only provides financing to customers but it does not invest in financial assets as main business activities.

- In the financing category, the new item of ‘Income or (-) expenses on non-operating liabilities’ shall include income and expenses arising from liabilities that are not related to the bank’s main business activities.

- Regarding the IFRS 18 other requirements on derivatives and hedge accounting, foreign exchange differences, hybrid contracts, derecognition and change in use, most of the related income and expenses should refer to items in the bank’s operating category. For this reason, the existing relevant rows of template F 02.00 are kept under the operating category. This approach aims at ensuring continuity with the past. However, should these income and expenses refer to items outside the operating category, Finrep instructions specify that banks shall report these income and expenses in new residual rows (i.e. ‘other income or expenses on investing non-financial assets’; ‘income or expenses on investing financial assets and on any related financial instruments’; ‘income or expense on non-operating liabilities’) created under the new categories of investing or financing, as appropriate.

- A similar approach is adopted to deal with any situation where banks’ main business activities deviate from those of an investment and retail bank used as a benchmark for reshaping template F 02.00. For example, if a bank assesses that its investments in non-financial assets (like commodities or carbon credits) are part of its main business activities, the related income and expenses shall be included in the residual items of ‘Other operating income/expense’. Furthermore, in case where a bank only provides financing to customers and it does not invest in financial assets as a main business activity, the income and expenses related to the investment in financial assets will be presented in the residual row of ‘income or expenses on investing financial assets and on any related financial instruments’ under the investing category, rather than in the specific rows of the operating category.

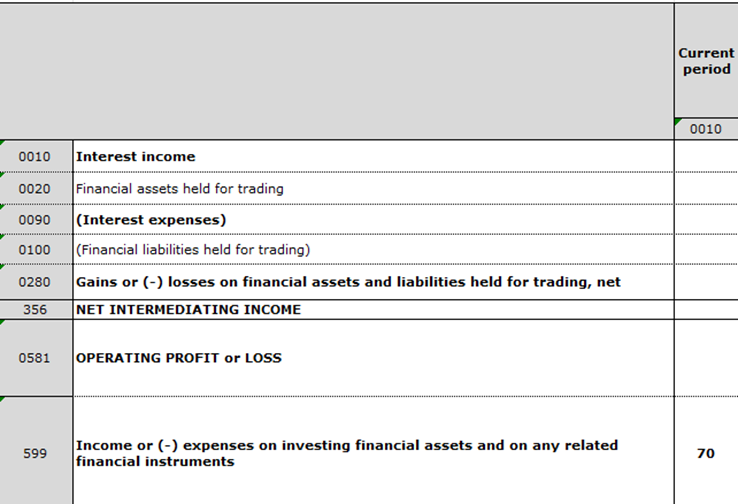

- Regarding the subtotals of template F 02.00, in addition to the inclusion of the IFRS 18 mandatory subtotal of ‘Operating profit or loss’, the existing ‘Total operating income, net’ is replaced by ‘Net intermediate income’, and the subtotal ‘Operating and investing profit or loss’ is added to provide a ‘useful structured summary’ of the institution’s income and expenses.

