Consultation Paper on Revisions to the ITS on supervisory reporting (Commission Implementing Regulation (EU) 2024/3117) - Module on SNCIs process for P3DH

The content on these interactive pages is provided for ease of reference and to assist in the reading and understanding of the Consultation Paper and it is not considered as the official version of such documents.

For the formal consultation papers and their components, please refer to the .pdf documents provided at the bottom of this page. In case of discrepancies between these interactive pages and the .pdf documents, the latter prevail as the authentic official versions.

Responding to this consultationPlease provide your responses by 10 July 2026 at 23:59 CEST via EU survey (Password for the survey: Reporting2026). Late responses will not be considered. |

1 Background and rationale

- The Pillar 3 disclosure requirements are established under the Commission Implementing Regulation (EU) 2024/3172[1] with regard to public disclosures by institutions of the information referred to in Part Eight of the CRR (the comprehensive ITS on institutions’ public disclosures). As regards credit institutions, the EU Pillar 3 framework is complemented by the ITS on total loss absorption capacity (TLAC) and minimum requirement for own funds and eligibility liabilities (MREL) disclosure and reporting[2], which include in a single package the disclosure and reporting requirements on eligible liabilities (TLAC and MREL), following the mandates included in the Articles 430 and 434a of the CRR and Article 45i of Directive (EU) 2019/879 (BRRD2).

1.1 New banking regulatory package and Pillar 3 data hub

- Under CRR2[3] (in force until 9 July 2024), institutions were required to disclose Pillar 3 information in electronic format and in a single medium or location. In addition, institutions were also required to make this information available on their website or, in the absence of a website, in any other appropriate location.

- The CRR3[4] introduced new provisions on the means of Pillar 3 disclosures aim at enhancing market discipline by centralising disclosures of prudential information in a single access point established by EBA. This will facilitate access to prudential data and comparability across industry and is expected to further reduce the administrative costs related to disclosures for small and non-complex institutions (SNCIs). The CRR mandates the EBA, under Article 434, to publish in its website the Pillar 3 information required to be disclosed by credit institutions (‘Pillar 3 Data Hub’ or ‘P3DH’). The main benefits of the data hub are the following:

- Serve as a single platform for users of Pillar 3 information to have common access to the Pillar 3 reports and increase the use and re-use of data;

- Provide the possibility to download data simultaneously and promote data comparability in a harmonised format;

- Promote transparency and market discipline by being part of the overall EU strategy. P3DH will be a source of data to the EU strategic project European Single Access Point (ESAP).

- Since 26 January 2026, the P3DH is available for large and other institutions (here). In the case of SNCIs, its implementation is expected to reduce costs of compliance with Pillar 3 disclosure obligations given that the disclosure figures are required to be centrally computed by the EBA. Proportionality is a key principle for European legislators. Proportionality is embedded in the CRR from the beginning and further emphasised in the subsequent revisions, including CRR2 and CRR3. The EBA was mandated under the CRR 2 to measure and gain insights into the costs that institutions incur when complying with the supervisory reporting requirements, and in particular with those set out in the EBA’s ITS on supervisory reporting. Based on that assessment, the EBA made recommendations on how to reduce reporting costs, particularly for SNCIs. The findings from this analysis were included in the EBA study on the cost of compliance with supervisory reporting requirements, published in 2021. The conclusions and recommendations included in this report have been present in the EBA work on successive framework releases since the publication of the report. In the same vein, proportionality has been considered when defining the proposed process to SNCIs that will be soon subject to a short consultation process.

- In line with the CRR mandate, the EBA will publish on its website the required Pillar 3 disclosures for SNCIs based on the information these institutions report to their respective Competent Authorities, in accordance with Article 430 of the Regulation. In practice, this means that the EBA will use supervisory reporting data to produce the quantitative Pillar 3 disclosures for SNCIs. This approach differs from the process applied to large and other institutions, which must submit their already processed Pillar 3 disclosure reports, which the EBA then publishes without further transformation.

1.2 Mapping between disclosures and reporting

- The comprehensive ITS on institutions’ public disclosures encompasses fixed templates to implement quantitative disclosure requirements and flexible tables for the qualitative disclosures, with detailed instructions on the type of information to be provided. The disclosure formats are kept consistent with Basel Committee on Banking Supervision’s (BCBS) Pillar 3 principles and standards[5] to facilitate the comparability of information. The P3DH centralises and makes publicly available the information of the credit institutions on the basis of the templates and tables as defined under the Pillar 3 ITS. This is already done for large and other institutions and is under development for SNCIs.

