Executive Summary

Efficient reporting: simpler, smarter, proportionate Driving EU‑wide harmonisation of reporting requirements, with a holistic push for simplification across all actors. Making reporting more integrated, efficient and supervisory‑relevant, ensuring that every template and definition serves a clear purpose and paves way for data sharing. Leveraging modern tools and technologies to unlock efficiency gains and future‑proof the EU reporting framework. |

The European Banking Authority (EBA) is advancing a comprehensive set of simplification and efficiency measures to ensure that supervisory reporting across the EU becomes simpler, smarter and more proportionate. Building on the recent 2025 Report on the efficiency of the regulatory and supervisory framework and the 2021 Cost of Compliance study, the current package represents the most wide‑ranging review of the reporting framework in over a decade.

This initiative takes a holistic approach: it addresses both the stock and the flow of EU‑level reporting requirements; it strengthens coordination of European and national reporting; and it lays the foundations for integrated reporting and enhanced data sharing.

The centrepiece is a comprehensive revision of the ITS on supervisory reporting. The latter rebalances the framework towards ‘need‑to‑have’ information and delivers a 16% reduction in data points in the EU harmonised reporting framework, complemented by lower frequencies, increased proportionality and the integration of ad hoc data collections. Additional regulatory‑driven amendments introduced in the consultation paper, such as the implementation of IFRS 18, ESG integration, and adjustments related to the Fundamental Review of the Trading Book (FRTB), ensure that the reporting framework remains aligned with supervisory needs.

Moreover, the stress testing data collections are reduced by around 55% data points including through better integration into harmonised reporting, and the volume of supervisory benchmarking reporting by up to 65%, particularly for credit risk and IFRS 9 portfolios.

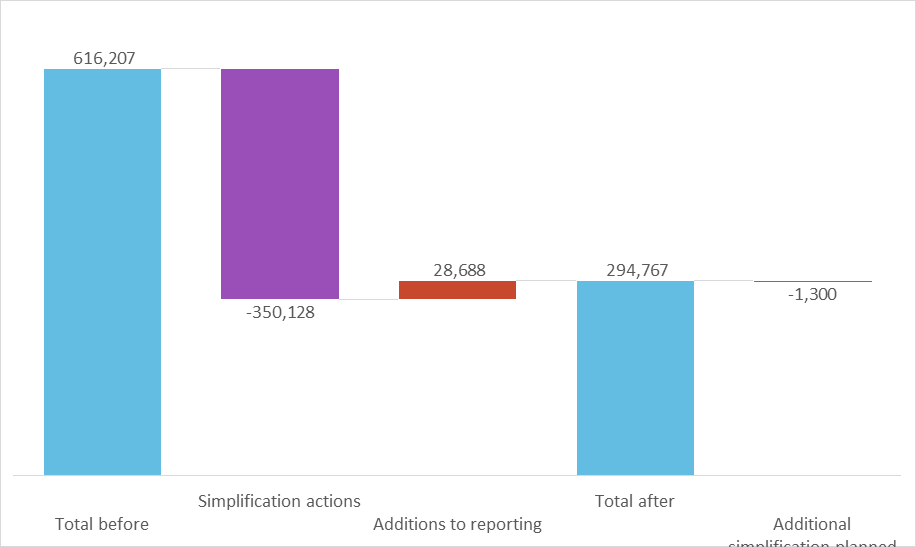

Taken together, these measures deliver an overall net reduction of around 50% in the data points of the EU harmonised reporting framework covering both the regular reporting and EU-wide stress test data collection, even after accounting for necessary additions.

Proportionality is a cornerstone of EBA’s approach. SNCIs, which already report only 49% of total reporting requirements, would see a further 18% reduction in reported data points from the simplification measures proposed, with additional benefits expected from reduced reporting frequencies. Revisions to the credit risk framework or the SNCI regime as recommended by the 2025 Report on the efficiency of the regulatory and supervisory framework may yield further substantial reductions in their reporting burden.

Beyond the EU‑level harmonised reporting, to reduce the overall burden, the EBA has carried out a stocktake of 2025 national supervisory data requests. It revealed the existence of 671 such requests totalling almost 980 thousand data points. Competent authorities have however already implemented or planned simplifications reducing national reporting data points by 17.4% for the data request by the EEA national competent authorities and 18.5% for SSM data requests.

The EBA is establishing an EU‑wide public repository of supervisory data requests to increase transparency, avoid duplication, and support data sharing amongst EU-level and national authorities. Complementary guidelines on data‑request practices will support how authorities design, coordinate and record their respective requests.

In line with the long‑term vision set out in its 2025 Report on the efficiency of the regulatory and supervisory framework, the EBA continues advancing integrated reporting alongside the ECB, SSM and SRB and national authorities through their Joint Bank Reporting Committee (JBRC). The first objective is to build a common data dictionary, harmonised definitions, and semantic integration across supervisory, resolution and statistical reporting. While integrated reporting may increase granularity, it should simplify design, reduce overlaps and support greater automation, improving efficiency for both banks and authorities.