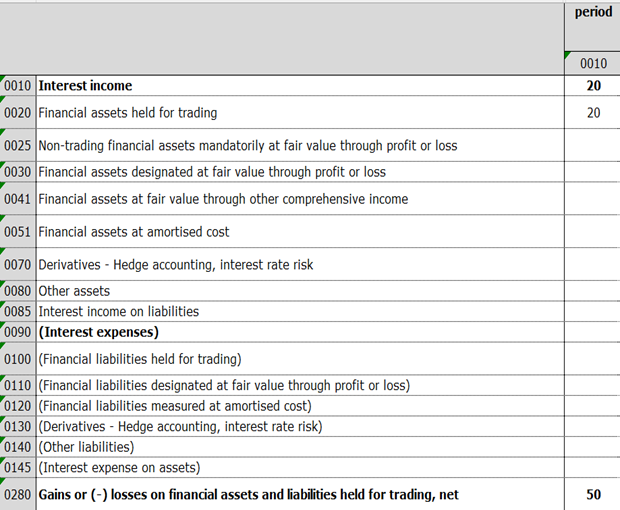

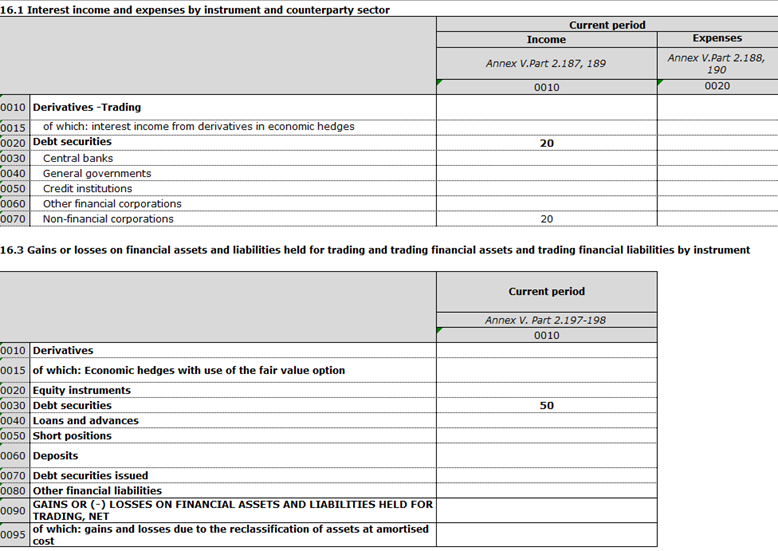

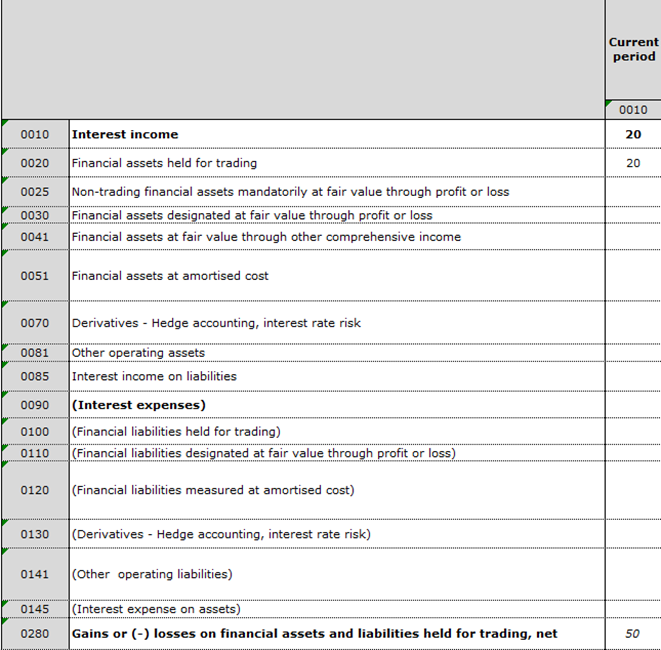

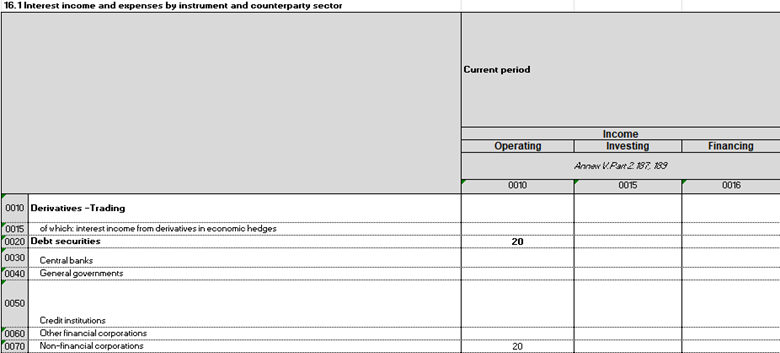

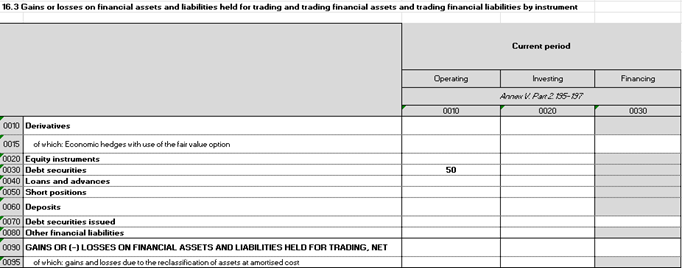

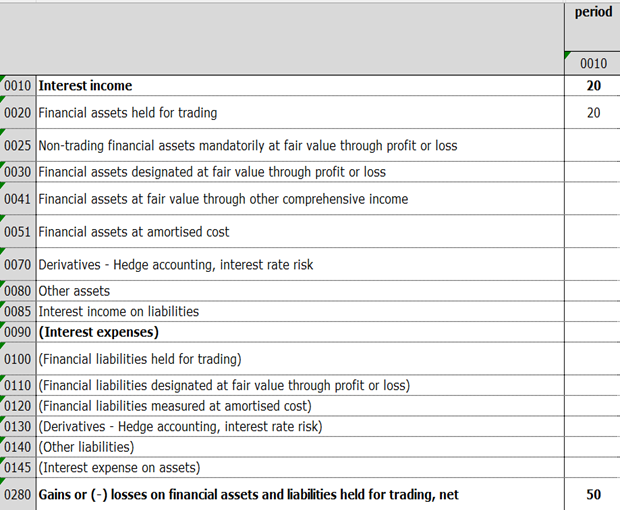

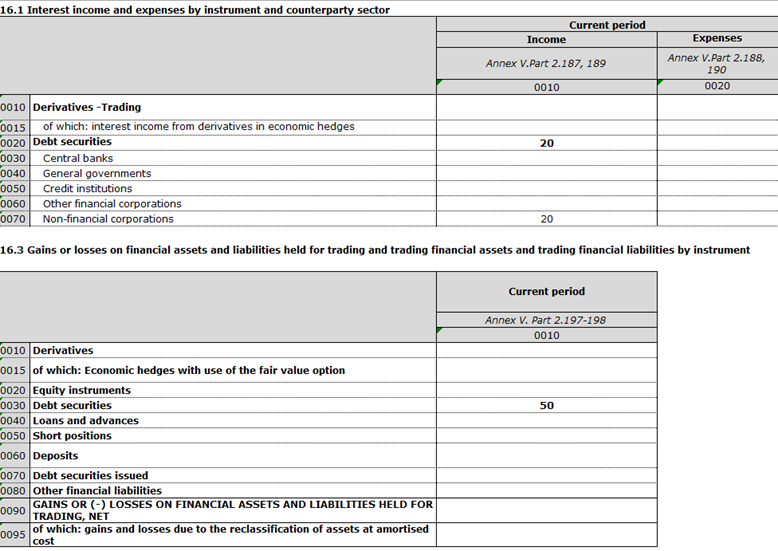

- Templates F 16 and F 45 are also reviewed to reflect the changes of IFRS 18. Specifically, columns for the new categories of operating, investing and financing are added to allow banks to report the same level of information as today, regardless of where the information is presented in the statement of profit or loss. The aim is to keep the same level of granularity as today, regardless of the banks’ assessment of main business activities. Therefore, even when the information is aggregated and presented in the new residual items of the template F 02, institutions shall keep reporting the details of the information as today in templates F 16 and F 45.

- As per article CRR 430(9), Finrep also includes templates and instructions for reporting financial information under national Generally Accepted Accounting Principles (GAAP) in accordance with Directive 86/635/EC (BAD). The changes to the Finrep framework stemming from IFRS 18 do not have any major impact for NGAAP reporters based on BAD (‘non-IFRS compatible). Therefore, NGAAP reporters non-IFRS-compatible will continue to present the information on income and expenses as today, in accordance with the provisions of the applicable Banking Accounting Directive (BAD).

- The following table shows a reconciliation between the current rows of Finrep template F 02.00 with the rows of the proposed Finrep template F 02.00 due to the IFRS 18 implementation to facilitate the reading of the changes.

Finrep 3.0 (F 02.00) | Finrep Draft Release (IFRS 18 implementation in F 02.00) |

| ||

Row | Label | Row | Label | Change type |

0080 | Interest income on other assets | 0081 | Interest income on other operating assets | IFRS: Label and content changed |

0140 | Interest expense on (Other liabilities) | 0141 | (Interest expense on other operating liabilities) | IFRS: Label and content changed |

0192 | Dividend income on Investments in subsidiaries, joint ventures and associates accounted for using other than equity method | 0192 | Dividend income on Investments in subsidiaries, joint ventures and associates accounted for using other than equity method | Kept for NGAAP |

0591 | Dividend income on investments in subsidiaries, joint ventures and associates accounted for using other than equity method | IFRS: moved in the investing category | ||

0320 | Gains or (-) losses on derecognition of investments in subsidiaries, joint ventures and associates, net | 0320 | Gains or (-) losses on derecognition of investments in subsidiaries, joint ventures and associates, net | Kept for NGAAP |

0593 | Gains or (-) losses on derecognition of investments in subsidiaries, joint ventures and associates, net | IFRS: moved in the investing category | ||

0330 | Gains or (-) losses on derecognition of non-financial assets, net | 0330 | Gains or (-) losses on derecognition of non-financial assets, net | Kept for NGAAP |

0331 | Gains or (-) losses on derecognition of property, plant and equipment or intangibles, net | IFRS: Kept only the derecognition of PPT and intangibles in the operating category and moved the derecognition of other non-financial assets in the investing category | ||

