Consultation Paper on Revisions to the ITS on supervisory reporting (Commission Implementing Regulation (EU) 2024/3117) - Module on ESG Reporting

The content on these interactive pages is provided for ease of reference and to assist in the reading and understanding of the Consultation Paper and it is not considered as the official version of such documents.

For the formal consultation papers and their components, please refer to the .pdf documents provided at the bottom of this page. In case of discrepancies between these interactive pages and the .pdf documents, the latter prevail as the authentic official versions.

Responding to this consultationPlease provide your responses by 10 July 2026 at 23:59 CEST via EU survey (Password for the survey: Reporting2026). Late responses will not be considered. |

Background and rationale

- The integration of ESG risks into prudential supervision constitutes a key regulatory priority within the Union’s sustainable finance strategy. CRR3 introduces new reporting and extends the scope of the disclosure requirements to ensure that competent authorities are equipped with harmonised data to assess institutions’ exposures to environmental and climate-related risks and their risk mitigation strategies.

- The mandate for the EBA to develop ESG-related supervisory reporting requirements derives from Article 430(7) of the CRR, which requires the EBA to develop draft Implementing Technical Standards (ITS) specifying uniform reporting formats, frequencies and instructions necessary for competent authorities to monitor compliance with prudential obligations.

- In preparing the reporting requirements set out in this consultation paper, the EBA has taken into account the relationship with the disclosure framework established under Article 449a of CRR3. Article 449a(3) specifies that disclosures shall not require institutions to provide information beyond that requested under supervisory reporting pursuant to Article 430(1), point (h), of CRR3. The reporting proposal on ESG has been designed taking into account the Pillar 3 disclosure requirements as a basis for the development of the reporting on ESG.

- Following the integration of ESG risks into the prudential framework through CRR3, ESG risk management forms part of institutions’ regulatory obligations. Consequently, insofar as ESG risks are embedded within prudential requirements, the EBA is required to specify corresponding supervisory reporting to enable effective monitoring and consistent supervisory assessment across Member States.

- This consultation paper builds on the EBA’s broader ESG roadmap, including its supervisory guidelines on the management of ESG risks and its previous work on Pillar 3 ESG disclosures. In developing the draft ITS on supervisory reporting on ESG risks, the EBA has taken into account the work undertaken in the context of the ITS on Pillar 3 ESG disclosures, including the analysis and feedback gathered through the related consultation paper. This parallel process ensures a high degree of consistency and full alignment between reporting and disclosure requirements in terms of definitions, methodologies and templates.

1 Simplification objectives

- The proposals have been developed taking into account the EBA’s strategic objective to simplify and enhance the proportionality of the EU supervisory reporting framework, in line with the EBA simplification objectives to rationalise reporting requirements and reduce unnecessary complexity. Particular attention has been paid to streamlining templates, consolidating data points, removing duplicative or low-use information and embedding proportionality mechanisms, including simplified requirements for smaller and less complex institutions, other institutions and large subsidiaries.

- The proposals included in this consultation paper have considered the broader EU objective of regulatory simplification and coherence, including the European Commission’s “Omnibus” initiatives aimed at improving consistency, proportionality and usability across sustainability-related regulations and directives. In this context, due regard has been given to the interaction with the Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS), with a view to promoting alignment, reducing overlaps and facilitating operational implementation for institutions subject to multiple sustainability reporting frameworks.

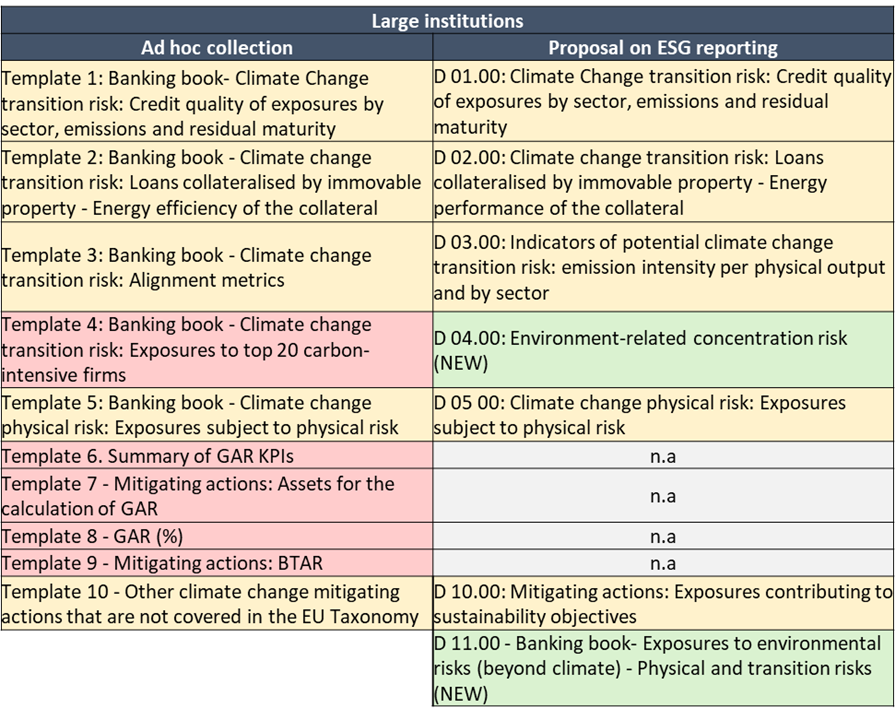

- In addition, prior to the development of the reporting framework proposed in this consultation paper, institutions have already been reporting ESG information through an ad- hoc data collection established by EBA Decision EBA/DC/498 of 6 July 2023. Under that decision, only large institutions that have issued securities admitted to trading on a regulated market of a Member State were required to report this information, using the templates developed for Pillar 3 ESG disclosures. This ad-hoc collection is intended to remain in place until the supervisory reporting framework proposed in this consultation paper becomes applicable.