- No new Pillar 3 disclosure requirements are established with the implementation of the P3DH, whose purpose is to make the data available on a centralised manner with the existing prudential requirements under the EBA Pillar 3 ITS.

- The disclosure requirements are aligned, to the possible extent, with the supervisory reporting framework. This implies that most of the quantitative information disclosed by institutions can be easily derived from supervisory reporting. In this regard, a mapping between disclosure and reporting data is developed and published by the EBA[6]. The EBA started to publish this tool on its own initiative when implementing the CRR2. The tool has been very well received and praised by reporting institutions and the CRR3 mandates the EBA to keep the tool updated and publicly available. In addition to the mapping tool, the EBA made also available a signposting tool[7] designed to support institutions in determining the applicable requirements based on their size and complexity and other relevant characteristics. Neither the mapping tool nor the signposting tool replaces the legal text. In case of uncertainty, the provisions set out in the legislation prevail.

- To note, SNCIs will be subject to additional requirements on disclosures as per the amendments to supervisory reporting framework being consulted in this consultation paper. In practice, listed SNCIs will have additional requirements on shadow banking and ESG while non-listed SNCIs will be subject to additional ESG requirements only.

1.3 Overview of Pillar 3 requirements for SNCIs and considerations on proportionality and simplification

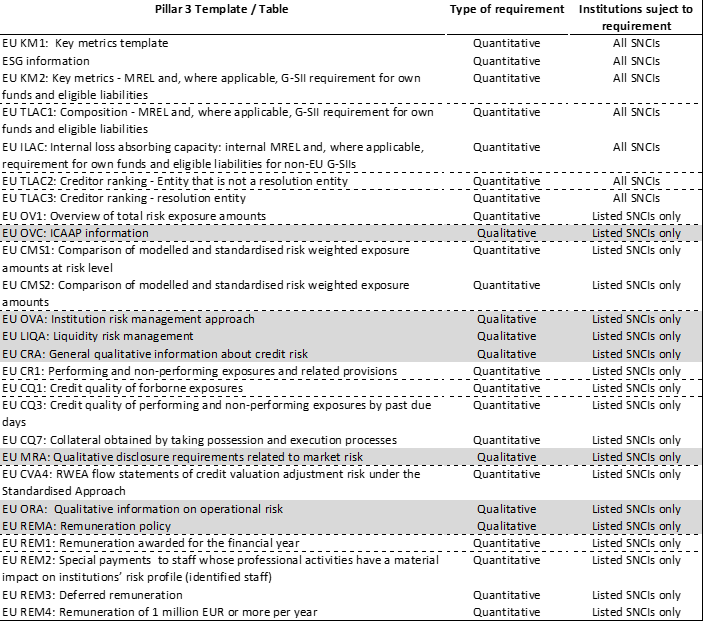

- SNCIs are subject to a reduced set of quantitative and qualitative disclosure requirements, reflecting the proportionality already embedded in the CRR legal text. Below, an overview of all Pillar 3 requirements applicable to SNCIs is provided:

- A centralised process for the calculation and subsequent publication of Pillar 3 information through the EBA P3DH is designed to ease the operational burden currently borne by institutions in managing their own disclosure processes. Centralising these tasks limits the need for institutions to maintain their own disclosure channels. Moreover, providing a single access point where all relevant information is available represents a significant improvement in terms of transparency, comparability, and data accessibility for all P3DH users, including institutions and supervisors.

- The requirements applicable to SNCIs are set out in the CRR and in the corresponding comprehensive ITS on institutions’ public disclosures. These requirements are not currently under review, except for the topics covered in this consultation paper, as they are already considered proportionate to the size and complexity of these institutions. The implementation of the P3DH introduces a new way of disclosing, but it does not alter the scope or volume of information that must be made publicly available.

- While certain quantitative data enabling a centralised computation by the EBA are already collected through the supervisory reporting framework, it matters analysing whether these data are sufficient to produce all information required for disclosure. In the case of qualitative information, it is not currently gathered within the supervisory reporting framework. In this context, it is necessary to assess which options would most effectively reduce the cost and operational burden for smaller institutions.