0597 | Gains or (-) losses on derecognition of investment properties and other non-financial assets, net | IFRS: Moved in the investing category | ||

0340 | Other operating income | 0340 | Other operating income | IFRS: Instruction for IFRS changed |

0350 | (Other operating expenses) | 0350 | (Other operating expenses) | IFRS: Instruction for IFRS changed |

0355 | TOTAL OPERATING INCOME, NET | 0356 | NET INTERMEDIATE INCOME | IFRS: Label and content partially changed |

0410 | (Depreciation on investment property) | 0410 | (Depreciation on investment property) | Kept for NGAAP |

0595 | (Depreciation on investment property) | IFRS: Moved in the investing category | ||

0420 | Depreciation on (Other intangible assets) | 0420 | (Depreciation on other intangible assets) | Kept for NGAAP |

0421 | (Depreciation on intangible assets) | IFRS: Label changed | ||

0510 | (Impairment or (-) reversal of impairment of investments in subsidiaries, joint ventures and associates) | 0510 | (Impairment or (-) reversal of impairment of investments in subsidiaries, joint ventures and associates) | Kept for NGAAP |

0592 | (Impairment or (-) reversal of impairment of investments in subsidiaries, joint ventures and associates) | IFRS: Moved in the investing category | ||

0540 | (Impairment or (-) reversal of impairment of investment property) | 0540 | (Impairment or (-) reversal of impairment of investment property) | Kept for NGAAP |

0596 | (Impairment or (-) reversal of impairment on investment property) | IFRS: Moved in the investing category | ||

0560 | (Impairment or (-) reversal of impairment of other intangible assets) | 0560 | (Impairment or (-) reversal of impairment of other intangible assets) | Kept for NGAAP |

0561 | (Impairment or (-) reversal of impairment of intangible assets) | IFRS: Label changed | ||

| 0581 | OPERATING PROFIT or LOSS | IFRS: New subtotal added | |

0582 | Income or (-) expenses on investments in subsidiaries, joint ventures and associates | IFRS: Added as new aggregating item | ||

0590 | Share of the profit or (-) loss of investments in subsidiaries, joint ventures and associates accounted for using the equity method | 0590 | Share of the profit or (-) loss of investments in subsidiaries, joint ventures and associates accounted for using the equity method | IFRS: Included in the new aggregating item |

| 0594 | Income or (-) expenses on investment properties and other non-financial assets | IFRS: Added as new aggregating item | |

| 0598 | Other income or (-) expenses on investing non-financial assets | IFRS: Added as a residual item | |

| 0599 | Income or (-) expenses on investing financial assets and on any related financial instruments | IFRS: Added as new item under the investing category | |

600 | Profit or (-) loss from non-current assets and disposal groups classified as held for sale not qualifying as discontinued operations | 600 | Profit or (-) loss from non-current assets and disposal groups classified as held for sale not qualifying as discontinued operations | IFRS: Kept as it is |

| 0601 | OPERATING and INVESTING PROFIT or LOSS | IFRS: Added as subtotal of Operating + Investing category | |

| 0602 | Income or (-) expenses on non-operating liabilities | IFRS: Added as new item for the financing category | |

1.2.2 Collateral additional information

- In the context of the regular Credit Risk Supervisory Review and Evaluation Process (SREP), supervisors have further investigated the role of collateral as credit risk mitigator and they have identified a lack of comparability and consistency in the collateral data collected, as well as differences in recovery rates across institutions and across member states, mainly due to differences in jurisdiction frameworks, prudential requirements, valuation and accounting practices.

- The proposal for changes to the ITS aims at strengthening supervisors’ ability to assess and monitor the quality of collateral, enabling a more focused benchmarking and identifying any institutions’ weak risk management practices related to collateral.

- To this purpose, the amended reporting requirements envisage the following elements:

- enhanced definition of ‘maximum amount of the collateral that can be considered’;

- separation of the information on collateral and guarantee received between performing and non-performing exposures;

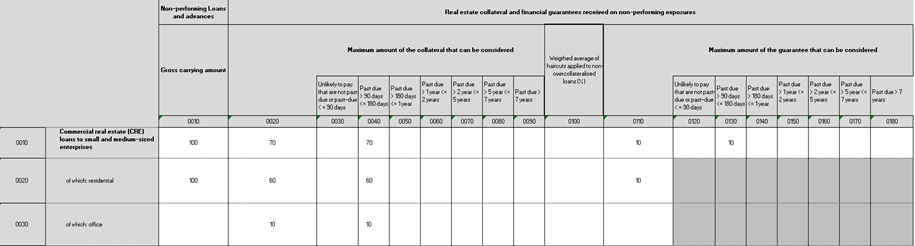

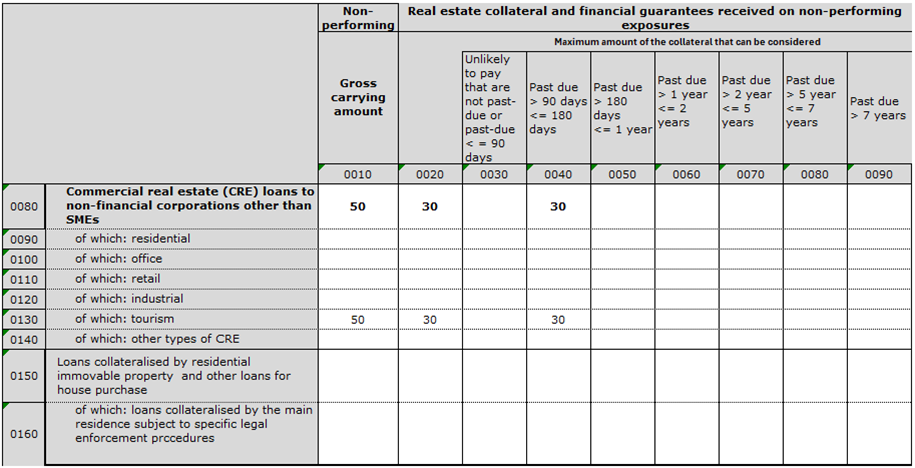

- enhanced information on LTV for commercial real estate (CRE) loans;

- new information on real estate collateral and guarantees received, with a breakdown by past-due days buckets of relevant non-performing exposures and a breakdown by type of real estates, information on the weighted average of haircuts applied to the collateral value and a breakdown by valuation methods used for collaterals received.

- The definition of ‘maximum amount of the collateral that can be considered’ is improved to clarify that institutions shall refer to the latest available collateral value that is used for the purpose of impairment calculation, after the application of any haircut by them, and in accordance with the applicable accounting framework, as well as with any applicable guidance issued by the relevant Competent Authority. This enhanced definition is included in the instructions to Finrep reporting and it should foster consistency in the collateral valuation and then increase the reliability of data reported by institutions.