- The experience gained through that data collection has informed the design of the proposed reporting framework. While the CRR3 introduces new requirements that extend the scope of ESG supervisory reporting to all institutions, the framework proposed in this consultation incorporates proportionality measures so that the reporting burden remains proportionate with institutions’ size and complexity. At the same time, compared with the ad-hoc collection, the reporting requirements for large institutions have been simplified. In particular, several templates previously included in the ad-hoc exercise have been streamlined and others have been removed, notably templates 6 to 9 related to information under the Taxonomy Regulation, including the Banking Taxonomy Alignment Ratio (BTAR), as well as template 4 on the exposures to top 20 carbon-intensive firms.

- The table below provides an overview of the main changes between the ad-hoc collection and the proposal for large institutions:

- Finally, the aim with this technical standard is to ensure maximum harmonisation of the supervisory reporting framework on ESG risks at EU level and allow competent authorities (CAs) to drop their parallel data collections on the topic.

2 Proportionality and scope of institutions

- Article 430(1)(h) of CRR3 mandates institutions to report to competent authorities’ information necessary for the monitoring of ESG risks. The supervisory reporting mandate extends to all institutions within the scope of the CRR framework, as required under Article 430 CRR. This includes large institutions, large subsidiaries, other institutions and small and non-complex institutions (SNCIs).

- While the scope of supervisory reporting is broad, CRR3 requires that ESG reporting is specified in a proportionate manner, taking into account the size, complexity and risk profile of institutions, as well as their relative exposure to ESG risks. In developing the proposed draft ITS on supervisory reporting on ESG risks, the EBA has followed, to the extent appropriate, the same approach to proportionality and differentiation of scope as applied under the ITS on Pillar 3 ESG disclosures, while adapting it to the specific objectives of supervisory monitoring.

- In preparing this proposal, the EBA has considered four main aspects to guide the proportionality approach:

- Providing supervisors with sufficient granular and comparable data: templates are designed to give competent authorities detailed and harmonised information on ESG exposures and risk mitigation strategies to support risk-based supervision.

- Strengthening alignment between supervisory reporting and Pillar 3 disclosures: the definitions, instructions and many data points are largely aligned with the Pillar 3 ESG disclosure framework to ensure consistency and reduce operational burden, while divergencies are explicitly justified by supervisory requirements. In this vein, the reporting requirements are following the same level of consolidation (highest level of consolidation in the EU for all institutions and for large subsidiaries on individual basis or, where applicable, on a sub-consolidated basis) as the Pillar 3 disclosures for consistency and for allow institutions to map the information with disclosures.

- Adjust reporting through differentiated templates and materiality thresholds: reporting requirements are differentiated according to the size, complexity, and risk profile of institutions, with smaller or less complex institutions subject to simplified and reduced templates. Materiality thresholds are applied in certain templates to focus on significant exposures, avoid unnecessary reporting, and ensure that the increased data requested does not impose disproportionate burden.

- Supporting simplification and efficiency: the proposal streamlines data collection, removes duplicative information, and focus on the essential data necessary for supervisory purposes. As a new reporting framework under CRR3, ESG reporting contributed to the EBA’s 2025 simplification efforts, supporting enhanced proportionality and avoiding overlaps between EBA and national reporting. Some of the information in the ESG templates serves multiple purposes, such as simplifying certain FINREP data points and meeting supervisory stress-testing data needs.

- Based on the above considerations, the EBA is putting forward a proportionate approach, consistent with the Pillar 3 framework, defining three sets of templates:

- A comprehensive set of templates (7 templates), to be reported by large listed and non-listed institutions. This set is largely aligned with the templates applicable under the Pillar 3 ESG disclosure framework and includes two additional supervisory-specific templates: Template D 04.00 on concentration risk and Template D 11.00 on exposures to environmental risks beyond climate.

- A simplified set of templates (6 templates), to be reported by Other listed institutions and large subsidiaries. This proposal includes a streamlined version of the physical risk template with similar content as in the Pillar 3 ITS.

- A reduced and essential set of information (1 template), that shall be reported by listed and non-listed SNCIs and by other non-listed institutions. This template provides a streamlined and aggregated view of both transition and physical risks, consolidating the key supervisory data into a single reporting format.

- The full sets of templates to be reported by each type of institution is provided in the table below:

