Consultation Paper on Revisions to the ITS on supervisory reporting (Commission Implementing Regulation (EU) 2024/3117) - Module on other CRR3 driven amendments to supervisory reporting (IRRBB, large exposures - shadow banking exposures, leverage, resubmission/explanations, ITS changes)

The content on these interactive pages is provided for ease of reference and to assist in the reading and understanding of the Consultation Paper and it is not considered as the official version of such documents.

For the formal consultation papers and their components, please refer to the .pdf documents provided at the bottom of this page. In case of discrepancies between these interactive pages and the .pdf documents, the latter prevail as the authentic official versions.

Responding to this consultationPlease provide your responses by 10 July 2026 at 23:59 CEST via EU survey (Password for the survey: Reporting2026). Late responses will not be considered. |

1 Background and rationale

- This consultation paper brings together a set of amendments to the ITS on supervisory reporting that, while not falling within the main thematic areas of the consultation , remain necessary to ensure coherence, completeness and operational soundness of the reporting framework. The main purpose of the consultation is to seek feedback on changes proposed with the objective of simplifying the reporting framework for the reporting agents. It also includes changes that arise from targeted issues identified during the broader review process—such as corrections, clarifications, alignment needs, or updates triggered by parallel regulatory workstreams—and therefore complement the more substantial revisions presented in the earlier modules. Even though these items are not thematically linked to one another, each addresses a concrete reporting need or resolves an inconsistency that would otherwise persist in the ITS.

- Given the cross‑cutting nature of these adjustments, the current section serves as an umbrella for updates relating to IRRBB, large exposures (including amendments linked to shadow banking exposures), leverage ratio, resubmission and explanations processes, and other miscellaneous modifications to templates, instructions and legal ITS text.

1.1 COREP Large Exposures – exposures to shadow banking

- The CRR 3 introduced a definition of “shadow banking entities” in Article 4(1)(155). A shadow banking entity is defined as “an entity that carries out banking activities outside the regulated framework”.

- The shadow banking entities were already referred to in Article 394(2) of the CRR2 also setting out the current reporting requirements on the ten largest exposures to shadow banking entities. The criteria for the identification of shadow banking entities are set out in the Regulatory Technical Standards (RTS)on criteria for the identification of shadow banking entities which were adopted by the Commission Delegated Regulation (EU) 2023/2779 of 6 September 2023. These RTS build on the work undertaken for the EBA guidelines EBA/GL/2015/20.

- Under these RTS, entities offering banking services or performing banking activities and being not authorised and supervised in accordance with any of the Union acts listed in the Annex to Commission Delegated Regulation (EU) 2023/2779 of 6 September 2023 shall be identified as ‘shadow banking entities’. Furthermore, some exposures shall be regarded as exposures to shadow banking entities: exposures to money market funds, due to the risks they may pose in stressed market conditions; exposures to alternative investment funds where they employ leverage on a substantial basis, originate loans in the ordinary course of their business or purchase third-party lending exposures for their own account.

- The RTS also set out the cases of exclusions from being shadow banking entities considering different aspects, among which: the comparability, in terms of robustness, of the prudential requirements of third countries with the ones applied in the Union; the inclusion of the entity in the consolidated prudential supervision in accordance with the CRR; the application of the Basel Core Principles for effective banking supervision.

- The current regulatory framework is complemented by reporting requirements. Specifically, Article 394(2) of the CRR 2 requires institutions to report the 10 largest exposures to institutions, on a consolidated basis, as well as the 10 largest exposures to shadow banking entities, on a consolidated basis. In application of this article, the reporting framework 3.0 applicable from 30 June 2021 includes this information in templates LE1, LE2 and LE3. The exposure value calculated in column 0210(‘Total’) of template LE2 is the amount that shall be used for determining these 20 largest exposures.

- The CRR 3 has strengthened the current framework on exposures to shadow banking entities by introducing new additional reporting requirements, new disclosure requirements and new policy mandates.

- Regarding the additional reporting requirements, the amendments to Article 394(2) according to CRR 3 require institutions to report their aggregate exposure to shadow banking entities, on a consolidated basis and on a solo basis, in addition to the reporting of the 10 largest exposures to shadow banking entities. The same obligation is introduced for Pillar 3 disclosures purposes. Therefore, consistency and integration between reporting and disclosure requirements is being ensured.