- Template F 13.01 ‘Breakdown of collateral and guarantees by loans and advances other than held for trading’ is split into two templates (F 13.01.1 and F 13.01.2) to distinguish the information between performing and non-performing exposures. This separation addresses the issue of current limited data available for non-performing exposures, for whom a more granular analysis of collateral received is particularly important for the calculation of impairment and of recovery rates.

- In template F 18.02 ‘Commercial Real Estate (CRE) loans and additional information on loans secured by immovable property’, the information on ‘loans for which LTV ratio is not available or cannot be calculated’ is added to distinguish these cases from loans where the LTV is below 60%. Indeed, supervisors have observed that some institutions do not have the LTV data readily available yet for the reporting dates, and in case any LTV data is not available/cannot be calculated, the current structure of the template suggests that for this part of the loan portfolio the LTV is below 60% which might be false.

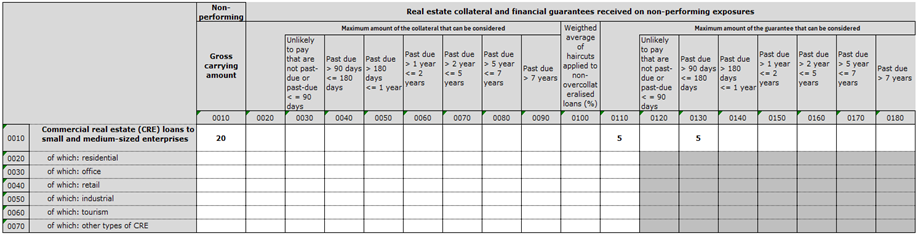

- The information on real estate collateral and guarantees received is included in two new templates: F 37.00 ‘Additional information on real estate collateral and financial guarantees received on non-performing loans’ with semi-annual frequency, and F 48.00 ‘Breakdown of real estate collateral received by type of valuation and by type of valuer- non-performing loans’ with annual frequency.

- These new templates provide further insights into the quality of real estate collateral and guarantee received on non-performing exposures and a comprehensive view on the coverage of different types of real estate collaterals. Specifically, in template F 37.00, the request of more granular information on different types of real estate collaterals and its breakdown by past-due days buckets of related non-performing exposures will allow supervisors to obtain information on the different levels of collateral liquidity and identify the collateral that is potentially not recoverable anymore. In addition, the information on the weighted average of haircuts applied by institutions, broken-down by type of real estate collaterals helps identify any discrepancies between the level of haircuts and their recovery rates. Template F 48.00 completes the analysis of collateral by providing further insights into the valuation methods applied and the types of valuer (internal or external) used for the real estate collateral valuation.

- Proportionality is implicit in the new reporting requirements that are triggered by the lending activities in the real estate sector carried out by institutions. In addition, the new information on real estate collateral and guarantees received is proposed to be reported by institutions other than small and non-complex institutions to limit the reporting efforts for the latter.

1.2.3 Information on other financial corporations

- Non-Bank Financial Intermediation comprises various financial sectors including both regulated and unregulated entities, such as asset management companies and investment funds, non-bank investment firms, pension funds, insurance companies, and other financial intermediaries.

- Banks and non-bank financial intermediaries (NBFI) are closely interlinked, with increasing tendency across many instruments (e.g. debt securities, equity instruments, loans, deposits, derivatives) that might be a source of vulnerability in times of turmoil.

- As of December 2023, EBA estimates the asset exposure of banks towards NBFI at 9.2% of total assets (EUR 2.5 trillion), while the liability exposure of banks towards NBFI funding at 10.3% of total assets (EUR 2.8 trillion). This is also reflected in off-balance sheet exposures, with undrawn loan commitments, financial guarantees and other commitments extended to NBFIs amounted to 6.4% of all EU/EEA banks off-balance-sheet items, while those received from NBFIs amounted to 9% of all EU/EEA banks off-balance-sheet items[2].

- In 2024, the European Commission conducted a consultation on risks and vulnerabilities posed by NBFI and the adequacy of the related macroprudential policies. The results of this consultation were published in March 2025[3]. Regarding the interlinking between banks and NBFI, several respondents to this consultation stressed the importance of effective supervision and data sharing to monitoring emerging risks from interconnectedness. Some national and EU public authorities suggested that greater transparency and data collection on NBFI-bank interactions is needed to monitor emerging risks effectively.

- The current reporting data on banks’ exposures towards NBFI and their granularity are very limited and further requests of data by the Commission to the European Supervisory Authorities (ESAs) are expected to properly monitor the phenomenon in the upcoming years.

- Against this background, new reporting requirements are introduced in Finrep. Nevertheless, simplification and proportionality are considered in developing the new templates by focusing only on the information that is strictly necessary for supervisory purposes.

- In particular, the three new templates include minimum information on banks’ financial assets, financial liabilities and off-balance sheet items towards ‘other financial corporations’, broken-down by type of subsectors and by classes of instruments. In addition, the information on the exposures towards those financial corporations that are primarily involved in private credit activities, such as private credit funds or business development companies (BDCs) is included.

- In order to facilitate the implementation of the new templates and alleviate the related reporting efforts for institutions, the breakdown by subsectors of ‘Other financial corporations’ is based on the current definition of ‘Other financial corporations’ included in the IT solutions to the ITS on reporting (Annex V, Part 1, par 42(d)), while the breakdown by classes of instruments is largely based on the information currently reported in the templates F 04 ‘Breakdown of financial assets by instrument and by counterparty sector’, F 08 ‘Breakdown of financial liabilities’ and F 09 ‘Loan commitments, financial guarantees and other commitments’. .

- The new templates are proposed to be requested with the same quarterly frequency of the existing templates F 04, F 08 and F 09. Proportionality is considered by requiring these new templates to institutions other than small and non-complex institutions, when their financial assets towards ‘other financial corporations’ exceed the threshold of 5% of their total financial assets. The threshold of 5% has been calibrated considering the bank’s reporting data as of December 2024 and it would allow to cover almost the total institutions’ exposures to NBFI, excluding smaller banks and banks with limited exposures to NBFI.

1.2.4 Information on crypto-assets

- Since 2024, supervisors have raised the need of data on digital transformation to properly monitor the relevant emerging risks for institutions, specifically regarding investments in crypto-assets.

- Although there is not a legal or commonly accepted definition of crypto-assets, the latter commonly refer to instruments characterized by the use of ‘blockchain technology’ including, for example, Bitcoin, Ethereum, stablecoin, asset token, utility token. This technology can support various rights and obligations of the holder that are reflected in different possible accounting treatments of crypto-assets in the financial statements.

- The IFRS Interpretations Committee (IFRS IC) has given some directions for the accounting treatments of those crypto-assets that meet the following conditions[4]:

- they are digital or virtual currencies recorded on a distributed ledger that uses cryptography for security;

- they are not issued by a jurisdictional authority or other parties;

- they do not give rise to a contract between the holder and another party.