- Collecting the relevant information through the supervisory reporting framework, to be processed and published centrally by the EBA, would directly reduce the volume of data that institutions would otherwise need to compile and disclose on their own websites or through equivalent channels. Consolidating all required information within a single, centralised disclosure process would provide a simpler and more transparent approach for all parties involved, without creating additional burden for institutions, as the information would in any case need to be prepared by institutions for disclosure.

- The assessment presented in the following sub‑sections is guided by the principle that any additional supervisory data requirements should be strictly limited to what is necessary, both in terms of the relevance of the information and the EBA’s ability to perform a centralised computation replacing institutions’ current disclosure processes. This approach is intended not only to ensure proportionality but also to maximise the efficiency gains for institutions, notably by reducing duplication of work and limiting the operational burden associated with preparing and publishing Pillar 3 information across multiple channels.

1.3.1 Assessment of SNCIs’ Pillar 3 requirements

- Most of the Pillar 3 requirements under the list previously presented is applicable to listed SNCIs only. However, some of these requirements are applicable to non-listed SNCIs as well. In this sub-section, a detailed assessment of the requirements applicable to non-listed SNCIs and quantitative / qualitative requirements applicable to listed SNCIs is provided.

Requirements applicable to non-listed SNCIs

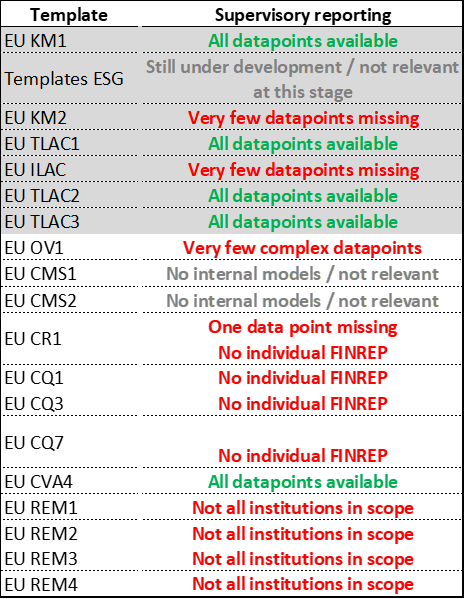

- As presented in the Figure above, only quantitative requirements are applicable to all SNCIs being these the solely requirements applicable to non-listed institutions. In this sense, after analysing the mapping tool for the templates at stake, the following is observed:

- ESG requirements are still under finalisation and for this reason are not yet considered in this analysis.

As regards requirements on MREL / TLAC (EU KM2, EU TLAC1, EU ILAC, EU TLAC2 and EU TLAC3), an overview of the institutions required to disclose each template is provided below. This list was prepared based on the disclosures signposting tool, excluding the requirement that would arise from BRRD only. In fact, the EBA mandate does not cover BRRD requirements. As such, in the context of the P3DH implementation, only the requirements arising from CRR would be relevant. While these requirements are presented in the previous table as applicable to all SNCIs, in practice, no SNCI seems to fall in the “level of application” presented in the following table to be mandatorily required to disclose this information under CRR. A question on this matter is included in this consultation.

Figure 3: Potential application of MREL/TLAC requirements to SNCIs - At this stage with the available information, no amendment is proposed to the supervisory reporting framework as regards the requirements that are applicable to non-listed SNCIs. All the information needed to compute the Pillar 3 figures under EU KM1 is available to the EBA.

- To allow non-listed SNCIs to provide accompanying narrative for EU KM1, if needed, this is proposed to be added to the EBA Data Point Model (DPM).

Quantitative requirements applicable to listed SNCIs

- Listed SNCIs currently account for approximately 4%[8] of the overall SNCI population. Nevertheless, under the CRR3 mandate, it remains essential to assess all applicable requirements and to determine whether the EBA can fulfil its mandate—namely, whether the necessary information is already captured through the supervisory reporting framework. It is therefore crucial that the potential proposals outlined below are considered in their proper context: any adjustments for listed SNCIs would affect only a very limited number of institutions and would, at the same time, enable these entities to have all Pillar 3 information disclosed in a single location.

- Similarly to the requirements applicable to non-listed SNCIs, an analysis of the mapping tool was performed as regards the quantitative requirements that are applicable to listed SNCIs only. The results are summarised below:

- Templates greyed out in the Figure above were already analysed for non-listed SNCIs. The conclusion of this analysis remains valid to listed SNCIs.