- Regarding the policy mandates, the new paragraph 2a of Article 395 mandates the EBA to update the guidelines EBA/GL/2015/20 on the limits on exposures to shadow banking entities within 30 months after the date of entry into force of the CRR 3.

- The EBA is also required to submit a report to the Commission by 31 December 2027 and, on the basis of that report, the Commission shall, where appropriate, submit to the European Parliament and to the Council a legislative proposal on exposure limits to shadow banking entities by 31 December 2028.

- On a different topic, the labels of rows 0020 and 0030 of template C 26.00 (Large exposures limits) have been amended to align with Article 395(1) CRR as amended by the Corrigendum to Regulation (EU) 2019/2033 of 20 December 2020. Investment firms under Article 4(1)(2) CRR are no longer subsumed by institutions under Article 4(1)(3) CRR (also see Article 395(1) CRR, first subparagraph). In this regard, a reference to investment firms has been added in the labels of rows 0020 and 0030.

1.1.1 Proposed new template on aggregate exposure to shadow banking entities

- Building on the existing reporting under Article 394(2) of the CRR 2, requiring institutions to report the 10 largest exposures to institutions, on a consolidated basis, as well as the 10 largest exposures to shadow banking entities on a consolidated basis, the new template LE4 (C 37.00) to report aggregate exposure to shadow banking entities has been added in the large exposures module. Proportionality has been considered in this decision and it is expected that it would entail minimum costs for the institutions.

- More specifically, the new reporting template includes information on original exposures, for both direct and indirect exposures and in each case on-balance sheet and off-balance sheet exposures to shadow banking entities, as well as information on exposure values before and after the application of the exemptions of Articles 400 and 493(3) of the CRR and CRM techniques. This information is consistent with the one already required in the reporting template LE2 (C 28.00) and shall be reported at aggregated level.

- Since the current regulatory framework will be reviewed with the new policy mandates of Article 395(2a) of the CRR 3 and this will likely have an impact on the reporting and disclosure requirements, the latter have been kept as simple as possible for the time being. More granular breakdowns will be considered for the future, depending on these future policy mandates under the CRR 3.

1.2 Interest Rate Risk in the Banking Book

- In the area of interest rate risk in the banking book (IRRBB) reporting, stakeholders have indicated that the current reporting requirements remain burdensome and could be further streamlined. Several NCAs noted that, while the templates introduced under the revised framework have improved supervisory visibility, they also entail a significant operational effort, particularly for SNCIs. In this context, it was suggested that additional proportionality could be introduced, for example by tailoring the requirements further for SNCIs or by reconsidering the granularity of certain breakdowns, especially those captured as memorandum items.

- At the same time, it is important to acknowledge that the IRRBB reporting framework only started to apply recently, with first submissions taking place in 2024 with v3.4. Given this short implementation period, institutions are still in the process of embedding the reporting in their systems and processes, and the EBA has only limited evidence so far on how the framework operates in practice across different types of institutions. As a result, while the feedback received so far points to potential areas for simplification, a more complete assessment requires additional supervisory experience as well as more targeted input from reporting institutions.

- Against this background, the EBA considers it premature to introduce structural changes to the IRRBB reporting templates without first gaining a clearer understanding of the operational implications for institutions. In particular, while simplifications are often assumed to reduce burden, changes to reporting structures may also trigger system redesigns, re‑mapping exercises or adjustments to automated processes. These adaptations can, in some cases, generate non‑negligible implementation costs—especially given that institutions have only recently finalised the IT builds required for the IRRBB framework following its first reporting in 2024. The EBA therefore seeks more granular and experience‑based feedback from the industry on which specific elements are most resource‑intensive, and whether simplifications would genuinely reduce ongoing effort or instead risk creating additional adjustment costs.

- The EBA therefore invites stakeholders to provide detailed comments based on their initial rounds of IRRBB reporting, including concrete examples of operational challenges, system complexities or redundancies encountered. In addition, institutions are encouraged to clarify whether potential changes—such as the removal of memorandum‑item breakdowns or additional proportionality for SNCIs—would lead to meaningful and lasting reductions in reporting burden, or whether, given the early stage of implementation, such modifications would require system rebuilding that could outweigh the benefits. This feedback will be crucial in determining whether future revisions to the IRRBB reporting module are warranted and in ensuring that any streamlining measures are both effective and proportionate.