- For this type of crypto-assets, the IFRS IC excludes the possibility of considering them as cash or cash equivalent or as financial instruments but believes that they meet the definition of an intangible asset. Therefore, the entities can apply the accounting standard IAS 38 ‘Intangible assets’ or in case of crypto-assets held for sale in the ordinary course of business, the accounting standard IAS 2 ‘Inventories’.

- Regarding other types of crypto-assets, in lack of a specific accounting standard, the guidance included in IAS 8 ‘Basis of preparation of financial statements’ should be followed and an analysis of the underlying rights and obligations linked to the holding of the crypto-assets is needed to determine the appropriate accounting treatment. For example, some stablecoins might meet the definition of a ‘financial asset’ if they give the holder a right to receive cash or other financial assets, and so they should be accounted for under IFRS 9, while ‘utility tokens’ that give the holder a right to access to future goods or services might meet the definition of an intangible asset of IAS 38.

- Against this background, basic information on the institutions’ level of activities in crypto-assets is included in Finrep, while considering the overarching principle of simplification and proportionality In particular, new rows are added in templates in F 22.01 ‘Fee and commission income and expenses by activity’ and in F 22.02 ‘Amount of assets involved in the services provided’ for the crypto-assets services as defined in Regulation (EU) 2023/1114 on markets in crypto-assets (MICAR). A new template F 38 ‘Information on crypto-assets’ is proposed to add to cover information on the different accounting portfolios where the crypto-assets can be allocated.

- In the new template, crypto-assets are classified into the following three categories:

- Electronic money token (EMT) as defined by the Regulation (EU) 2023/1114 on markets in crypto-assets (MICAR);

- Asset-referenced token (ART) as defined by the Regulation (EU) 2023/1114 on markets in crypto-assets (MICAR);

- Other crypto-assets, different from EMT and ART, like stablecoins not compliant with MICAR and crypto-assets out of the scope of MICAR, such as ‘utility token’ and ‘security token’ when they qualify as financial instruments as defined in the Directive 2014/65/EU (Mifid).

- The template also includes information on crypto-assets compliant with IFRS-IC definition and on derivatives with underlying crypto-assets, to give a complete picture of the institution’s exposures to crypto-assets.

- Proportionality is implicit in the new reporting requirements that are triggered by the activities in crypto-assets carried out by institutions. In addition, the new template is proposed to be reported by institutions other than small and non-complex institutions, with a semi-annual frequency.

1.2.5 Other adjustments

- Other adjustments to the templates and related instructions are driven by different needs:

- regularly update of the reporting requirements when the underlying legal framework changes;

- experience in using financial information for supervision purposes;

- experience with data quality and feedback from institutions compiling data.

- incorporation of guidance and clarifications coming from Q&As published on the EBA website where relevant for a more complete and seamless application of the single rulebook;

- Regarding the adjustments due to changes of the underlying legal framework, in template F 01.01 ‘Assets’, goodwill is now reported separately from the ‘intangible assets’ in accordance with the provisions of IFRS 18.

- In templates F 03 ‘Statement of comprehensive income’ and F 46 ‘Statement of changes in equity’, information on equity instruments measured at fair value through other comprehensive income is added to implement the amendments to IFRS 7, paragraphs 11A (f) and 11B (d) on disclosures of equity instruments measured at fair value through other comprehensive income. These amendments were issued by the IASB in May 2024 and endorsed by the European Commission in May 2025 with first application for reporting periods beginning on or after 1 January 2026. However, the first application date of these changes in Finrep will be aligned with the first reference date of the rest of Finrep package.

- In the general instructions to Finrep (IT solutions – Annex V, Part 1, paragraph 5 (i)), the definition of ‘micro, small and medium-sized enterprises’ (‘SME’)’ is changed to consider the CRR3 definition that is also used in Corep. In addition, in the instructions to template F05.01 ‘Loans and advances other than held for trading, trading or held for sale assets by product’, the definition of ‘specialised lending’ is specified by including project finance, object finance, commodity finance and income-producing real estate (IPRE), in line with the amendments to the CRR article 147(8). Finally, in the instructions to templates F 09 on loan commitments, financial guarantees and other commitments, the legal references and the wording are adjusted to consider the CRR 3 amendments to Annex I and the CRR article 111 (4).

- Regarding the changes linked to the experience in using Finrep for supervision purposes, in template F 12.01 ‘Movements in allowances and provisions for credit losses’, the information on overlays is added. Overlays are defined as post-model adjustments for the estimation of expected credit losses under IFRS 9. They became common practice during the Covid-19 crisis, and now they are extensively used to cover novel risks like energy supply, supply chains in general, environmental risks, inflation and geopolitical risks, not easily captured by IFRS 9 models. The introduction of minimum information on overlays in Finrep will therefore allow supervisors to better monitor the modelling aspects of IFRS 9 ECL calculation and their related impact on credit risk allowances, while considering the overarching principle of simplification.

- In template F 18.00 ‘Non-performing exposures’, information on loans subject to public Guarantee Scheme (PGS) is added. The PGS became common practice during the Covid-19 crisis when the relevant data on PGS were also collected. After the Covid-19 pandemic, the data collection on PGS was stopped. Notwithstanding, some member states have started to set up PGS to face emerging risks, like those related to energy crisis and to the breakout of the Russian war. The introduction of essential information on loans subject to PGS in template F 18.00 aims at giving supervisors indications on the impact of these measures on the institutions’ lending activities and the related asset quality, while considering the overarching principle of simplification.

- In templates F 40 on ‘Group structure’, the information on ‘type of code’ is enhanced by providing a hierarchy of pre-defined detailed code lists to be used when entities’ LEI codes are not available. The aim of this enhancement is to facilitate the integration with statistical reporting and ESCB/SSM datasets and improving the data quality.

- In template F 41.01 ‘Fair value hierarchy: financial instruments at amortised cost’, information on the carrying amount of hedging derivatives in offsetting unrealized losses or gains on the hedged instruments is added. This information is particularly relevant in the context of current volatility in interest rates—both upward and downward movements where supervisors have a recurring need to monitor unrealised gains and losses. For this reason, the frequency of this template has been also increased from annual to quarterly.

- Finally, the following table summarize the Q&As published that are incorporated in the proposal of Finrep review and other adjustments related to the experience with data quality and feedback from institutions compiling data, notably the extra data quality checks (EGDQ) regularly published by ECB.