Table 2: Proportionate approach for ESG reporting

Supervisory reporting |

| ||||

Full approach | Simplified approach |

| |||

Template | Large institutions | Other listed institutions + Large subsidiaries | SNCI + Other non-listed institutions | Materiality thresholds | |

| D 01.00: Climate Change transition risk: Credit quality of exposures by sector, emissions and residual maturity | Semi-annual (for large institutions with total assets >= 30 bn EUR) | - | - | Country breakdown applying FINREP materiality thresholds + thresholds at sectoral level | |

| D 01.02: Climate Change transition risk: Credit quality of exposures by sector, emissions and residual maturity (subset of D 01.00) | Semi-annual (for large institutions with total assets < 30 bn EUR) | Annual |

|

| |

| D 01.01 Template 1A: Transition and physical risk | - | - | Annual |

| |

| D 02.00: Climate change transition risk: Loans collateralised by immovable property - Energy performance of the collateral | Semi-annual | Annual | - |

| |

| D 03.00: Indicators of potential climate change transition risk: emission intensity per physical output and by sector | Annual | - | - |

| |

| D 04.00: Environment-related concentration risk (NEW) | Semi-annual | Annual | - | Report counterparties for which the total exposure level exceeds EUR 10 million. | |

| D 05 00: Climate change physical risk: Exposures subject to physical risk | Semi-annual | Country breakdown applying FINREP materiality thresholds | |||

| D 05.01: Climate change physical risk: Exposures subject to physical risk | Annual | ||||

| D 10.00: Mitigating actions: Exposures contributing to sustainability objectives | Annual | Annual | - |

| |

| D 11.00: Banking book- Exposures to environmental risks (beyond climate) - Physical and transition risks (NEW) | Annual | Annual |

| Country breakdown applying FINREP materiality thresholds | |

Materiality

- Following the objectives of simplification and proportionality, materiality thresholds are proposed for those templates where a geographical breakdown is requested (D01.00, D05.00 and D11.00). In those cases, the EBA proposes to follow similar materiality thresholds as those proposed in this consultation for the Finrep and stress test reporting geographical breakdowns:

- Institutions shall report the geographical breakdown in the z-axis of the template (country breakdown (when their non-domestic exposures represent more than 10% of their total exposures.

- Furthermore, institutions shall report only those countries that represent more than 1% of the total exposures, in order to avoid reporting of less material countries (exposures in these less material countries would be aggregated into an “other countries” residual category). Reporting institutions below the abovementioned 10% non-domestic exposure threshold would be requested to report a simplified geographical breakdown with only the totals and the split between domestic and non-domestic exposures. The materiality threshold allows to include further proportionality in the reporting of the templates which have a geographical breakdown.

- For further information on the materiality thresholds applicable to D 01.00, please refer to the module on Integration of EU-wide stress testing.

3 Overview and rationale of reporting templates

- The ESG supervisory reporting templates are based on the Pillar 3 ESG disclosure framework. Building on this foundation, the following section sets out the rationale for each template and the additional data introduced to develop supervisory reporting requirements. The supplementary data ensures that competent authorities have sufficiently detailed and comparable information to assess institutions’ exposures to ESG risks, including transition and physical risks.

a) D 01.00 – Climate Change Transition Risk: Credit quality of exposures by sector, emissions and residual maturity

- This template shall be reported by large institutions with total assets above 30bn EUR (at the highest level of consolidation in the EU at consolidated and individual level).

- Template D01.00 is designed to address multiple data needs. It supports the supervisory monitoring of exposures to climate change transition risks by identifying those exposures towards corporates in sectors that can highly impact climate change, and by providing information on GHG emissions, maturity and credit quality that may support supervisors in their risk assessment. At the same time, provides data required for the EU-wide stress test exercises, including both credit risk and climate-related stress tests.

- The structure of the template is closely aligned with the corresponding Pillar 3 disclosure template and covers exposures in the banking book, including loans, debt securities and equity instruments at amortised costs and those measured at fair value through other comprehensive income (FVOCI). Building on that framework, additional data points have been introduced for supervisory reporting purposes to enable more granular risk analysis and to meet specific stress test data requirements. Certain data points have also been incorporated with a view to further simplifying and streamlining FINREP reporting, by reducing overlaps and improving consistency across supervisory data collections.

- For supervisory reporting purposes, the template has been further expanded to enhance its suitability for supervisory risk assessment and monitoring. In particular, it now incorporates information on gross interest income and gross fee and commission income, allowing supervisors to better assess the relevance of ESG risk exposures in terms of income generation. Information on ‘off-balance sheet exposures’ has also been added to allow for comprehensive assessment of all possible risk exposures.

- In addition, the sectoral breakdown in the rows has been extended with more granular NACE codes to ensure that information on exposures towards fossil fuel sectors can be identified, as requested by the level 1 text, and to facilitate the risk analysis, as the fossil fuel sectors are the ones most exposed to climate change transition risk. Information on household exposures has also been added, to facilitate the climate stress test. Furthermore, information on the coverage of portfolios using proxies (in accordance with the PCAF methodology), expressed as a percentage, for Scope 3 financed emissions, has been added, allowing supervisors to assess the extent to which emissions data rely on proxy methodologies. The template also includes more granular information on credit quality and classification of exposures and impairments, to allow identification not only of information on non-performing loans but also on stage 3 exposures, allowing for consistent reporting by institutions under both IFRS and nGAAP.

- Finally, the template includes information not only on NACE sectors but also on country breakdown, the latter for the amortised cost portfolios. The information on country breakdown is important for supervisors to assess and stress climate change transition risk, as this risk may be very much impacted by policy decisions and regulations of the country where the exposures are located. For this purpose, institutions would be requested to report a “z-axes”, in older to provide information on loans and advances and debt securities at amortised cost, which, provide breakdowns by country, for those countries that need to be reported according to materiality thresholds defined, and aggregate for the rest of amortised costs exposures. Materiality thresholds will apply to certain reported information, consistent with the approach used in the EU-wide stress test.

- For further details on the data requirements specifically related to the stress test components and the materiality thresholds applicable, please refer to the module on integration of EU-wide stress testing.