The EBA also continues to provide modern technical foundations and innovation. The transition to ‘Data point Model (DPM) 2.0’, combined with the rollout of ‘DPM Studio’ and an enhanced glossary of concepts, will modernise the entire reporting lifecycle and support future integration with ECB statistical reporting. Improvements to modelling tools and to the publication process—such as XBRL CSV taxonomies, improved technical packages, and new tools like the Reporting Time Traveller and Signposting Tool—strengthen clarity, usability and predictability for institutions.

The successful launch of the Pillar 3 Data Hub in February 2025 demonstrates the benefits of improved data sharing, harmonisation and machine‑readable disclosure formats.

The EBA is also strengthening change management practices. Key improvements envisaged include enhanced impact assessments, clearer communication of upcoming changes, more explanatory material, move towards one or two annual releases for reporting changes only. The current simplification package will already create a two‑year period of stability ahead of a September 2027 implementation.

1. Continuous commitment to efficiency and simplification of supervisory reporting

The EBA has striven from its inception to build a harmonised EU wide reporting framework. This brings direct efficiency, simplification and supervisory convergence benefits compared to having 27 separate national frameworks. Harmonised data support efficient supervision and ensured level playing field across the EU.

EU-level supervisory reporting has been developed in stages following the developments and the expansion of the underlying regulatory framework. The key element omnipresent in all EBA work, including supervisory reporting is proportionality, which remains a cornerstone of our approach to reporting and small and non-complex institutions (SNCI).

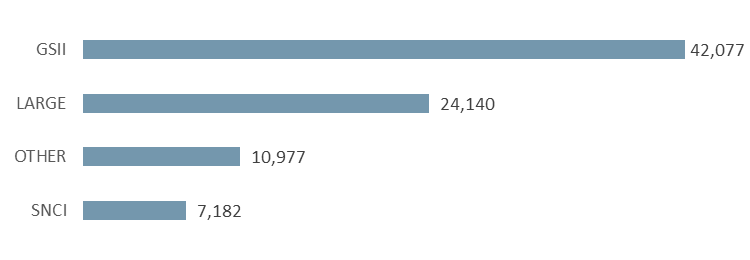

The EBA reporting framework exhibits a wide presence of proportionality, where numerous requirements are linked to institution type, activities, prudential approaches, thresholds. Over 66% of the full range of templates (covering 92,000 modelled/defined data points) have some kind of proportionality feature or simplification measure attached to. SNCIs are subject to reporting of only 45,000 data points (49% of total requirements). The proportionality is also evident in terms of the actual reporting volumes, where SNCIs report only 30% of data points compared to large institutions.

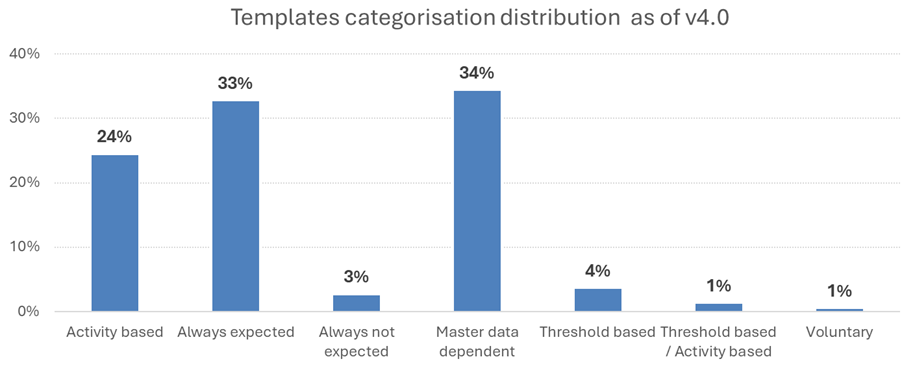

The EBA supervisory reporting framework has around 220 reporting templates of which 33% are always expected to be reported while the remaining templates are subject to different criteria to trigger the reporting obligation. These templates are reported for activities banks are carrying out (e.g. only banks have securitised assets, issuing covered bonds or certain type of hedging), applicable to banks with advanced approaches (e.g. IRB, IM) or certain size category (SNCI, other, large) or based on thresholds (e.g. foreign exposures, high NPLs).

The EU-level reporting is often supplemented with the competent authorities’ national reporting requirements and ad hoc information requests by various public authorities. Regardless of their relevance, these requests often lack coordination, albeit there are notable coordination initiatives (ECB within the SSM), but those do not cover the whole spectrum and all Member States.

Over the years this common reporting framework has been subject to various simplification and enhancements including recently through the 2021 study on the cost of compliance with supervisory reporting[1]. Most of the recommendations from this report have been largely completed (see Annex 1) leading to up to 25% reduction in estimated reporting costs primarily for small and non-complex institutions (SNCI)[2].

However, despite these past simplification efforts, there are still shortcomings in coordination efforts and the reporting framework remains complex mostly due to the complexity of the underlying regulatory framework. Furthermore, over time, continuous regulatory changes and the need to have information on new risks have notably expanded our reporting framework.

All of this, combined with the EU priorities to further strengthen the competitiveness of the EU banking sector, means it is time to pause, and have a holistic review with the aim of simplification, addressing both the existing stock of requirements and the flow of new ones, national and EU reporting while maintaining an effective and prudent supervision.