Templates and instructions | Q&As and extra data quality checks (EGDQ) | Proposed amendments |

F 12.01 Annex V Part 2, par 160 | Published Q&As: - 2021_5840 | In template F 12.01, the column "Decreases due to derecognition" shall also include the transfer in non-current assets and disposal groups classified as held for sale. |

F 22.02 Annex V Part 2, par 285(h) | Published Q&As: 2022_6598 | In template F 22.02, a row is added for 'loans servicing activities' with related instructions. |

F 25.01 Annex V Part 2, par 347 | Rejected Q&As: 2020_5576 | In template F 25.01, Row 0080: "Profits/(-) losses from sale of collateral obtained by taking possession" is renamed to: "(-) Profits/(+) losses from sale of collateral obtained by taking possession" and the instructions are changed accordingly. |

F 01.01 Annex V Part 2, par 2 | Rejected Q&As: 2022_6352 Published Q&A: 2025_7568 | Clarification in the instructions that compulsory reserves are excluded from "Cash balances and central banks" and they shall be reported as 'loans and advances' in the accounting portfolios “financial assets at amortised cost” for IFRS institutions, or “non-trading non-derivative financial assets measured at a cost-based method” for NGAAP institutions. Also, a clarification on the nature of cash balances is also added "...shall be readily available at all times" |

F 24.01/ F 18.01 Annex V Part 2, par 239vi, 328i | Published Q&As: -2019_5066 -2020_5613 Rejected Q&As: -2021_5687 | In the instructions to template F 18.01, a clarification on the reporting in case of reclassification of the counterparty sector (e.g. from large corporation to SME) during the period is added. In template F 24.01, two rows 0015 and 0016 are added to consider the effects of changes in classification of the counterparties with related instructions. In particular, when a counterparty changes its classification during the period, the opening balance shall be adjusted by adding/removing the amount previously considered in the former classification by using the row ‘Effects of changes in classification of the counterparties’. |

| Annex V, Part 2, par 88(a) | Published Q&A: - 2020_5167 - 2021_6219 EGDQ | In the instructions, clarification on the definition of 'credit for consumption'. |

F 25.01 Annex V Part 2, par 346 | Published Q&A: 2023_6823 EGDQ | In template F 25.01, a row is added to consider "Outflow due to reclassification to PP&E" with related instructions. |

F 19 Annex V Part 2, par 260 | Published Q&A: 2015_1842 2014_736 2014_878 | In the instructions to template F 19.00. clarification is added in case of additional forbearance measures granted to performing exposure. In that case, the probation period is not discontinued, unless the additional forbearance measures lead the exposure to be classified as non-performing. |

F 26 Annex V Part 2, par 360(a)(ii), 360(b) | Published Q&A: 2020_5239 | The instructions were improved to specify that “cure period” refers to the 1-year period necessary for non-performing forborne exposures to become performing forborne exposures, while the 'probation period' refers to the 2-years necessary for performing forborne exposures to become performing exposures. |

F 46.00 Annex V Part 2, par 317 | Published Q&A: 2022_6520 2023_6834 2024_7005 EGDQ | Instructions is added to specify that if the functional currency of an entity differs from the euro, the foreign exchange differences related to capital and share premium that arise in the preparation of FINREP shall be included as components of other comprehensive income. Consequently, these differences must be reported as “Accumulated other comprehensive income” under “Other increase or (-) decrease in equity”. |

F 22.02 Annex V Part 2, par 285 (e) | Published Q&A: 2020_5399 2014_1535 | Improvements on the definition of 'Payment services' in the instructions, following the PSD Directive. In particular, ‘Payment services’ shall refer to payments collected on behalf of the customers during the period while providing the services listed in Annex I of the Directive (EU) 2015/2366. The debt instruments by which the payments are generated shall be neither recognised on the balance sheet of the institution nor originated by it. |

| F 18, F 19 | Published Q&A: 2018_3930 2014_1055 | In template F 18.00, cells currently greyed-out shall be open (from rows 211 to 231 under columns 122 and 140) and the following cells shall be greyed-out (r340-400; c205 and c210); (r480-540; c205 and c210) In template F 19.00, cells currently greyed-out shall be open (from rows 211 to 231 under columns 100 and 130) and the following cells shall be greyed-out (r340; c180 and c185). |

| F 46 | Published Q&A: 2020_5301 | Cell (r0130, c0020) is open for reporting of profit/loss from trading of own shares. |

| Annex V, Part 1, par 5(i) and Part 2, par 89 | Published Q&A: 2024_7139 2024_7164 | The definition of 'SME' is changed to be consistent with Corep by referring to Article 5(9) CRR. For the definition of 'Project finance loans', a reference to Article 147(8) CRR is added to consider all the different categories (project finance, object finance, commodity finance, income-producing real estate). |

| Annex V, Part 1, par 42(e) | Rejected Q&A: 2025_7379 | Clarification that the sector of 'non-financial corporations' includes also self-employment activities, except for the case specified in Part 1 2.119(d) of ESA 2010 that are treated as ‘Households’. |

| F 40, Annex V Part 2, par 294 | Published Q&A: 2016_2820 2013_574 | Clarification in the instructions that all entities included in the group structure shall be reported, regardless of the activity they perform and regardless of the accounting portfolio in which the participation is included in the accounting scope of consolidation. However, the reporting agent and branches shall not be included. |

| F 40.1, Annex V Part 2, par 296 (q) | Published Q&A: 2014_1222 | Clarification in the instruction on the definition of 'acquisition costs' in case of a partial sale of a subsidiary without losing the control and in case of constitution of a subsidiary |

| Annex V, Part 2, par 86(b), par 173(b)(iv) | EGDQ | Clarifications in the instructions that 'other collateralised loans' include pledges of securities, cash, and other collateral, regardless of the legal form of the collateral and also regardless of whether the obligor has the right to sell/transfer/dispose the collateral, without seeking prior permission of the lender (fixed and floating charges). |

| Annex V, Part 2, par 298 | EGDQ | Addition of a reference to IFRS 7.25 and clarification that where an exception applies under IFRS 7.29(a), values shall be reported based on the carrying amount. |

F 16.01 Annex V, Part 2, par 194 | Q&A 2022_6350 | Amendments coherently with the Q&A: for assets not classified as credit impaired anymore at the reporting reference date, the related interest income is not reported in row 0280 "Of which: interest income on impaired financial assets" |

F 31.01 Annex V Part 2 par 289 | Q&A 2016_2032 related parties | Added a clarification on what needs to be reported under column 0010 "Parents and entities with joint control or significant influence" and column 0020 "Subsidiaries and other entities of the same group". |

| F18.00, F 18.02, F 23.02, F 23.04 | Q&A 2021_6050 | Term "material" added to the past due breakdown of F18.00, F18.02 and F23.02, F 23.04 (Annex V, Part 2 par 236) in order to distinguish from the breakdown by past due in F 7.01 |

2 Transitional arrangements for IFRS 18 implementation

- IFRS 18 has been endorsed by Commission Regulation (EU) 2026/338and it will be mandatory for public consolidated financial statements of institutions using the IFRS from the reporting periods beginning on or after 1 January 2027.