Other possible information for which the EBA is seeking feedback

- In the context of assessing potential systemic risks, including those stemming from climate-related exposures, information on risk-weighted exposure amounts (RWEA) could play a role in link ESG-related data to prudential metrics used for supervisory purposes. In particular, information on RWEA could enhance the ability to assess the prudential materiality of environmental risks and to inform the potential calibration of macroprudential tools, such as the Systemic Risk Buffer (SyRB). Without such information, it may be challenging to evaluate consistently the extent to which climate-related exposures translate into capital requirements and contribute to system-wide vulnerabilities.

- However, the ESG reporting templates under this ITS are primarily designed on accounting premises and structured around financial reporting concepts. The inclusion of prudential metrics such as RWEA would therefore raise important operational and methodological challenges for institutions, including the need to reconcile accounting and regulatory reporting frameworks, adapt internal data systems, and potentially duplicate reporting processes. This could result in additional complexity and reporting burden.

- In light of this trade-off between prudential usefulness and operational feasibility, the EBA is seeking stakeholders’ views on the relevance, proportionality and practical implications of incorporating RWEA information into the ESG templates, as well as possible alternative approaches that would achieve similar prudential objectives while limiting operational constraints.

b) D 01.02 – Climate Change Transition Risk: Credit quality of exposures by sector, emissions and residual maturity

- This template is a subset of template D 01.00, which will apply to other listed institutions, large subsidiaries and to large institutions with less than 30bn EUR total assets.

c) D 01.01 – Simplified ESG information (for SNCIs and other non-listed institutions).

- This template is largely based on the corresponding Pillar 3 template. Some additional data points have been introduced for supervisory reporting purposes.

- The simplified template should capture information on climate change transition and physical risk for SNCIs and other non-listed institutions. It shall be reported on an annual basis.

- The template provides an overview of exposures subject to physical risk with a reduced scope of geographies, ensuring proportionality while preserving supervisory usefulness.

- For supervisory reporting purposes, additional columns have been included:

- Off balance sheet items, to provide a more comprehensive view of institutions’ exposures, consistent with the supervisory objective of capturing risks beyond the balance sheet.

- “Accumulated impairment accumulated negative changes in fair value due to credit risk”, added to support a simplified yet complete reporting framework and to facilitate the planned simplification of some Finrep templates (F 06.01 and F 20.07.1). Please refer to the module on Finrep for further details.

- In the rows, further NACE sector breakdown has been incorporated with a view to further simplifying and streamlining FINREP reporting, by reducing overlaps and improving consistency across supervisory data collections.

- The template consolidates all relevant information into a single template, simplifying information on maturity buckets, and removing information on GHG financed emissions.

d) D 02.00 – Climate Change Transition Risk: Loans collateralised by immovable property

- This template provides information on the distribution of real estate loans and advances and repossessed collateral, classified by primary energy use and EPC label of the collateral. IT should help supervisors understand how the value of the real estate assets backing these loans may be impacted by climate change transition risk drivers depending on the energy efficiency of the collateral. The template is largely unchanged from the Pillar 3 template, with only a few additional elements added:

- Column on ‘Of which loans with an improvement of the energy efficiency of the collateral compared with the previous periods’, this column aims to allow the assessment of the efficiency of banks’ strategies for reducing transition risk in their mortgage portfolios.

- Covered bonds: following recital 55 of CRR3, the EBA previously consulted on including ESG risks of covered bond cover pools in Pillar 3 disclosures. Feedback suggested this information should not be included in disclosures but could be added for supervisory reporting. Accordingly, template D 02.00 now includes a row “of which: part of a cover pool of covered bonds” for total EU and non-EU exposures, and feedback is sought on its relevance for supervisory reporting purposes. It should help to have a better understanding of the part of the portfolio that is already encumbered and the part and efficiency of the rest

- Specific rows have been added to reflect LTV buckets, in order to allow more accurate analysis of vulnerability of specific exposures to transition risk related to the underlying collateral.

- A new column has been added to capture estimated EPC information under “Of which: level of energy efficiency (EPC label of collateral) – estimated”. This allows the EPC section of the template to include both actual EPC data, where an EPC label exists, and estimated information for cases where an EPC label is not available.

e) D 03.00 – Indicators of potential transition risk: Emission Intensity by Sector

- This template is largely based on the corresponding Pillar 3 template. Only two additional columns have been introduced for supervisory reporting purposes in relation to internal short-term targets, enabling supervisors to better understand institutions’ internal strategies, planning horizons and risk management approaches.

- This template shall be reported by large institutions on annual basis.

f) D 04.00 – Obligor-level environment-related corporate exposures

- The EBA proposes to introduce a new template on environment-related corporate exposures at obligor level , which will replace existing template 4 on concentration of exposures towards top 20 polluting companies, reported both in Pillar 3 and in the ad hoc supervisory reporting The new template 4 will be only part of supervisory reporting, and not of Pillar 3, as it will include obligor level information. It leverages on the structure of the large exposures template to ensure consistency and facilitate supervisory analysis.

- The objective of this template is to enable supervisors to identify and monitor concentration risks arising from exposures to counterparties operating in selected sectors subject to environmental factors. It is proposed that the template be reported at obligor level by large institutions on a semi-annual basis, and by other listed institutions and large subsidiaries annually.

- The introduction of this new template is also aligned with the short‑term recommendation set out in the EBA’s 2023 Report on the role of environmental and social risks in the prudential framework (EBA/REP/2023/34), which calls for the development of exposure‑based metrics to quantify environment‑related concentration risks. The template provides the necessary data to design and implement such metrics and to support supervisors in peer benchmarking, identifying emerging concentration patterns, and assessing the risks faced by institutions consistently across the EU.