1.3 COREP Leverage ratio

- The reporting framework in scope of leverage ratio computation has been amended with the objective of reducing the reporting burden to institutions while at the same time making sure authorities have the necessary data to fulfill their mandates.

- The proposal put forward in this consultation paper envisions the following:

- reducing reporting frequency for template C 44.00 (LR5) from quarterly reporting to annual reporting. The underlying data is not expected to change significantly from quarter to quarter, so annual reporting is considered sufficient and reduces unnecessary reporting burden.

- While the template C 43.00 (LR4) is of great value to supervisors, balancing the costs and benefits of reporting this data, it is proposed that this template be discontinued.

- Feedback received from institutions pointed to the significant burden to report granular information on cash pooling in Template C 47.00 (LRCalc). In this respect, balancing costs and benefits, it is proposed to remove the granular rows 0193 to 0198 and instead require institutions to report an aggregated value.

- In addition, few rows are proposed to be removed in C 47.00 template referring to transitional arrangements which are no longer applicable, namely rows {0280, 0300, 0320, 0340, 0490}. Labels have been adjusted accordingly.

1.4 Voluntary reporting by small and non-complex institutions (SNCIs) and by institutions other than large institutions

- The reporting ITS includes specific provisions for SNCIs and for institutions other than large institutions (‘other institutions’) with the aim of avoiding triggering high compliance costs for smaller institutions. Still, SNCIs may want to report on a voluntary basis the information required for ‘other institutions’ or for ‘large institutions’, and ‘other institutions may want to report on a voluntary basis the information required for ‘large institutions’ pursuant to this Regulation, including reporting with the same frequency as those institutions.

- To this end, the ITS legal text has been amended to allow SNCIs to report as ‘other institutions’ or as ‘large institutions’ and ’other institutions’ to report as ‘large institutions’. The ITS legal text also clarifies that if an institution makes use of this provision, it should report the same set of information that is required for ‘other institutions’ or for large institutions, either for all the modules in the ITS, or only for some modules (e.g. COREP_OF, COREP_LR) and that partial application within a module is not allowed (i.e. it is not possible to voluntarily report only some templates in a module, because of technical reasons, like validation rules). In case an institution makes use of voluntary reporting it should notify the Competent Authority in advance.

1.5 Reasons for resubmission

- Since the introduction of harmonised supervisory reporting, supervisors and reporting institutions have increasingly recognised the need to exchange structured contextual information supporting the analysis of the quantitative data in the reports. In particular, dedicated communication channels have often been established to exchange information including: explanations for failing validation rules; information on resubmissions (i.e. information on what has changed and the reasons for the revisions); general comments on specific data points, tables, or templates reported in a submissions, or on the submission as a whole.

- At present, such “submission metadata” is exchanged outside the xBRL transmission channel, through ad‑hoc processes and bilateral communications.

- Considering also the involvement of different authorities in the exchange of submission metadata (including national authorities, the ECB for SSM countries, and the EBA), some shortcomings and inefficiencies have been identified in relation to this exchange of information, potentially leading to less-than-optimal supervisory processes and additional burden for the reporting entities:

- Information cannot be provided proactively at the time of submission by reporters; it can only be provided through side channels and may be requested multiple times by different authorities.

- Information must follow a multi-step chain (for example: from bank to NCA, to ECB, to EBA) through various channels, increasing operational burden and risk of inconsistency.

- Information is not integrated in the standard reporting-processing infrastructure and is not systematically replicated to all relevant authorities.

- It is difficult to link comments reliably and in a standardised way to specific reported data or validation rules.

- As a general observation, the ITS on Supervisory Reporting concerns the implementation of the reporting obligations mandated by the applicable regulatory framework and does not require the introduction of reporting elements to facilitate the collection of submission metadata. Nonetheless, the technical arrangements for the collection of supervisory reports, namely the IT solutions published by the EBA together with the EBA XBRL Filing Rules, can be considered a suitable instrument to standardise and streamline the reporting of submission metadata for the benefit of the users of the reporting framework.

- If technical arrangement were defined by the EBA for the collection of submission metadata, they would give the option to reporters to provide qualitative information to supervisors and other users of supervisory reporting. No new regulatory reporting obligations would be implied as a result of the addition of these technical solutions to the reporting framework: the decision to make use of the technical solutions for exchanging submission metadata would be left to the specific arrangements defined independently between supervisors and reporters, which would need to define the type, level and granularity of information to be provided in this way, if any.