- The timely implementation of IFRS 18 in Finrep would significantly reduce the risk of double or divergent reporting for IFRS institutions, as also highlighted by EFRAG in its endorsement advice to the EU Commission in May 2025: “For financial institutions, the costs to be incurred, both one-off and ongoing, depend entirely on the level and timing of potential harmonisation of the local regulatory requirements with those of IFRS 18. Financial institutions are subject to Finrep reporting requirements. Unless FINREP is harmonised with IFRS 18, they would be subject to different reporting requirements/double reporting requirements.

- Considering the timing of the introduction of the changes to the overall Finrep reporting, a shorter one-month public consultation is provided for the templates and instructions mainly affected by the IFRS 18 implementation (i.e. F 02.00, F 16.01, F 16.02, F 16.03, F 16.04, F 16.04.1, F 16.05, F 16.06, F 16.07, F 45.02, F 45.03, F 20.03), with the aim of publishing the final version of these templates and related instructions over the summer 2026, although their formal adoption by the EU Commission will follow the whole ITS. This should reduce the risk of double or divergent reporting for institutions implementing IFRS 18 in their public consolidated financial statements from the reporting periods beginning on or after 1 January 2027.

- An EBA decision will be published to specify the enforcement of the temporary use of these templates until the formal adoption by the EU Commission, together with clarifications on the first reference and remittance dates and the related technical package (DPM, taxonomies, validation rules) for the IFRS 18-mainly affected templates.

3 Accompanying documents

3.1 Draft cost-benefit analysis / impact assessment

As per Article 15 of Regulation (EU) No 1093/2010 (EBA Regulation), any draft implementing technical standards (ITS) developed by EBA shall be accompanied by an Impact Assessment (IA), which analyses ‘the potential related costs and benefits’.

This analysis presents the IA of the main policy options included in this Consultation Paper on the draft ITS amending Commission Implementing Regulation (EU) 2024/3117 on supervisory reporting referred to in Article 430 (7) of Regulation (EU) No 575/2013 concerning financial information (‘the draft ITS’). The analysis provides an overview of the identified problems, the proposed options to address this problem as well as the potential impact of these options. The IA is high level and qualitative in nature.

A. Problem identification and background

Article 430(7) of the Regulation (EU) No 575/2013 (‘the CRR’) mandates the EBA to ‘develop draft implementing technical standards to specify the uniform reporting formats and templates, the instructions and methodology on how to use those templates, the frequency and dates of reporting, the definitions and the IT solutions for the reporting (…).’. Under this mandate the EBA developed draft ITS, published by the Commission under the Commission Implementing Regulation (EU) 2024/3117 (‘CIR 2024/3117’) This regulation shall be updated whenever the underlying legal provisions change and in relation to the evolving supervisory needs.

The EBA originally chose to base the reporting of financial information (Finrep) on IFRS accounting standards. In April 2024, the International Accounting Standards Board (IASB) issued ‘IFRS 18 - Presentation and Disclosure in Financial Statements’, which supersedes the accounting standard ‘IAS 1 -Presentation of financial statements’ and introduces a defined structure for the statement of profit or loss. Therefore, an adaptation of the CIR 2024/3117 (i.e. in this case FINREP templates and instructions’ part) is necessary.

Furthermore, in accordance with Article 430 (5) CRR, the reporting on financial information needs to include the information to obtain a comprehensive view of the risk profile of institutions’ activities and a view of systemic risks posed by institutions to the financial sector or the real economy. In this respect, recent evolving supervisory needs, including monitoring emerging risks and experience with data quality and feedback received by the stakeholders over time also triggered a necessary review of some parts of the Finrep templates and instructions.

B. Policy objectives

The draft ITS amending Commission Implementing Regulation (EU) 2024/3117 on supervisory reporting referred to in Article 430 (7) of Regulation (EU) No 575/2013 concerning financial information aims at specifying Finrep uniform formats and definitions related to the changes triggered by IFRS 18 and by recent evolving supervisory needs.

C. Options considered, assessment of the options and preferred options

Section C. presents the main policy options discussed and the decisions made by the EBA during the development of the Draft ITS. Advantages and disadvantages, as well as potential costs and benefits from the qualitative perspective of the policy options and the preferred options resulting from this analysis, are provided.

C.1. IFRS 18 implementation

Implementation of IFRS 18

As mentioned above, the International Accounting Standards Board (IASB) issued ‘IFRS 18 - Presentation and Disclosure in Financial Statements’ in April 2024. This new standard has been endorsed by Commission Regulation (EU) 2026/338, and it will be applicable for reporting periods beginning on or after 1 January 2027. Regarding the modification – in the Draft ITS – of Finrep templates and instructions, the EBA considered two options.

Option 1a: Not incorporating IFRS 18 in the Finrep templates

Option 1b: Incorporating IFRS 18 in the Finrep templates

Not incorporating IFRS 18 into the Finrep templates would avoid certain implementation costs for IFRS reporting institutions. These costs arise primarily from different scopes of consolidation: for institutions using IFRS for consolidated public financial statements, the accounting scope of consolidation may diverge from Finrep’s prudential one and thus institutions would need to implement procedures to reprocess IFRS-based information, accordingly, resulting in initial one-off costs. Moreover, Finrep requires quarterly reporting, whereas public financial statements are typically disclosed less frequently, leading to increased ongoing costs. These burdens are not unique to IFRS 18 but apply more broadly to the implementation of IFRS requirements into Finrep. For N-GAAP institutions, the changes due to the IFRS 18 implementation are not applicable, therefore there is no impact on them.

However, implementing IFRS 18 into Finrep would significantly reduce the risk of double or divergent reporting requirements for IFRS institutions. As IFRS 18 becomes mandatory for public financial statements from the reporting period beginning on or after 1 January 2027, aligning Finrep with IFRS 18 would alleviate implementation costs and streamline reporting processes. This concern was also highlighted by EFRAG in its endorsement advice to the European Commission in May 2025: “For financial institutions, the costs to be incurred, both one-off and ongoing, depend entirely on the level and timing of potential harmonisation of the local regulatory requirements with those of IFRS 18. Financial institutions are subject to Finrep reporting requirements. Unless Finrep is harmonised with IFRS 18, they would be subject to different reporting requirements / double reporting requirements.” Furthermore, implementing IFRS 18 into Finrep is consistent with past practices and supports the broader objective of harmonizing supervisory reporting with international accounting standards. This approach enhances comparability, reduces duplication, and promotes regulatory efficiency across jurisdictions.

Based on the above, option 1b has been chosen as the preferred option, and the draft ITS will implement IFRS 18 into the Finrep supervisory reporting templates and related instructions.

Structure of Finrep statement of profit or loss (F 02.00)

In Finrep, template F 02.00 is the ‘Statement of profit or loss’ and is, as such, naturally concerned by IFRS 18. With regard to integration of IFRS 18 within this template, the EBA considered three options.