- The template requires single-name or obligor-level reporting of exposures to non-financial corporates active in predefined sectors (including aluminium, automotive, aviation, building, cement, chemicals, coal, maritime and transport, oil and gas, power, steel), based on NACE codes. These sectors are selected to capture transition risk and are aligned with other supervisory reporting templates on climate-related risks. The template and selected sectors align with the content and design of other templates in the package such as D 01.00 and D03.00. Feedback from the consultation on this point is sought.

- The template collects obligor-level risk parameters, including:

- Gross carrying amount (on- and off-balance sheet), including breakdowns for new exposures, Stage 2 exposures and non-performing exposures;

- Accumulated impairment and provisions;

- Probability of default (12-month and lifetime, where applicable);

- Exposures subject to physical risks;

- Nominal amounts of off-balance-sheet exposures.

- To support the assessment of mitigation capacity and transition preparedness, the template also includes information on:

- The existence of a counterparty transition plan;

- Alignment with sectoral decarbonisation pathways;

- Financed emissions and emissions intensity indicators.

By combining sector classification, credit risk parameters, transition and physical risk exposures and mitigation indicators, the template enables supervisors to:

1. Assess concentration risks in key environmentally sensitive sectors;

2. Evaluate the risk profile and resilience of significant corporate obligors;

- Monitor the interaction between environmental risk drivers and traditional prudential risk metrics.

- A materiality threshold applies to ensure proportionality, limiting reporting to exposures above a defined level. Institutions shall report counterparties for which the total exposure level exceeds EUR 10 million. An additional threshold should be defined to ensure that institutions are only asked to report material information on relevant counterparties. This threshold could be defined in terms of a limit on the number of counterparties to report (e.g. top 20 counterparties with exposures above 10MN EUR) or in terms of a threshold similar to the one that is being defined under the stress test module for reporting of sectors. Feedback from the consultation on this point is also sought.

g) D 05.00 – Climate-related physical risk: Exposures Subject to physical risk

- The purpose of this template is to capture detailed information on exposures subject to physical risks by sector, geography and hazard category. It remains closely aligned with the corresponding Pillar 3 disclosure template, with only limited additional elements introduced for supervisory reporting purposes. This template shall be reported by large institutions on a semi-annual basis.

- Similarly, as in the Pillar 3 template, the geographical breakdown has been set up at country level, and institutions shall report in addition to the total:

- Country by country information, to be reported considering the materiality thresholds for the geographical breakdown, and

- Other EU exposures

- The template has also been expanded to include off‑balance‑sheet exposures, to have a complete view of physical‑risk exposures. Hazard‑category reporting is retained as in Pillar 3 disclosures, to allow the assessment of exposures sensitive to temperature, wind, water and/or solid‑mass related hazards.

- Under the Pillar 3 framework, only the aggregate amount of exposures subject to material physical risk shall be disclosed. For supervisory reporting purposes, a more detailed breakdown is considered necessary to allow for enhanced analysis and risk assessment. Therefore, within the total exposures subject to material physical risk, two further columns “of which highly exposed” and “of which moderately exposed” are proposed. This split is intended to allow supervisory authorities to better assess the relative severity of physical-risk exposure within institutions’ portfolios. Please refer to the accompanying document section 3, where further information and illustrative examples are provided.

- To enable an initial assessment of the impact of physical‑risk sensitivity (i.e. combining exposure and vulnerability) of institutions’ counterparties, the template now includes common credit‑risk indicators, namely 12-month PD, lifetime PD, LGD and LTV, which will also help to monitor any potential deterioration in institutions’ credit risk due to climate events over time.

h) D 05.01 – Climate-related physical risk: Exposures subject to physical risk (simplified)

- This template is largely based on the corresponding Pillar 3 template. Only a limited number of additional data points have been introduced for supervisory reporting purposes, while the row structure remains aligned with the Pillar 3 framework.

- The simplified template is designed to provide a proportionate reporting framework for capturing physical risk information for Other listed institutions and large subsidiaries. It shall be reported on an annual basis.

- The template provides an overview of exposures subject to physical risk with a reduced number of data points, ensuring proportionality while preserving supervisory usefulness.

- For supervisory reporting purposes, ‘Off-balance-sheet items subject to physical risk’, has been included to provide a more comprehensive view of institutions’ exposures, consistent with the supervisory objective of capturing risks beyond the balance sheet.

i) D 10.00 – Mitigating actions: Exposures contributing to sustainability objectives

- This template corresponds fully to the template set out in the ITS on Pillar 3 disclosures. No structural changes, additional data points, or modifications have been introduced for supervisory reporting purposes.

- Its main purpose is to ensure that institutions disclose all exposures that mitigate climate-related risks, irrespective of their alignment with the EU Taxonomy. The template also captures investments in assets and activities contributing to climate change mitigation, climate change adaptation and other environmental objectives, including nature and biodiversity protection, thereby addressing both transition and physical risks.

j) D 11.00 – Exposures to Environmental Risks (Beyond Climate)

- This Consultation Paper proposes the introduction of a new reporting template, D 11.00 – “Banking book: Exposures to environmental risks (beyond climate) – Physical and transition risks.” The template shall be reported by large institutions, other listed institutions and large subsidiaries on an annual basis. Its purpose is to provide competent authorities with harmonised quantitative information necessary to assess institutions’ exposures to a broader set of environmental risk drivers, in line with the EBA’s mandate under Article 430(7) CRR to develop uniform reporting requirements for the effective prudential supervision of ESG risks.