- Allowing the inclusion of submission metadata directly within xBRL‑CSV submissions is expected to bring various benefits, including: reducing reliance on parallel communication channels and manual follow‑up; increasing timeliness and completeness of the contextual information available to all relevant authorities; providing a harmonised, standardised machine‑readable structure for comments.

- In line with the broader efforts undertaken by the EBA to simplify reporting processes and reduce the associated costs for reporting entities, this Consultation Paper also aims to assess whether the technical solutions proposed here would effectively contribute to these objectives. By offering streamlined and harmonised mechanisms for providing contextual information, the approaches presented have the potential to decrease operational burden, minimise duplication of work, and enhance the efficiency of supervisory interactions. It is therefore essential to gather feedback from respondents on whether any of the proposed solutions would bring tangible benefits in practice, including improvements in usability, clarity, or cost‑effectiveness, and whether alternative simplification opportunities should be considered.

1.5.1 Possible approaches for collecting submission metadata

- Following a feasibility analysis undertaken in 2025 within the EBA working structures, two possible technical solutions were identified for accommodating the collection of submission metadata within xBRL-CSV submissions:

- an approach relying on extending the metadata that can be included in the report.json file, which is part of the xBRL-CSV reporting package[1] (“report.json approach”); and

- an approach based on dedicated technical tables included in the reporting modules (“metadata as data” approach).

- Draft specifications were developed for both solutions with the objective to provide a standard, technology‑neutral way for reporting entities to submit structured textual comments together with the xBRL‑CSV reports. The specifications were designed to support the following use cases:

- Collecting comments relating to the report as a whole, or to specific modules, templates, tables or data points.

- Collecting comments on validation rule failures.

- Collecting comments on resubmissions, including comments explaining what has changed compared with the previous submissions at the level of the whole report, module, template, table or datapoint.

- Collecting the cause and originator of the resubmission, according to a standardised taxonomy.

- Collecting comments in multiple languages, where relevant.

- Collecting comments that may apply to multiple items (e.g. covering several data points or tables) without duplication.

- A brief description of the two solutions is provided in the following sections. It is important to note that the reporting of this metadata would be voluntary for reporting institutions and subject to each NCA to enforce it.

1.5.1.1 “report.json” approach

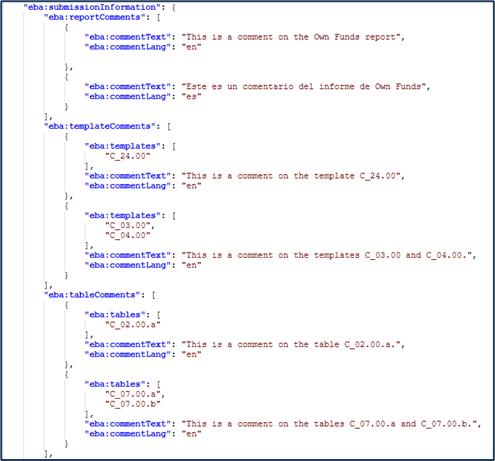

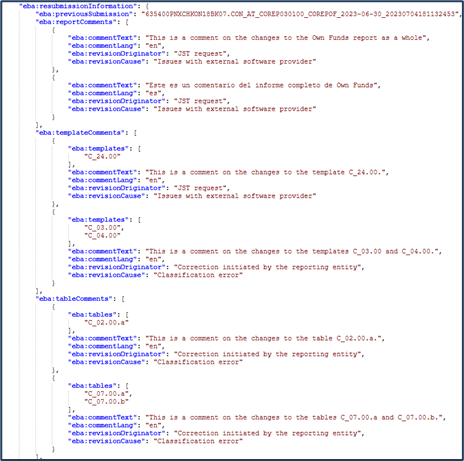

- Under this approach, the EBA XBRL Filing Rules would be amended to include the definition and technical specifications of additional JSON objects that could be reported inside the report.json file (similarly to the “eba:generatingSoftwareInformation” object defined in section 2.26 of the EBA XBRL Filing Rules), making use of the extensibility features foreseen in the xBRL‑CSV specification.