The current simplification efforts follow the publication of the 2025 Report on the efficiency of the regulatory and supervisory framework[3], and seek further streamlining and simplification of the supervisory reporting requirements both at the EU and national level as well more stability in reporting requirements, more predictability and coordinated changes across different types and requesters of data would also avoid unwarranted reporting burden. These are not a one-off initiative, but a part of a consistent work on building efficient and proportionate EU-wide harmonised reporting requirements.

The EBA objectives in this regard are fully aligned with the European Commission’s 2024 work programme and data strategy on long‑term competitiveness call for reduction in reporting costs through streamlined requirements, greater re‑use of data and improved data sharing among authorities. In the EBA view, the simplification measures introduced in this consultation paper combined with other ongoing and planned initiatives in the area of supervisory reporting deliver the expected degree of cost savings, but this need to be confirmed through the industry response to the consultation.

2.Simplification and efficiency proposals

2.1 Current proposals for simplification of the EBA supervisory reporting framework

A major part of the EBA supervisory reporting requirements is currently laid down in Commission Implementing Regulation (EU) 2024/3117 (ITS on supervisory reporting requirements) that serve as a cornerstone for supervisors’ ability to monitor institutions’ compliance with prudential rules and to assess financial soundness. After 15 years of harmonisation and given the focus of the policymakers across the EU on the simplification and streamlining of the regulatory framework and the breadth of recent regulatory, accounting and supervisory developments, a comprehensive review of the ITS on supervisory reporting was considered warranted.

The simplification and revisions of the EBA reporting framework are mainly channelled through a comprehensive consultation paper on revision to the ITS on supervisory reporting requirements that tackles the main areas of reporting and puts together simplification proposals, regulatory driven amendments and enhancements based on supervisory experience. To complete the package of simplification proposals, this comprehensive consultation paper is complemented by another consultation paper setting out the proposals for the improving and simplifying the supervisory benchmarking exercises and the associated reporting.

The simplification proposals set out in both consultation papers focus on (1) a reduction of data points and templates, (2) a reduction of frequency and scope adjustments, (3) introduction of greater proportionality for SNCIs, (4) introducing synergies though the integration into regular reporting and streamlining of separate data collections such as EU-wide stress testing and supervisory benchmarking and (5) qualitative effects, e.g. through better alignment of definitions.

In addition to the simplification proposals, the consultation paper also introduces regulatory-driven amendments and enhancements that are necessary due to the changes in the underlying regulatory requirements covered by the supervisory reporting. These notably include the adoption of IFRS 18 on presentation and disclosure in financial statements requires corresponding adjustments to FINREP reporting. Further drivers include the integration of environmental, social and governance (ESG) risks into prudential supervision, the review of certain reporting requirements on liquidity, asset encumbrance or FINREP to enhance them building on the lessons learnt from supervisory experience, and the forthcoming application of the revised market risk framework under the Fundamental Review of the Trading Book (FRTB).

With these proposals, the EBA would reduce the volume of the current supervisory reporting data points defined/modelled in the ITS on supervisory reporting by 16%[4] (see chart below), on a ‘need to have’ vs ‘nice to have’ basis, while ensuring that the framework remains fit for purpose. The simplification in practice would go far beyond, through reduction of frequencies and increased proportionality. Furthermore, efficiency gains will be higher through the integration of the national data collections into regular EU reporting, better focusing on the data needed for the supervisory purposes, and promoting supervisory convergence. These measures are not reflected in the reduction of the modelled/defined data points, but are expected to significantly contribute to the overall reduction of the reporting costs by institutions, to which the EBA is seeking industry feedback as part of the consultation process. From the perspective of proportionality, the impact of the proposed simplification actions is even more pronounced for SNCI through the reductions of the specific data points and frequencies mostly benefiting SNCIs.

The streamlining of the stress test data requests is expected to lead to around 55% reduction of the data points compared to those requested in the last EU-wide stress testing exercise, and the integration of the most stable part of those data requirements into the regular data supervisory reporting as part of the ITS on supervisory reporting will contribute to the stability and predictability of this data request and related cost reduction.

The simplification and streamlining of the supervisory benchmarking exercises carried out by the EBA will also have immediate effect on the related part of the supervisory reporting, in particular for credit risk and IFRS 9 benchmarking. The simplifications proposals under a separate public consultation include revisions and streamlining of the required data points and portfolios in the scope of the benchmarking, and the integration of the data collections into the regular supervisory reporting under the ITS on supervisory reporting. These simplifications are expected to bring significant impacts the overall reporting burden reduction by up to 65% in terms of volume of the reported data points.