- With the integration of ESG risks into the prudential framework under CRR3, institutions are expected to identify, manage and monitor not only climate-related risks but also wider environmental risks arising from biodiversity loss, ecosystem degradation, pollution, overexploitation of natural resources and invasive species. These environmental risks can materially affect institutions’ financial soundness through disruptions to counterparties’ operations, higher input costs, supply chain vulnerabilities or transition pressures linked to policy and market responses to nature loss. Such vulnerabilities may weaken counterparties’ creditworthiness and, through transmission channels, affect the resilience of institutions and the financial system. A dedicated reporting template is therefore needed to enable supervisors to understand the scale, distribution and drivers of exposures subject to environmental risks beyond climate. The need for consistent, comparable information is reinforced by the EBA Guidelines on the management of ESG risks (EBA/GL/2025/01), which emphasise that institutions should progressively develop tools and practices to assess a sufficiently comprehensive range of environmental risks, recognising that most are currently more advanced in their assessment of climate related risks.

- To meet these supervisory needs, the template structures information around the two key channels through which environmental risks materialise: (i) environmental impacts, capturing where a counterparty’s activities negatively affect nature (e.g. land, freshwater and ocean use change; pollution; overexploitation; invasive species); and (ii) ecosystem service dependencies, capturing where a counterparty relies on natural systems (e.g. water supply; provisioning; regulating; supporting or cultural services) for its operations. This approach, aligned with Task Force on Nature-related Financial Disclosures (TNFD) and NGFS guidance, enables supervisors to identify exposures vulnerable to the degradation of natural systems or to transition measures aimed at protecting and restoring biodiversity.

The template also includes a country breakdown (z-axis) to reflect the location dependent nature of environmental risks and incorporates FINREP-rooted credit quality metrics to ensure alignment with the wider ESG reporting framework. Similarly, as in template D05.00, the geographical breakdown has been set up at country level, and institutions shall report, in addition to the totals:

i. Country by country information, to be reported considering the materiality threshold for the geographical breakdown, and

ii. Other EU exposures

Accompanying documents

1 Draft cost-benefit analysis / impact assessment

As per Article 15 of Regulation (EU) No 1093/2010 (EBA Regulation), any draft implementing technical standards (ITS) developed by the EBA shall be accompanied by an Impact Assessment (IA), which analyses ‘the potential related costs and benefits’.

This analysis presents the IA of the main policy options included in this Consultation Paper on the draft ITS revising the ITS on supervisory reporting (Commission Implementing Regulation (EU) 2024/3117) regarding ESG (“the Draft ITS”). The analysis provides an overview of the identified problem, the proposed options to address this problem as well as the potential impact of these options. The IA is high level and qualitative in nature.

A. Problem identification and background

Following the integration of ESG risks into the prudential framework through CRR3, ESG risk management forms part of institutions’ regulatory obligations. Article 430(7) of the CRR mandates the EBA to develop and specify uniform reporting formats, frequencies and instructions necessary for competent authorities to monitor compliance with prudential obligations. Consequently, insofar as ESG risks are embedded within prudential requirements, the EBA is required to specify corresponding supervisory reporting to enable effective monitoring and consistent supervisory assessment across Member States.

B. Policy objectives

The draft ITS revising the ITS on supervisory reporting (Commission Implementing Regulation (EU) 2024/3117) regarding ESG (“the Draft ITS”) aims at developping and specifying uniform ESG reporting formats, frequencies and instructions.

C. Options considered, assessment of the options and preferred options

Section C. presents the main policy options discussed and the decisions made by the EBA during the development of the Draft ITS. Advantages and disadvantages, as well as potential costs and benefits from the qualitative perspective of the policy options and the preferred options resulting from this analysis, are provided.

Climate Change transition risk: Credit quality of exposures by sector, emissions and residual maturity –institutions, with assets above 30bn EUR, stress test related information

The ESG reporting framework will include data request related to Climate Change transition risk (Credit quality of exposures by sector, emissions and residual maturity). For institutions with total assets above 30 bn EUR (‘institutions >30bn’), that participate to the stress test exercises, the concerned template (D 01.00) has been seen as a possibility of requesting also credit and climate risk stress test related data. With this regard, the EBA considered two options.

Option 1a: Aligning the template D 01.00 with related pillar 3 template (with limited necessary additional data points)

Option 1b: Aligning the template D 01.00 with related pillar 3 template (with limited necessary additional data points) and adding stress test information requests

Option 1a, which consists in aligning template D 01.00 with the related Pillar 3 disclosure template and introducing only a limited number of additional data points, would maintain a straightforward reporting structure. The costs associated with this approach are to some extent driven by the new CRR ESG requirements themselves and the associated mandate to integrate these elements into supervisory reporting. However, Option 1a would not capture information needed for stress test exercises, which would require to request those in the ad hoc stress‑test data collections.

On the other hand, Option 1b extends the alignment with the Pillar 3 template by integrating some stress‑test information directly within D 01.00. Although it implies adding more columns - particularly for credit‑risk parameters - and expanding the sectoral breakdown with more granular NACE codes, this option provides a benefit as it is expected to reduce the need for separate, ad hoc stress‑test data collections. Consolidating supervisory ESG reporting and concerned climate and credit risk stress‑test information in a single template strengthens internal consistency, improves comparability, and streamlines data processes.