Option 2a: Keeping as much as possible the current structure of the template F 02.00 by considering, as reference, the IFRS 18 Illustrative Example No. 13 for a retail and investment bank

Option 2b: Developing different possible structures of template F 02.00 to be used in relation to the institutions’ assessments of their main business activities.

Option 2c: Considering a single structure of the template F 02.00 but duplicating some rows under the three new categories (operating, investing, financing) provided by IFRS 18 to reflect any different institutions’ assessments of their main business activities.

Developing different structures of template F 02.00 (Option 2b) or duplicating rows within a single template (Option 2c) would allow for a more tailored representation of income and expenses based on the specific business models of reporting institutions. These approaches could improve the relevance and transparency of the reported data for institutions whose activities differ significantly from those of a classic retail and investment bank as considered in the IFRS 18 Illustrative Example No. 13. However, they would also introduce complexity in the supervisory reporting framework, with the risk of reducing the standardisation having different ways of reporting the information of the income statement. This would also make the analysis and comparisons across institutions more complex.

By contrast, Option 2a, which retains as much as possible the current structure of template F 02.00 and uses the IFRS 18 Illustrative Example No. 13 as a reference, offers a more standardised and simplified approach. It reclassifies income and expenses into the three new IFRS 18 categories – operating, investing, and financing – based on the business model of a typical retail and investment bank that should be the most common one. This ensures continuity with the existing Finrep structure, as most current line items have been preserved under the new subtotal of the operating profit or loss. Only a limited number of new data points have been added to comply with IFRS 18 requirements.

This approach is expected to facilitate the implementation by institutions, as it builds as much as possible on current reporting practices. and supports the broader objective of harmonisation in supervisory reporting.

Nevertheless, the chosen approach introduces new residual line items to accommodate cases where an institution’s business model deviates from the one of a standard retail and investment bank taken as a reference to develop the new structure of template F 02.00. While this may reduce transparency in template F 02.00 and complicate comparisons across institutions in case of different business models, the loss of transparency in template F 02.00 is mitigated by keeping the current breakdowns in templates F 16 and F 45 but with the addition of columns in these latter templates to consider the three new IFRS 18 categories (operating, investing and financing) where the income and expenses are classified in relation to the institution’s business model.

Based on the above, option 2a has been chosen as the preferred option, and the draft ITS will retain the current structure of template F 02.00 as much as possible, using the IFRS 18 Illustrative Example No. 13 as a reference.

Subtotals in template F 02.00 (‘Statement of profit or loss’)

The EBA considered two options regarding the inclusion of new subtotals in template F 02.00:

Option 3a: In addition to new IFRS 18 mandatory subtotal “Operating profit or loss”, including new non-mandatory subtotals “Net intermediating income” (replacing the current “Total operating income, net”) and “Operating and investing profit or loss” in the template F 02.00

Option 3b: Including only the new IFRS 18 mandatory subtotal “Operating profit or loss”

Adding the subtotal “Net intermediating income” ensures continuity with current practice, as it replaces the existing subtotal “Operating income, net”, that is considered as a key metric since it allows to isolate institutions’ performance from their banking activities. This approach maintains consistency with current reporting.

Including the subtotal “Operating and investing profit or loss”, although not mandatory under IFRS 18, provides a structured summary of institutions’ financial performance from operating and investing activities. This is particularly relevant given that certain line items have been moved below “Operating profit or loss” in line with IFRS 18.

As such, even though introducing subtotals not strictly required by IFRS 18, tailoring the template with these subtotals enhances clarity and usefulness of financial reporting.

Based on the above, option 3a has been chosen as the preferred approach. The draft ITS will therefore include, in addition to new mandatory subtotal “Operating profit or loss”, the new subtotals “Net intermediating income” and “Operating and investing profit or loss”.

Breakdown of Selected Statement of Profit or Loss Items (Templates F 16 and F 45)

Templates F 16 and F 45 provide detailed breakdowns of selected profit or loss items. Regarding IFRS 18 integration in those templates, the EBA considered two options.

Option 4a: Keeping the current structure of templates F 16 and F 45 with minor adjustments to row labels, considering the business model of a retail and investment bank as reference (like template F 02.00).

Option 4b: Adding new columns to consider the three new IFRS 18 categories – operating, investing, and financing – in templates F 16 and F 45 to capture any possible deviations from the classic retail and investment bank business model used as a reference to develop the structure of the template F 02.00.

Keeping the current structure with minor label adjustments (Option 4a) would maintain simplicity and continuity and it would be in line with the approach used in template F 02.00. However, this approach assumes that most institutions follow the retail and investment bank model. For institutions with different business models, certain income and expenses could fall into residual line items of template F 02.00 and under Option 4a they would no longer be reported in templates F 16 and F 45, reducing transparency.

On the other hand, adding new columns for operating, investing, and financing (Option 4b) allows institutions to report detailed information regardless of their business model. This approach ensures that data classified under residual items in template F 02.00 can still be captured in templates F 16 and F 45. While reconciliation between templates F 02.00 and F 16/F 45 may become more complex for non-standard business models, this impact is expected to be limited since most institutions follow the retail and investment bank model.

Based on the above, option 4b has been chosen as the preferred option. The draft ITS will therefore provide the inclusion of new columns for operating, investing, and financing categories in templates F 16 and F 45.

C.2. Collateral

Additional Collateral Information in Finrep

Today, institutions report collateral-related information in several different Finrep templates. However, weaknesses have been identified in these templates’ information and related instructions. In this regard, the EBA considered two options.

Option 5a: Keeping the current level of detail of the Finrep collateral-related templates

Option 5b: Improving the definition of the collateral value and including new and amended collateral-related information

Keeping the current level of detail (Option 5a) would avoid additional implementation costs and preserve stability in reporting practices. However, this approach would not solve the issues faced by supervisors in carrying out their activities. Indeed, collateral plays a critical role as a credit risk mitigator, and a weak definition combined with insufficient details have led to a lack of consistency and comparability in collateral valuation across institutions and jurisdictions, which hinders effective supervisory analysis.

On the other hand, improving the definition of collateral value and introducing more granular breakdowns (Option 5b) would enhance data reliability and allow supervisors to perform meaningful benchmarking and identify lower-quality collateral. Under this option 5b, the proposed changes include: i) an improved definition of the ‘maximum amount of the collateral that can be considered’; ii) a more stringent definition of Loan-to-Value (‘LTV’) to distinguish cases where LTV is below 60% from cases where LTV cannot be calculated; iii)a breakdown of collateral received by performing status to enable in-depth analysis of collateral linked to non-performing exposures; and iv) two new templates including, among others, a breakdown of collateral received by Day-Past-Due (‘DPD’) buckets of the related exposures, (to enable the identification of collateral that is potentially non-recoverable), a breakdown by collateral type (to help supervisors understand which collateral is easier to realise), and information on the haircuts applied by institutions and recovered collateral values (to allow detection of discrepancies across institutions and across countries.