- Templates EU CMS1 and EU CMS2 relate to comparison of modelled and standardised risk weighted exposure amounts. By definition, SNCIs do not apply internal models. Under Article 4, paragraph 1, point (145) (g) of the CRR, a SNCI corresponds to an institution that does not use internal models to meet the prudential requirements in accordance with this Regulation except for subsidiaries using internal models developed at the group level, provided that the group is subject to the disclosure requirements laid down in Article 433a or 433c on a consolidated basis.

- SNCIs are subject to Pillar 3 requirements at the highest level of consolidation, as per Article 13 of the CRR. As such, no SNCI under the scope of P3DH will be making use of internal models reason why this requirement is, in practice, not applicable to these institutions and can be disregarded in the context of this analysis.

- For EU CVA4 all datapoints are available under the supervisory reporting framework. For this reason, no action is needed.

- As regards all the other Pillar 3 templates presented in the figure above, a detailed analysis and proposed way forward is presented under section 3.3.2 of this consultation paper.

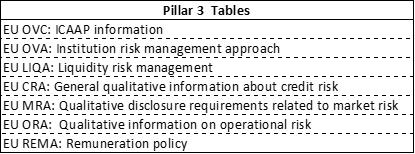

Qualitative requirements applicable to listed SNCIs

- As previously mentioned, listed SNCIs are subject to a few qualitative requirements. Below, the list of required tables to be disclosed is presented:

- Currently, under the reporting framework, no qualitative information is collected. As such, as regards SNCIs process for qualitative information, there are three possible options:

- Option A: Take no action - SNCIs would need to continue disclosing this information as done under CRR2 (i.e. on their website or, in the absence of a website, in any other appropriate location);

- Option B: Submission of a report in PDF format - SNCIs would prepare a report containing all the qualitative tables + accompanying narratives and submit to the EBA under the supervisory reporting framework;

- Option C: Use the DPM - The EBA would model the tables and the templates to allow the submission of (i) the qualitative information required under each table and (ii) the accompanying narrative needed to be disclosed together with the quantitative data. To note that the DPM has limitations for the inclusion and transmission of qualitative information, compared to traditional work processors, and the information reported using this option might be much limited compared to the use of PDFs.

1.3.2 Detailed amendments’ proposals to reporting framework templates

Template EU OV1 – Overview of total risk exposure amount

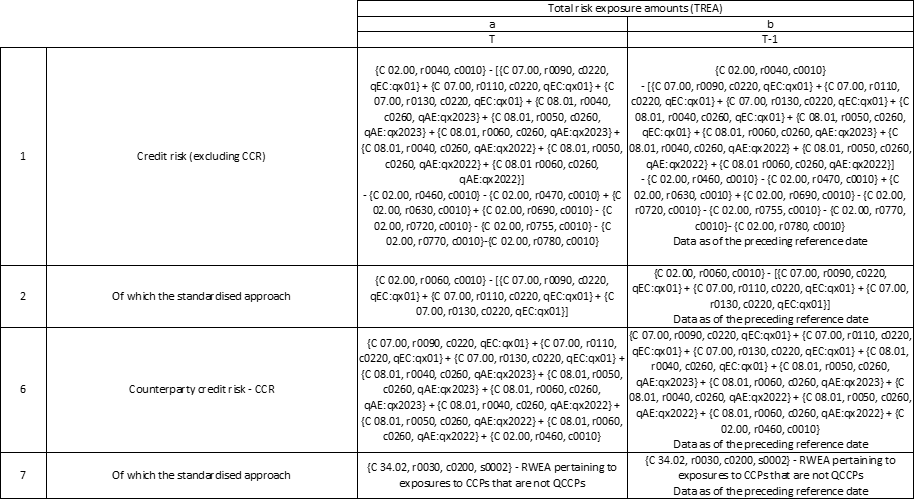

- Regarding EU OV1, the relevant datapoints for SNCIs are mapped to the supervisory reporting templates, a few of them may involve complex calculations and therefore present a higher risk of errors. It is therefore recommended that these datapoints are collected separately. In total, this would concern 4 datapoints for two reference dates as outlined below:

- As previously mentioned, SNCIs do not make use of internal models. As such, it would suffice to add rows 2 and 6 in the supervisory reporting template. In order to minimize as much as possible the number of added datapoints, only period T would be considered. In practice, this means that for the first year of centralised disclosure the comparative for “T-1” would not be available. The datapoints are proposed to be added to COREP in “C 04.00 – Memorandum items”. It was also considered to add these datapoints in C 02.00 but the figures for credit risk in this template are presented including CCR while under the P3 templates it is required to be disclosed separately. It would look as follows:

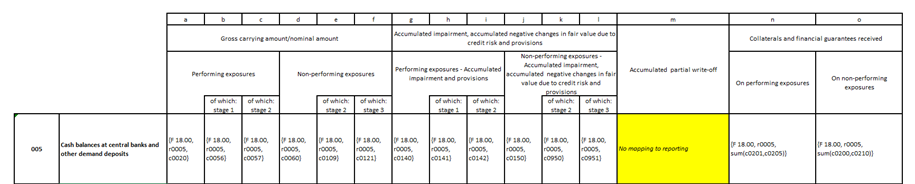

Template EU CR1 - Performing and non-performing exposures and related provisions / Template EU CQ1 - Credit quality of forborne exposures / Template EU CQ3 - Credit quality of performing and non-performing exposures by past due days / Template EU CQ7 - Collateral obtained by taking possession and execution processes

- As regards EU CR1, only one datapoint is not mapped to FINREP (please see below):

- This datapoint is proposed to be disregarded as any type of write-off on “cash balances at central banks and other demand deposits” that could be considered by institutions in this disclosure template is not deemed as significant information.

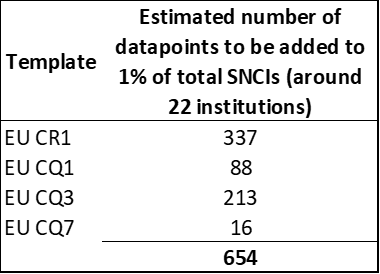

- Information on credit quality and non-performing loans is now collected in the supervisory reporting ITS as part of the FINREP module. The FINREP module is not reported on an individual basis. A small part of the listed SNCIs are solo entities (corresponding to 1% of the total number of SNCIs). As such, for these SNCIs, EU CR1 would need to be collected. The same is valid to EU CQ1, EU CQ3 and EU CQ7. These 4 disclosures templates are proposed to be added in the supervisory reporting framework under a separate module dedicated to SNCIs’ information on non-performing loans. These templates would be applicable only to the listed SNCIs on a solo basis (around 22 institutions).

Templates on Remuneration policies

- Listed SNCIs are also required to disclose information on remuneration policies. Less than half of the existing listed SNCIs are currently reporting this information under the EBA Guidelines on remuneration. As such, similarly to what was presented in the previous sub-section, also for remuneration disclosure templates the proposal would be to include them in the separate supervisory reporting module dedicated to SNCIs’ disclosures. This would guarantee that information is available to all listed SNCIs. Being this venue pursued, no duplication would occur as these institutions would not need to provide the same information under the EBA Guidelines on remuneration.

Overview datapoints

- Following the proposals presented in this consultation paper as regards the disclosure requirements for SNCIs, an overview of the datapoints that could possibly be added to the supervisory reporting is provided below. As previously mentioned, the increase in datapoints that SNCIs would provide under the supervisory reporting framework is offset by the reduction in datapoints they would otherwise need to disclose, as the EBA would publish this information on their behalf:

2 Accompanying documents

2.1 Draft cost-benefit analysis / impact assessment

As per Article 15 of Regulation (EU) No 1093/2010 (EBA Regulation), any draft implementing technical standards (ITS) developed by the EBA shall be accompanied by an Impact Assessment (IA), which analyses ‘the potential related costs and benefits’.

This analysis presents the IA of the main policy options included in this Consultation Paper on the draft ITS amending Commission Implementing Regulation (EU) 2024/3117 on supervisory reporting referred to in Article 430 (7) of Regulation (EU) No 575/2013 concerning SNCIs Pillar 3 Data Hub (‘the draft ITS’). The analysis provides an overview of the identified problem, the proposed options to address this problem as well as the potential impact of these options. The IA is high level and qualitative in nature.

A. Problem identification and background

The banking regulation has been amended in the context of the Capital Requirements Directive (CRD IV) and Capital Requirements Regulation (CRR 3) package. The CRR 3 introduces important changes related to the disclosure of institutions’ Pillar 3 information. Article 434a, first paragraph of Regulation (EU) No 575/2013 (‘the CRR’) mandates the EBA to develop IT solutions for disclosures required under Titles II and III of the same regulation. Article 434 of the CRR requires the EBA to publish in its website the Pillar 3 information to be disclosed by institutions ('Pillar 3 Data Hub' or 'P3DH').