Based on the above, the Option 1b has been chosen as the preferred option and, for institutions >30bn, the Draft ITS will align the template D 01.00 with related pillar 3 template (with limited necessary additional data points) and add stress test information requests.

Obligor-level environment-related corporate exposures

A new template (D 04.00) on obligor-level environment-related corporate exposures for supervisory reporting purposes will be included in the ESG supervisory reporting. This template will replace one existing template (reported both in Pillar 3 and in the ad hoc supervisory reporting framework) on concentration of exposures towards top 20 polluting companies. With regards to the possible synergies of this new template with the Large Exposure template, the EBA considered two options.

Option 2a: Using the existing Large Exposure (LE) template to develop ESG reporting, including amendments to the LE reporting module

Option 2b: Developing a new ESG template, but leveraging on the one put in place for LE

Option 2a, which consists in adding the ESG reporting requirements directly on the existing Large Exposures (LE) template, would have the benefit of relying on a well‑established reporting structure already familiar to institutions. Nevertheless, the LE framework relies on prudential notions such as the group of connected clients, which do not naturally align with environmental‑risk concepts. Several core elements of the LE template are not relevant for capturing environmental risk exposures, and adapting them for ESG purposes could still not allow to provide with reasonable changes the granularity needed to identify environment‑related concentration drivers. It could also create overlaps between prudential concentration risk and environmental‑related concentration risk, reducing the clarity and conceptual coherence of the information reported.

On the other hand, Option 2b - developing a dedicated ESG template inspired by the obligor‑level structure of the LE reporting - offers a simpler approach. This option allows the framework to capture environmental‑related concentration risks in a manner that is better aligned with ESG concepts and with the CRR definition of environmental risks, while preserving the usability of a familiar reporting logic. It provides the flexibility to design metrics specifically tailored to environmental risk drivers, ensuring a more accurate and meaningful representation of exposures. Furthermore, this choice is consistent with the short‑term recommendations of the EBA’s 2023 Report on the role of environmental and social risks in the prudential framework, which called for the development of exposure‑based metrics to quantify environment‑related concentration risks.

Based on the above, the Option 2b has been chosen as the preferred option and the Draft ITS will develop a new ESG template, but leveraging on the one put in place for large exposures.

Banking book – Indicators of potential climate change transition risk

With the integration of ESG risks into the prudential framework under CRR3, institutions are expected to identify, manage and monitor not only climate related risks but also wider environmental risks arising from biodiversity loss, ecosystem degradation, pollution, overexploitation of natural resources and invasive species. Such information will be requested in the ESG reporting for large institutions, other listed institutions and large subsidiaries on an annual basis. With regards to these information’s level of details to be reported, the EBA considered two options.

Option 3a: Including 4 templates to cover full range of data on environmental risks beyond climate (incl. risks and opportunities, nature-related foot-printing)

Option 3b: Covering only the necessary risk-relevant data in one single template

Option 3a, which would introduce four separate templates covering environmental impacts, dependencies, nature‑related opportunities and foot-printing indicators, would have the benefit of offering a broad and detailed view of environmental risks beyond climate. Nevertheless, internal analysis showed that such a wide‑ranging framework would introduce unnecessary complexity and significantly increase the reporting burden without delivering proportionate supervisory value. The dispersion of data across multiple templates could also reduce clarity and make it more difficult for supervisors to isolate risk‑relevant information.

On the other hand, Option 3b streamlines the framework by consolidating all necessary information into a single template focused on exposures to environmental risks beyond climate via impact drivers and ecosystem‑service dependencies. This approach ensures proportionality, avoids excessive granularity that provides limited supervisory benefit, and keeps the structure focused on metrics that are directly relevant for risk assessment.

Based on the above considerations, the Option 3b has been chosen as the preferred option and the Draft ITS will cover only the necessary risk-relevant data in one single template.

D. Conclusion

The development of the draft ITS revising the ITS on supervisory reporting (Commission Implementing Regulation (EU) 2024/3117) regarding ESG is intended to develop and specify uniform ESG reporting formats, frequencies and instructions. Overall, benefits are expected to exceed the incurred expected costs.

2 Overview of questions for consultation

Proportionality and scope of institutions

- Do you have any comments on the comprehensive approach proposed for large institutions?

- Do you have any comments on the simplified approach proposed to Other listed institutions and large subsidiaries?

- Do you agree that large subsidiaries should report ESG risk exposures using the simplified reporting approach, in line with the proportionality principles applied to other institutions and similarly as in the Pillar 3 framework?

- Do you have any views on the reduced and essential set of information applicable to SNCI and Other non-listed institutions?

- Do you have any views on the proportionality approach proposed?

- Are the proposed materiality thresholds for geographical breakdowns sufficient to provide meaningful reporting without imposing undue reporting burden?

- Is or are there any element(s) of this proposal for new and amended reporting requirements that you expect to trigger a particularly high, or in your view disproportionate, effort or cost of compliance? If yes, please:

▪ specify which element(s) of the proposal trigger(s) that particularly high cost of compliance,

▪ explain the nature/source of the cost (i.e. explain what makes it costly to comply with this particular element of the proposal) and specify whether the cost arises as part of the implementation, or as part of the on-going compliance with the reporting requirements,

▪ offer suggestions on alternative ways to achieve the same/a similar result with lower cost of compliance for you.

D 01.00 – Climate Change Transition Risk: Credit quality of exposures by sector, emissions and residual maturity

- Do you have any views on the additional information included for supervisory reporting purposes in template D 01.00?