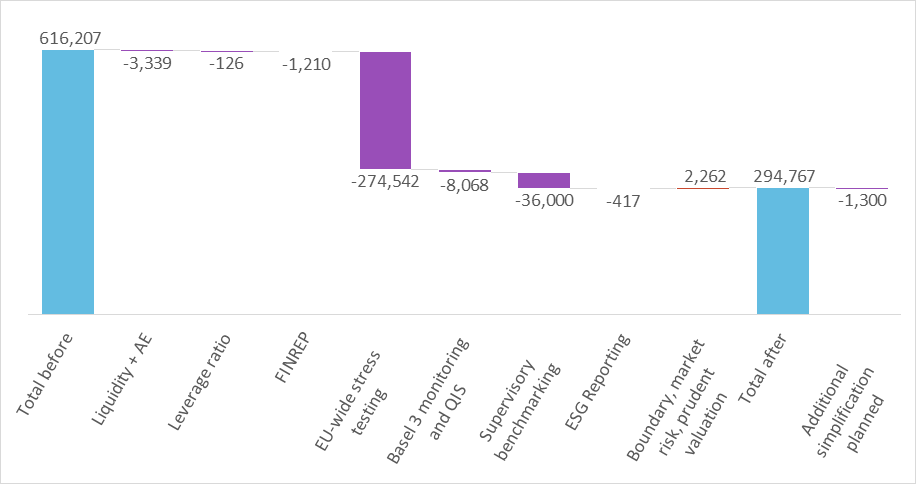

Notes: Totals include data points for the EBA reporting framework, EU-wide stress testing, supervisory benchmarking, Basel III and QIS and ESG reporting. Basel III monitoring and QIS considered as average for all types of institutions covered excluding crypto and trading book IMA backtesting P&L data requested for BCBS-monitored banks. Supervisory benchmarking data is approximation based on average submitted data points for banks covered due to open-ended nature of all templates and portfolios count. Additional simplification includes high-level estimated for funding plans and remuneration, but excludes IRRBB and credit risks, where simplification proposals are not elaborated.

Notes: Totals include data points for the EBA reporting framework, EU-wide stress testing, supervisory benchmarking, Basel III and QIS and ESG reporting. Basel III monitoring and QIS considered as average for all types of institutions covered excluding crypto and trading book IMA backtesting P&L data requested for BCBS-monitored banks. Supervisory benchmarking data is approximation based on average submitted data points for banks covered due to open-ended nature of all templates and portfolios count. Additional simplification includes high-level estimated for funding plans and remuneration, but excludes IRRBB and credit risks, where simplification proposals are not elaborated.

Considering the proposed simplification measures in the ITS on supervisory reporting, streamlining of the EU-wide stress testing data needs and simplification and integration of supervisory benchmarking reporting, the overall reductions from the simplification actions, after considering necessary increases of the data points, where relevant, lead to an overall net reduction of data points in the EBA reporting framework by around 50%[5].

Additional impacts on the reduction of the reporting costs may come in the future from the implementation of a number of other recommendations set out in the 2025 Report on the efficiency of the regulatory and supervisory framework, notably those on credit risk simplification and revision of the SNCI perimeter. To this end, changes in the credit risk framework may lead to further simplification of COREP credit and counterparty risk reporting that are currently not subject to changes in the consultation paper. Furthermore, potential expansion of the SNCI perimeter through the changed SNCI criteria will naturally lead to the reduction of the overall reporting burden, as more banks would move to the SNCI category, which is subject to significantly lower reporting requirements. The potential effects of both actions on supervisory reporting are not currently considered, but can be substantial, especially in the case of the expansion of the SNCI perimeter.

2.2. Future planned work

The EBA does not stop with the simplification and efficiency agenda with the publication of the proposals set out in the consultation paper on changes to the ITS on supervisory reporting and supervisory benchmarking. The short- to medium-term agenda for further simplification actions in relation to supervisory reporting envisage further simplification actions:

- As part of the consultation, the EBA is seeking stakeholders' input on the potential review of the reporting on interest rate risk in banking book (IRRBB), which is not included in the current round of the revisions. Based on feedback received the EBA will evaluate the areas for potential improvement and simplification and will consider this for future updates of the EBA reporting requirements.

- In response to 2025 Report on the efficiency of the regulatory and supervisory framework the EBA is working on simplification of remuneration and diversity benchmarking. The simplification measurers adopted in that area will also benefit the simplification of the associated reporting requirements.

- The EBA is also planning to review its Guidelines on funding plans reporting with the aim of significant streamlining the content to reduce reporting burden and to ensure that the data meets the needs to supervise liquidity and funding risks. Preliminary analysis shows that the scope of simplification could range between 20% to 30% of the data points. The work on revision is expected to proceed once the current changes to the ITS on supervisory reporting are finalised.

- As part of the revision of the securitisation requirements, the EU Commission is looking at adding more proportionality to the due diligence and transparency rules set out in the Securitisation Regulation. As part of the proposals the EU Commission is aiming at streamlining the requirements for the disclosures that the needs to be made available to investors in case of public and private disclosures that are set out in the templates developed by ESMA. In particular, to lower the reporting and compliance burden, the EU Commission proposal has suggested to streamline the current templates by reducing the number of data fields by more than 35%, where possible, and consider differentiating between mandatory and voluntary fields and remove loan level information for highly granular and short-term asset types (e.g. credit cards). Furthermore, it is suggested to introduce a dedicated ‘lighter’ template for private securitisations tailored to supervisors’ needs leveraging on existing notification templates. This work is expected to proceed once the legislative changes are finalised.

Whilst the current focus of the EBA simplification efforts is primarily on the supervisory reporting, in line with the 2025 Report on the efficiency of the regulatory and supervisory framework the EBA is also intends to review and its resolution reporting requirements. This review will proceed once the current changes to the ITS on supervisory reporting are finalised.