- The draft specifications for this approach envisage a dedicated root object (eba:submissionInformation) to host structured metadata about the submission. Within this object, reporting entities could provide information structured in various JSON elements:

- eba:reportComments – comments on the report as a whole;

- eba:templateComments – comments linked to specific templates;

- eba:tableComments – comments linked to specific tables;

- eba:datapointComments – comments linked to specific data points;

- eba:validationComments – comments linked to validation rules.

- Similarly, a root object (eba:resubmissionInformation) would be defined to host structured metadata about resubmissions, including references to previous submissions and dedicated fields for the originator and cause of the resubmission.

- A JSON schema would be provided to allow automatic validation of the structure of the reported information.

- The following images show examples of how the information could be structured in the JSON objects according to the draft specifications.

- The “report.json” approach has the following main advantages:

- It does not require structural changes to the reporting taxonomies: the solution is implemented entirely by extending report.json and is independent from the release of new versions of the reporting framework. The same approach can be reused across different reporting modules without revising each module.

- The JSON format is able to accommodate structured information (e.g. lists of template codes) in an organized and machine-friendly manner. This approach is flexible and can be extended in the future with no impact on the reporting taxonomies.

- The approach is transparent to entities that only pass the xBRL submission along the reporting chain and do not need to extract the additional information from “report.json”: if not used, the additional JSON objects can simply be ignored. Similarly, entities and authorities that do not intend to use the new JSON objects would not be impacted.

- The main disadvantage of the “report.json” approach is that all parties in the reporting chain that want to supply or make use of the additional submission metadata (reporters, NCAs, ECB, EBA and any intermediaries) must undertake an implementation effort to be able to generate, parse, validate, store and present to users the information in the extended JSON structures. Supervisory systems and vendor solutions may require updates to fully support the new JSON objects.

- The requirement mentioned above – that all parties involved in the data exchange implement the specifications as a prerequisite before the data exchange can be undertaken – constitutes a barrier which can delay or limit adoption.

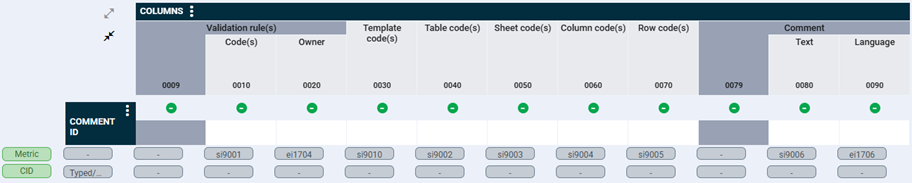

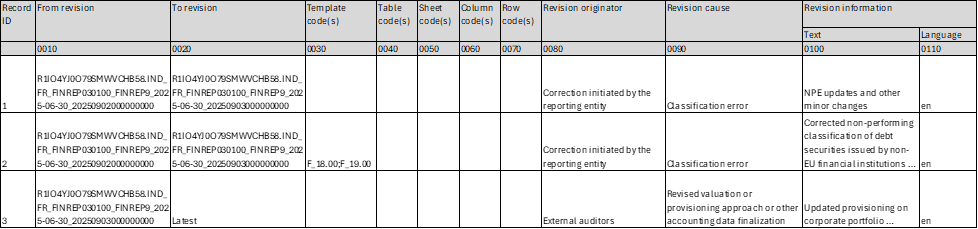

1.5.1.2 “Metadata as data” approach

- Under this approach, all reporting modules would be amended to include two new technical tables. These tables would be designed exclusively for metadata (e.g. comments on data points, explanations of validation failures, resubmission reasons).

- Following the draft specifications under discussion, the additional tables would be:

2) a table including information about the submission, with the following structure:

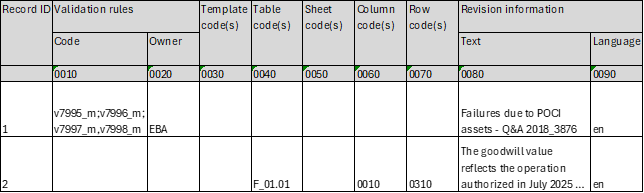

- The following images show examples of how the tables could be filled in by reporters:

- The key advantage of the “Metadata as data” approach is the reuse of existing reporting processes: once the templates are defined in the taxonomy, metadata can be reported, transmitted and processed with the same mechanisms as quantitative data, with limited need for separate technical infrastructure. The information would automatically flow to the final users in the same way as regular supervisory data. Moreover, the content of the metadata templates can itself be subject to validation rules, improving quality and consistency.