The process to be followed by large and other institutions was already treated in the 2025 Final Draft Implementing Technical Standards on IT solutions for public disclosures by institutions, other than small and non-complex institutions, of the information referred to in Titles II and III of Part Eight of Regulation (EU) No 575/2013 (‘EBA/ITS/2025/01’). As regards SNCIs, given the specificities of the process envisaged in the level 1 text and the need to find a proportionate solution for these institutions, it was decided to consult separately. For SNCIs, the approach will differ from the process applied to large and other institutions (which must submit their already processed Pillar 3 disclosure reports, which the EBA then publishes without further transformation) as the EBA will use SNCIs supervisory reporting data to produce the quantitative Pillar 3 disclosures for SNCIs. For this approach, the EBA will need some additional data to be reported by SNCIs in their supervisory reporting. Hence, this consultation paper presents the draft ITS amending Commission Implementing Regulation (EU) 2024/3117 on supervisory reporting referred to in Article 430 (7) of Regulation (EU) No 575/2013 concerning SNCIs P3DH.

B. Policy objectives

The draft ITS amending Commission Implementing Regulation (EU) 2024/3117 on supervisory reporting referred to in Article 430 (7) of Regulation (EU) No 575/2013 concerning SNCIs Pillar 3 Data Hub aims at allowing EBA to produce the Pillar 3 disclosures for SNCIs, requiring the additional necessary data to be reported by SNCIs in their supervisory reporting. This will allo in turn SNCIs tos opt dislcosing this infomraiton themselves, as the EBA will dislcose it based on the data received through supervisory reporting.

C. Options considered, assessment of the options and preferred options

Section C. presents the main policy options discussed, and the decisions made by the EBA during the development of the Draft ITS. Advantages and disadvantages, as well as potential costs and benefits from the qualitative perspective of the policy options and the preferred options resulting from this analysis, are provided.

Template EU OV1 – Overview of total risk exposure amount

To fully meet the EBA mandate regarding the EU OV1 template for listed SNCIs, only four datapoints covering two reference dates (in total 8 datapoints) are currently missing from the supervisory reporting framework. To address this gap with the least possible burden on institutions, the EBA proposes incorporating these datapoints into COREP, accompanied by two key simplifications: (i) institutions would report the required data only for the current reference date (meaning that no comparative figures would be available for the first disclosure, but these would naturally become available in subsequent cycles); and (ii) only two datapoints would be collected directly, as the remaining two can be reliably derived by the EBA. This means that only two additional datapoints are proposed to be added.

Option 1a: Collect the missing datapoints, minimizing the burden to the maximum, so the EBA mandate as regards EU OV1 can be fully met

Option 1b: Do not collect the missing datapoints, being institutions required to disclose this information on their website or via similar means

Including two additional datapoints in COREP is not considered an undue burden, particularly when weighed against the benefits. This approach avoids the disproportionate costs institutions would otherwise incur to disclose such a small amount of information separately, while also ensuring that all relevant data are available in a single, centralised location.

Based on the above, the Option 1a has been chosen as the preferred option and the draft ITS will request the collection of the missing datapoints, minimizing the burden to the maximum, so the EBA mandate as regards EU OV1 can be fully met.

Template EU CR1 - Performing and non-performing exposures and related provisions

To fully meet the EBA mandate regarding the EU CR1 template for listed SNCIs, only one data point is missing from the supervisory reporting framework.

Option 2a: Add the datapoint to the supervisory reporting framework as this information is required under the Pillar 3 template

Option 2b: Do not add the datapoint as this is not deemed information significant enough to increase the reporting requirements

Following EBA’s analysis performed, this datapoint is not deemed to provide very relevant information (also based on the materiality principle that is applicable to the Pillar 3 framework under CRR).

Based on the above, the Option 2b has been chosen as the preferred option.

Template EU CR1 - Performing and non-performing exposures and related provisions / Template EU CQ1 - Credit quality of forborne exposures / Template EU CQ3 - Credit quality of performing and non-performing exposures by past due days / Template EU CQ7 - Collateral obtained by taking possession and execution processes

To fully meet the EBA mandate regarding templates EU CR1, EU CQ1, EU CQ3 and EU CQ7 for listed SNCIs on a solo basis, these templates on credit quality would need to be added to the supervisory reporting framework under FINREP module.