- The EBA is assessing the introduction of data points requesting RWA in Templates D 01.00 and D 05.00 to enable national authorities to calculate potential Systemic Risk Buffer (SyRB) in case of systemic risks. What are your views on the inclusion of this information, both from an operational and from a macroprudential perspective? Do you foresee significant operational challenges related to the inclusion of this information? What alternative approaches would you suggest?

D 01.02 – Climate Change Transition Risk: Credit quality of exposures by sector, emissions and residual maturity

- Do you have any views on the proposed template D 01.02?

D 01.01 – Simplified ESG Information (for SNCIs and other non-listed institutions)

- Do you have any views on the proposed Template D 01.01?

D 02.00 – Climate Change Transition Risk: Loans collateralised by immovable property

- Do you have any views on the proposed Template D 02.00?

- Do you have any comments on the inclusion of information on covered bonds?

- Do you have any comments on the new column for EPC estimates?

- To what degree do institutions consider assessing transitions in the energy performance of collateral (e.g., EPC label or energy performance score categories) to be relevant for evaluating the evolution of transition risk exposures and enhancing transparency on improvements in energy efficiency of CRE and RRE portfolios? Please indicate how such transitions are currently monitored for both existing collateral and newly originated loans.

- To what degree do institutions consider that adding the same information on LTV buckets by EPC label and energy performance score categories for RRE exposures as for CRE exposures would facilitate identification of risk concentrations, improve comparability across portfolios, and support more effective prudential assessment?

D 03.00 – Indicators of potential transition risk: Emission Intensity by Sector

- Do you have any views on the proposed Template D 03.00?

D 04.00 – Obligor-level environment-related corporate exposures

- Do you agree with the proposed sectoral scope for D 04.00?

- For the purpose of obligor-level information requested in this template, do you agree that output-denominated emission intensity is more comparable and informative compared to revenue-based emission intensity? Please justify your view.

- Do you have any views on the list of sectors proposed for this template?

- Do you have views on whether the absolute 10 Mn Eur threshold could be replaced by a relative threshold (e.g. obligors representing above x % of total NFC exposures)?

- Do you have views on how to define the threshold in addition to the EUR 10 million exposure threshold (e.g. total number of obligors to be reported per institution or other Tier 1 capital-based relative threshold)?

- Do you have any other comments on Template D04.00?

D 05.00 – Mitigating actions: Exposures contributing to sustainability objectives

- Do you have any views on the additional information included in D05.00 for supervisory reporting purposes?

- What would be the most appropriate way to assess the extent to which exposures are (“adequately”) insured against relevant hazards? In particular, would the inclusion of a single column indicating the percentage of insured exposures be sufficient? How to deal with potential State insurance schemes?

- What information can credit institutions provide regarding the insurance coverage of their exposures? In particular, please indicate whether institutions can report: (i) the existence of active and up-to-date insurance coverage for a given exposure; (ii) the insured amount as a percentage of the exposure; (iii) the types of hazards covered by the insurance policy; (iv) whether the insurance is held by the institution or by the borrower; (v) whether reporting should be limited to real estate-related exposures or may also include non-real estate exposures; and (vi) any other relevant information (please specify).

- To better monitor the risk and losses stemming from physical impacts. Do you agree to include information on exposures highly and moderately exposed to physical risk?

- Do you have alternative proposals to reflect the vulnerability of institutions’ portfolio and the potential damage that physical hazards could cause them?

- Do you have any views on whether additional information on expected losses, (excluding insurance) and reflecting the accurate vulnerability, including damage functions, would be useful?

D 05.01 – Climate change physical risk: Exposures subject to physical risk (simplified)

- Do you have any views on the proposed Template D 05.01(simplified)?

D 10.00 – Exposures Contributing to Sustainability Objectives

- Do you have any views on the proposed Template D 10.00?

D 11.00 – Exposures to Environmental Risks (Beyond Climate)

- Do you have any views on the proposed Template D 11.00?

- Do you have any views on the materiality threshold introduced in this template?

3 Illustrative examples on D05.00 reporting of exposures subject to physical risk (high and moderate exposure)

- The following information and examples are included solely for illustrative purposes to clarify the reporting of template D 05.00. The examples presented in this document are intended for illustration only.

- For the purpose of the reporting of template D 05.00, an exposure is considered “subject to physical risk” when the underlying asset, activity or collateral is geographically located in an area identified as exposed to a recognised physical hazard. The concept refers to the structural presence of the exposure in a hazard-prone area, irrespective of whether a damaging event has occurred or is expected to occur in the short term.

- The notion of being “subject to” physical risk therefore reflects geographic co-location with a hazard, not the expected financial loss, nor the probability of default of the counterparty. It is a location-based assessment that precedes any modelling of vulnerability, damage, insurance coverage or credit deterioration.

- In practical terms, the classification is based on the intersection between (i) the geolocation of the underlying property or assets and (ii) officially recognised hazard maps (e.g. flood maps, heat stress maps, wildfire risk maps). Where such an intersection exists within predefined hazard thresholds, the exposure is deemed to be subject to the corresponding physical risk.

- This assessment is independent of:

- the financial strength of the borrower,

- the existence of insurance coverage,

- adaptation or mitigation measures,

- or any forward-looking assumptions regarding climate change.

Those elements may affect the magnitude of potential impact, but they do not determine whether the exposure is subject to the hazard.

Consultation paper and Annexes |