2.3 A holistic approach to the reductions of the supervisory reporting requirements

An important premise state by the EBA in its 2025 Report on the efficiency of the regulatory and supervisory framework is the holistic approach to the reduction of the reporting burden of institutions. This means that there is a shared commitment by the EU competent authorities not only to simplify the EBA reporting framework, but also all additional national supervisory reporting and data requests that come on top of the EU reporting requirements.

To better understand the additional reporting requirements and data collections of supervisory information by the EEA competent authorities the EBA carried out a stocktake of supervisory data requests made by competent authorities to credit institutions in 2025. The stocktake also collected information on simplification measures already implemented or planned by competent authorities in relation to these data requests. The exercise represents a preparatory step towards the establishment of an EU‑wide public repository of supervisory data requests (see below).

The analysis shows that, in 2025, competent authorities across the EEA conducted a substantial number of structured microprudential supervisory data requests (671 requests totalling 978,109 requested data points) addressed to banks and their branches. These requests covered a wide range of topics and were predominantly of a regular and recurring nature, with quarterly, annual and monthly reporting frequencies prevailing.

As part of the holistic approach to reducing the overall supervisory reporting burden, the competent authorities reported having implemented or planned simplification measures for a material subset of data collections. These measures primarily relate to the decommissioning of data requests, reductions in the number of requested data points, reductions in reporting frequency or reporting population, and the restructuring of data collections. The extent and penetration of simplification measures vary across jurisdictions, with some authorities applying simplifications to a relatively large share of their ongoing data requests. In aggregate, the reported measures are expected to lead to a meaningful reduction in the overall volume of requested data points, complementing the simplification initiatives already announced at ECB level for SSM‑wide data collections. The overall impact of the executed or planned simplification measures in terms of the data point reduction can be estimated at 17.4% reduction of data points for the data requests by the EEA national competent authorities and at 18.5%[6] for SSM data requests (comparing the number of the data points affected by decommissioning or data point reduction-related simplification measures compared to the amount of data points requested in 2025).

2.4 Improving coordination and raising transparency and accountability for national reporting

To support the holistic approach to the simplification of the supervisory reporting requirements both at the EU and national level, as part of the Implementation of 2025 Report on the efficiency of the regulatory and supervisory framework the EBA is advancing two major simplification initiatives: establishing an EU‑wide public repository of supervisory data requests (Recommendation 6) and developing harmonised ‘common rules of the game’ to coordinate data‑request practices across EU and national authorities (Recommendation 7). Together, these measures aim to enhance transparency, reduce duplication, promote convergence of supervisory practices, and support more efficient monitoring of reporting burdens across the EU.

The EBA is creating a public EU‑wide database that records structured and ad‑hoc data requests issued by competent authorities and, later, resolution authorities.

For the benefit of wider public, the repository will provide details on the data requests offering as much transparency regarding data requests without jeopardising confidentiality of the supervisory information, where relevant.

For the benefit of the competent and resolution authorities that will have unrestricted access to the repository, the repository will list descriptions of data requests and include empty templates used for the data requests (but will not contain institution‑specific data collected based on those data requests). The repository will allow competent and resolution authorities to record their requests, search existing ones, download templates, and initiate data‑sharing requests through the platform.

The repository will add to the accountability of the competent authorities to their commitment to the holistic reduction of the overall reporting burden of institutions and, thus, will also facilitate the monitoring of trends and support the implementation of Recommendation 5 on reporting burden reduction by the competent authorities.

In setting up the repository, the EBA is closely working with the competent and resolution authorities and expects the repository to be fully functional in early 2027.

To support consistent practices across supervisors and fully operationalise the new repository, the EBA is also developing guidelines that will apply to the competent and resolution authorities and establish common principles for data requests. These will (1) aim to harmonise how competent and resolution authorities prepare and launch requests (e.g., common definitions, checking existing requests in the repository, consulting industry), and (2) introduce obligations for recording all relevant data requests in the EU repository.

With these guidelines the EBA is not intending limit supervisory powers nor reduce flexibility in crisis situations. Instead, these guidelines aim at increasing convergence of practices and will also enable peer reviews to assess alignment of national practices with common principles. The timeline for the development of the guidelines is aligned to the timeline of the repository.

2.5 Moving towards integrated reporting

In addition to the simplification and efficiency improvements the EBA is undertaking in a short-to medium-term, in line with the 2025 Report on the efficiency of the regulatory and supervisory framework the ultimate objective for the EBA for the long-term remains the move towards integrated reporting.

The EBA is committed to build a more integrated reporting system for the banking sector covering supervisory, resolution and statistical reporting and promote cross-sectoral integration efforts. The journey started from the 2021 feasibility study on integrated reporting[7] and went live with the establishment of Joint Bank Reporting Committee (JBRC) [8] together with the ECB.

Integration of reporting requirements is a major effort requiring investments from authorities and eventually from institutions, but it will lead to several benefits reducing costs of producing, collecting and using reporting. Integrated reporting should continue to be the flagship action to improve efficiency of reporting system.