Option 3a: Add the abovementioned templates to the supervisory reporting framework

Option 3b: Do not add the abovementioned templates to the supervisory reporting framework

Including these templates in the supervisory reporting framework is not considered an undue burden, particularly when weighed against the associated benefits and given that the requirement would currently apply to only a small portion of the SNCI population. This approach avoids the disproportionate costs that institutions would otherwise incur to disclose this information separately, while ensuring that all relevant data are captured in a single, centralised location.

Based on the above, the Option 3a has been chosen as the preferred option.

Templates on Remuneration policies

To fully meet the EBA mandate regarding information on remuneration policies for listed SNCIs, the respective templates would need to be added to the supervisory reporting framework. If this option is pursued, the respective information would not be requested under the Guidelines on remuneration.

Option 4a: Add the remuneration policies templates to the supervisory reporting framework

Option 4b: Do not add the remuneration policies templates to the supervisory reporting framework

Including these templates in the supervisory reporting framework is not considered an undue burden, particularly when weighed against the associated benefits and given that the requirement would currently apply to a small portion of the SNCI population. This approach avoids the disproportionate costs that institutions would otherwise incur to disclose this information separately, while ensuring that all relevant data are captured in a single, centralised location.

Based on the above, the Option 4a has been chosen as the preferred option.

D. Conclusion

Overall, the impact assessment on the Draft ITS suggests that the expected benefits are higher than the incurred expected costs. The draft ITS amending Commission Implementing Regulation (EU) 2024/3117 on supervisory reporting referred to in Article 430 (7) of Regulation (EU) No 575/2013 concerning SNCIs Pillar 3 Data Hub will, by requiring the additional necessary data to be reported by SNCIs in their supervisory reporting, allow EBA to produce the Pillar 3 disclosures on behalf of the SNCIs. For the institutions, the implementation of these draft ITS is not expected to trigger significant costs and these costs are balanced by the benefit of EBA itself producing the Pillar 3 disclosures. Furthermore, the majority of the costs are linked to the CRR3 changes and thus the costs are not all to be associated with the draft ITS but with the underlying related changes brought by the CRR3. Overall, the impact assessment on the draft ITS suggests that the expected benefits are higher than the incurred expected costs.

2.2 Overview of questions for consultation

2.2.1 Assessment of SNCIs’ Pillar 3 requirements

Question 1: Do you agree with our assessment regarding MREL/TLAC disclosures?

Question 2: Would you agree that no datapoints need to be added to the reporting framework as regards the Pillar 3 requirements applicable to non-listed SNCIs?

Question 3: Would you agree with the assessment performed as regards EU CMS1 and EU CMS2 and that no action is needed?

Question 4: Would you agree to add in DPM the accompanying narrative for EU KM1 (applicable to listed and non-listed SNCIs)?

Question 5: As regards the options presented for the disclosure of qualitative information (Options A, B, C), which one would you prefer? Please explain the reasoning followed.

2.2.1 Detailed amendments’ proposals to reporting framework templates

Question 6: Would you agree with the general approach to add datapoints to the supervisory reporting framework, so the EBA is under conditions to compute the respective Pillar 3 figures? Please explain your reasoning.

Question 7: In case you are an institution and the answer to the previous question is no, how do you plan to disclose this information? How would you see the split in the disclosure process in terms of burden, usefulness and good understanding of the disclosed Pillar 3 data? Please see also question 5 on the disclosure of qualitative information.

Question 8: Would you agree with the rationale followed and proposed solution to EU OV1 datapoints? Would you agree that these datapoints would be useful not only to listed SNCIs but all institutions reporting and disclosing this information?

Question 9: Would you agree with the assessment performed for the missing data point in the EU CR1 template, i.e., to disregard this information?

Question 10: Would you agree with the proposal to collect EU CR1, EU CQ1, EU CQ3 and EU CQ7 for listed SNCIs at solo level, that would allow that listed SNCIs do not have to keep disclosing this information separately?

Question 11: Would you agree with the proposal to include the remuneration templates in the supervisory reporting framework for listed SNCIs, that would allow that listed SNCIs do not have to keep disclosing this information separately?

Consultation paper and Annexes |

[4] Regulation (EU) 2024/1623 of the European Parliament and of the Council of 31 May 2024 amending Regulation (EU) No 575/2013 as regards requirements for credit risk, credit valuation adjustment risk, operational risk, market risk and the output floorText with EEA relevance.

[8] Around 90 institutions.