Integrated requirements will streamline reporting requirements by ensuring common definitions, reducing overlaps and redundancies when building integrated glossary and a common data dictionary. These actions will ensure common understanding facilitating compliance, improving comparability of data, facilitate data sharing and enable improved digitalisation of reporting processes.

Integration of reporting can lead to more granular reporting, hence volume of reported data is expected to grow but design should be simpler, closer to institutions’ internal reporting systems, with data serving multiple purposes and uses for authorities and also at institutions.

The ongoing work on integrated reporting is led by the JBRC, which is an EU‑level advisory committee created to simplify, harmonise, and improve bank reporting across Europe. It helps to develop common definitions and standards for the data that banks are required to report for statistical, supervisory and resolution purposes. All European and national authorities contribute to this work and are committed to follow the JBRC advice to enhance integration of reporting, build an integrated glossary of harmonised definitions and a common data dictionary. Banking sector is involved in integration work via Reporting Contact Group bringing in resources and expertise to work together with authorities.

One of the main priorities of the JBRC is semantic integration. Authorities and industry[9] are working together[10] to ensure that concepts and definitions are harmonised and aligned across the three different areas of reporting, contributing to defining a common data dictionary and an integrated glossary. The concepts and definitions from the EBA consultation paper are subject to the JBRC work plan for 2026. The EBA is reaching out to the JBRC to provide the necessary details and support for discussing content of this consultation paper and how to achieve efficient design of reporting to ensure semantic integration of final reporting requirements. The EBA is committed to implementing the recommendations of the JBRC in the finalisation of the ITS on supervisory reporting.

The JBRC issued in January 2026 advice on ESG definitions[11]. The EBA has incorporated this advice into the proposals for ESG reporting presented in the consultation paper on the revisions to the ITS on supervisory reporting.

3.Technical enhancements and innovation

Since the beginning, the use by the EBA of the Data Point Model (DPM) standard for the structured representation of reporting requirements has enabled the integration of data and provided a clear, machine readable structure for reporting requirements. The recent evolution to DPM 2.0 brings major improvements, as it allows for better representation of concepts, supports more use cases—from statistical to transactional data—and covers the entire reporting lifecycle.

The evolution to DPM 2.0, developed together with EIOPA, is bringing major improvements. It allows better representation of concepts, supports more use cases—from statistical to transactional data—and covers the entire reporting lifecycle, from data definition to data dissemination, including data relationships and lineage. It also enhances integration of diverse data granularities and introduces an improved business expression language for validations and calculations. DPM 2.0 allows us to be better prepared to integrate with ECB statistical reporting. Transition to DPM 2.0 and the new glossary has been gradual, starting in 2024 and finalising in 2025 with the publication of the reporting framework 4.2.

The EBA has also revised our glossary of concepts, to enhance definitions, avoid duplications and ensure harmonisation across our modules – all as part of the DPM quality review project. This, together with DPM 2.0, allow the EBA to be better prepared for the work on integrated reporting. Changes in the DPM have been also supported by the roll out of the new data modelling tool - DPM Studio, which enables more agile development and earlier production of technical packages.

In 2026 new project under Digital Europe Programme will support building a common European data dictionary for banking and insurance and further enhance the DPM 2.0 standard and related tools[12]. This digital infrastructure will facilitate compliance with reporting requirements, improve data quality and facilitate data sharing and building an integrated reporting system.

The EBA is also doing a big effort to modernise its tools, in particular tools facilitating understanding of the applicable reporting requirements such as Reporting Time Traveller, Signposting Tool, Mapping Tool to improve accessibility of information. The EBA also enhanced the process for the publication of our technical packages (DPM database, validation rules and taxonomies), with the publication of draft versions for comments and pre-announced fixed date for hotfixes. The improvements to the taxonomies have been facilitated by introduction of XBRL CSV taxonomies, replacing previously used XBRL XML.

Finally, one of the most significant recent achievements of the EBA has been the launch of Pillar 3 data hub, which is now fully operational for large and medium institutions. It centralises Pillar 3 data from across the EEA, enhancing transparency and market discipline. The hub is a good example of data sharing and efficiency, as it provides centralised accessed to information so far spread on institutions websites, with harmonised machine-readable formats and easy to use tools. It will improve quality of data, reduce costs for key players, including banks for peer comparison.

4.Paving way for greater data sharing

The past and ongoing work of the EBA on enhancing the EBA reporting framework, advances in modelling tools, drive towards the integration of reporting as well as the initiatives in the area of coordination and transparency on the data requests by various authorities pave way for better data sharing amongst authorities. Sharing of data will greatly contribute to the reduction of reporting burden for the institutions by removing duplicative data requests.

The EBA work on cataloguing data requests by the competent authorities though the upcoming EU repository, would allow the authorities to identify the data that is being asked by other authorities form the same institutions allowing them to share the collected data between themselves.

From the EBA perspective, the EBA is itself making necessary steps toward the implementation of the recent EU data sharing regulation[13] and already provides transparency on the taxonomies and DPM and building common data dictionaries though the work on integrated reporting. The current work on the simplification of the requirements of the ITS on supervisory reporting also contributed to the objectives of the said regulation that expects periodic removal of the obsolete reporting templates.

The EBA actively facilitates sharing of its data that is made available to supervisors or other authorities such as the ESRB or ESAs. The EBA also facilitates data sharing and collaboration via shared platforms to build common monitoring tools or top-down stress testing based on shared data. The EBA’s European Data Access Portal (EDAP) provides data, registers and dashboards to the public, including Pillar 3 data hub.

5.Improvements to reporting change management framework

As part of the current consultation the EBA is advancing efforts to simplify and reduce the cost of supervisory reporting, with a strong focus on improving change management practices. This priority reflects consistent feedback from supervisors and industry stakeholders and is aligned with recommendations from the 2021 study on the cost of compliance with supervisory reporting and the 2025 Report on the efficiency of the regulatory and supervisory framework. The EBA has identified two main areas of improvement

- Enhancing communication and impact assessments

The EBA aims to increase transparency, provide earlier visibility of planned changes, strengthen ex‑ante impact assessments, and offer clearer explanations and practical examples in consultations. Good practices include improved calendars, structured consultation questions, systematic fitness checks of existing reporting, rigorous cost‑benefit analysis, and more explanatory materials and workshops.

- Improving the timing and stability of reporting changes

To reduce the burden of continuous change, the EBA is exploring less frequent and more predictable release cycles, ideally limiting updates to one or two batches per year. While full pauses in new requirements are difficult due to dependencies on underlying legislation, the current simplification initiative has allowed a two‑year period of stability ahead of the planned September 2027 implementation.

The EBA has already acted on several recommendations, such as redesigning its website and tools (e.g., Reporting Time Traveller, Signposting Tool, Mapping Tool) to improve accessibility of information. The current consultation introduces a modular format and a two‑step impact assessment process, seeking more detailed input from stakeholders, particularly on cost implications and on change‑management tools.

A key issue still requiring industry input is the alignment of reporting timelines with regulatory calendars. Constraints stemming from Level 1 legislation can limit the ability to batch or delay reporting changes. One possible mitigation under consideration is requiring reporting to start earlier—e.g., six months before regulatory requirements apply—to avoid supervisory blind spots. Any improvements in the change management, however, need to be considered in the context of the supervisory effectiveness and the ability to supervise newly applied regulatory requirements.

The stakeholders feedback to the consideration on improving reporting change management framework set out in Section 3.5 of the consultation paper is sought through response to consultation questions 3 to 7. |

Annex 1. Implementation of recommendations of 2021 study on the cost of compliance with supervisory reporting

Group | # | Recommendation | Addressee | Status | Implementation comments |

Changes to the development process for the EBA reporting framework | 1 | Signposting of overall regulatory requirements applicable to different proportionality categories of institutions | EBA | No action taken yet | The work has been delayed due to the resource constraints, but will be reassessed and covered by work under Recommendation 3 of 2025 Report looking at the digital overhaul of the Single Rulebook |

2 | Signposting of the EBA supervisory reporting requirements and identification of the reporting templates applicable to different proportionality categories of institutions | EBA | Completed | Available on the EBA website: Signposting Tool | |

3 | Apply a new reporting framework release at most once per year and provide materials and documents for implementation 12 months before the date of application (first reference date) of that release | EBA | Completed | Completed to a degree possible by the EBA, however, calendar of underlying regulatory changes may require separate release to allow for the implementation of the requirements. Is also followed in the current consultation paper on changes to the ITS on supervisory reporting. | |

4 | Include in the EBA consultation paper on changes to the ITS on supervisory reporting or as a separate reporting roadmap with forward-looking plan for new reporting requirements based on the regulatory pipeline and calendar | EBA | Completed | Completed by the EBA, however, calendar of underlying regulatory changes may require separate release to allow for the implementation of the requirements. Is also followed in the current consultation paper on changes to the ITS on supervisory reporting, which invites stakeholders’ feedback. | |

5 | Consider a more coordinated approach to introducing changes into the existing legislation or developing new legislation allowing for better ‘packaging’ of reporting changes and longer implementation time proportionate to the nature and scope of changes/new requirements | EU Commission, co-legislators | Completed | ||

6 | Better articulation of the reporting requirements - provide better additional reasoning and explanations of the use of reported information as well as examples for calculating certain data points in CPs and supporting material for ITS (e.g. explanatory note) | EBA | Completed | ||

7 | Provide instructions to the reporting requirements and other data collections in machine-readable format | EBA | Ongoing | Covered under Digital Europe Programme will support building a common European data dictionary for banking and insurance and further enhance the DPM 2.0 standard and related tools. Also advances in AI facilitate machine reading of the existing regulations. | |

8 | Further improving EBA internal processes to ensure that new reporting requirements are free from overlaps with already existing reporting, and also that redundant data points are removed from earlier releases | EBA | Completed | ||

Changes to the design of EBA supervisory reporting requirements and reporting content | 9 | Investigate possibility of enabling simplified reporting also at consolidated level (e.g. develop criteria for ‘group consisting predominantly of entities benefitting from the simplified reporting requirement’) where compatible with the level of application of the underlying legislation and data needs for performance of supervisory tasks | EBA, EU Commission | Completed | |

10 | Adopt a ‘core + supplement’ approach, when designing new reporting requirements as well as when revising existing requirements, where such approach is suitable | EBA | Completed | ||

11 | Exempt SNCI irrespective of their level of asset encumbrance from reporting the information included in the F 33-, F 34- and F 36-templates | EBA | Completed | ||

12 | Review the asset encumbrance definition to create a level playing field between entities applying different accounting standards | EBA | Completed | ||

13 | Changes to ALMM reporting requirements: - Exempt SNCI from reporting of C 68.00, C 69.00 and C 70.00 - Exempt medium entities from reporting of C 70.00 - Remove 1% thresholds regarding reporting of C 67.00 and C 68.00 | EBA | Completed | ||

14 | Review of the scope of application, the reporting frequency and/or the content of the reporting requirements identified as least important and least frequently used by data recipients | EBA | Completed | Reflected in the current consultation paper and simplification proposals | |

15 | Large exposures reporting: drop maturity bucket breakdown (mainly benefitting medium and large institutions) Leverage ratio: drop templates C 41.00 and C 42.00 - Develop dedicated and simpler reporting for entities applying the simplified NSFR - Other small changes (streamline information on transitional provisions, reduce frequency of reporting on losses stemming from immovable property exposures) | EBA | Completed | ||

Coordination and integration of data requests and reporting requirements | 16 | Commitment to better coordinate additional reporting requirements or data requests (at national or jurisdiction level) with the EBA reporting framework using the same definitions and taxonomy until the introduction of the integrated reporting the realisation of its benefits | National competent authorities, ECB, SRB | Completed | JBRC MoU Memorandum of Understanding on the establishment of the Joint Bank Reporting Committee between the European Central Bank and the European Banking Authority |

17 | Develop ‘best practice’ guidance for CAs for better coordination of ad hoc information requests in a form of modules of the EBA Supervisory Handbook | EBA, national competent authorities, ECB, SRB | Ongoing | Included as Recommendation 7 in the 2025 report and will be implemented through the upcoming guidelines on ‘common rules of the game’ for making and preparing data requests. | |

18 | EBA to maintain a simple repository of ad hoc requests that stakeholders could consult before making their own requests | EBA, national competent authorities, ECB, SRB | Ongoing | EBA maintains own repository of ad hoc data requests, the ECB maintains the repository for the data requests to significant institutions. The EU-wide repository is being established based on Recommendation 6 of the 2025 Report. | |

19 | Promote the work on integrated reporting as a way of reducing overlaps between the information reported to various stakeholders and differences in definitions/taxonomies | EBA, national competent authorities, ECB, SRB | Completed | ||

20 | Continue ongoing work on integration between reporting and disclosures | EBA | Completed | ||

Changes to the reporting process, including the wider use of technology | 21 | Wider use of better internal risk data aggregation and proportionate implementation of BCBS 239 as means to improve internal data management and simplify reporting preparation processes leading to the reduction of reporting costs | Large and, subject to the principle of proportionality, medium-sized institutions | Completed | |

22 | Better digitalisation of documents/contracts for all banks as a way to ensure that institutions have richer set of underlying granular data | All institutions | Completed | ||

23 | Raising awareness of institutions, and in particular SNCI, about possible use cases of FinTech/RegTech and their suitability to SNCI needs and specific business models, which might be beneficial for SNCI | EBA, Competent authorities | Completed | ||

24 | Industry trade bodies representing SNCI to work together with FinTech/RegTech providers to improve their understanding of technology needs of SNCI and see whether possible solutions could be found at costs that are affordable to SNCI | Industry trade bodies, FinTech/RegTech service providers | Completed | ||

25 | Develop guidelines (or recommendations) outlining resubmission policy | EBA | Completed | EBA Guidelines on resubmissions of historical data (EBA/GL/2024/04) |

[2] This estimation is based on the completed actions in response to the recommendation of the Cost of Compliance study considering the estimated impacts on the reporting costs of the original recommendations. As no follow up study or survey of the industry has been performed the estimations cannot be confirmed

[4] In the absence of data on potential cost impacts that is requested from the respondents to the public consultation, the best proxy for the impact of the simplification initiatives is the count of data points and comparing the count before and after the simplification initiatives.

[5] Net change of the data point count considering all simplification measures introduced and necessary additions of data points to the overall EBA reporting framework, including ITS on supervisory reporting, supervisory benchmarking, EU-wide stress testing data, Basel III monitoring and QIS.

[6] ECB report on streamlining supervision, safeguarding resilience (11 December 2025)

[7] See: https://www.eba.europa.eu/activities/single-rulebook/regulatory-activities/supervisory-reporting/integrated-and-consistent-reporting-system

[9] via the Reporting Contact Group (RCG), one of the permanent structures of the JBRC

[10] Expert Group on Semantic integration

[11] The Joint Bank Reporting Committee publishes its 2026 Work Programme and recommendations to enhance semantic integration on ESG definitions | European Banking Authority

[12] Development of a common data dictionary for reporting in the banking and insurance sectors and supporting IT tools and Design and proof-of-concept of a common master data management framework in EU financial services - EU Funding & Tenders Portal | EU Funding & Tenders Portal | EU Funding & Tenders Portal

[13] Regulation (EU) 2025/2088