- On the other end, the design, modelling, review and maintenance of new templates for metadata imply taxonomy development and governance efforts. As the new templates are intended to apply to all reporting modules, a consistent approach in terms of governance, semantics and versioning is especially important. Changes and extensions would be tied to the release cycle of each reporting module, limiting flexibility.

1.5.2 Options considered

- The following four options were considered for the future treatment of submission metadata in the EBA reporting framework. Options a, b, c would introduce the technical possibility to transmit metadata within xBRL‑CSV submissions; Option d would maintain the current situation. Respondents are asked to choose the preferred option in the questions for consultation section.

Option a: adoption of the “report.json” approach.

- Under this option, the “report.json” approach described above would be adopted by releasing detailed specifications in a future release of the EBA XBRL Filing Rules (possibly accompanied by supporting artifacts, such as JSON schema files). From the entering into force of the new XBRL Filing Rules, authorities and reporters would have the option of implementing the specifications to support the exchange of submission metadata.

Option b: adoption of the “metadata as data” approach for all reporting modules at a specific time.

- Under this option, the “metadata as data” approach described above would be adopted in a dedicated release of the reporting framework (e.g. in version 4.3 of the reporting framework), by having new versions of all reporting modules included in the release, adding the technical tables for submission metadata in the new module versions. Dedicated reporting instructions would be provided as part of the IT solutions. This option concentrates the effort for the transition into a single release, making sure that from that release, submission metadata can be transmitted for all reporting modules.

Option c: adoption of the “metadata as data” approach for each reporting module with a staggered approach.

- Under this option, the “metadata as data” approach would be adopted gradually, by including the additional technical tables for submission metadata in each reporting modules whenever a new version of the reporting module is released. For example, the additional tables would be included in the 4.3 reporting framework for the modules subject to change in the 4.3 release, and would be included at a later stage for the other modules. Also in this case, dedicated reporting instructions would be provided as part of the IT solutions. This option spreads the transition effort across multiple releases of the reporting framework, but delays the adoption process.

Option d: no action.

- Under this option, the EBA reporting framework would not be extended to support submission metadata in xBRLCSV. Supervisors and reporting entities would continue to exchange explanations for failed validations, reasons for resubmissions and other comments through existing channels (email, portals, bespoke tools), outside the standard reporting flow.

2 Accompanying documents

2.1 Impact assessment

2.1.1 Options considered for the reporting of Large exposures – shadow banking entities template

This section presents the main policy options discussed, and the decisions made by the EBA during the development of the Draft ITS. Advantages and disadvantages, as well as potential costs and benefits from the qualitative perspective of the policy options and the preferred options resulting from this analysis, are provided.

Aggregate exposure to shadow banking entities

Shadow banking entities can lead to increased risks for financial stability since they are entities involved in credit intermediation activities outside the regulated framework. For the time being, based on Article 394(2) of the CRR, the institutions had to report their 10 largest exposures to shadow banking entities on a consolidated basis but the CRR 3 has strengthened the current framework on exposures to shadow banking entities by introducing new supervisory reporting requirements, additional reporting requirements and new policy mandates. More precisely, on the supervisory reporting requirements, the CRR 3 introduced the requirement for institutions to report the information concerning their aggregate exposure to shadow banking entities. With regards to the level of details of the reporting of these information, the EBA considered the following two options.

Option 1a: Requesting institutions to report the aggregate exposure to shadow banking entities with a breakdown by country.

Option 1b: Requesting institutions to report only the aggregate exposure to shadow banking entities.

Requesting institutions to report the aggregate exposure to shadow banking entities with a breakdown by country of incorporation of the counterparty would provide stakeholders with additional and useful information on the geographical breakdown of shadow banking entities to which institutions are exposed and the related risks. This option may go beyond the regulatory requirements of Article 394(2) of the CRR 3 and the regulatory framework on shadow banking entities is going to be changed according to the CRR 3 (cf. Article 395(2a) of the CRR 3).

Based on the above, the Option 1b has been chosen as the preferred option and the Draft ITS will request institutions to report only the aggregate exposure to shadow banking entities.

2.2 Overview of questions for consultation

Question 1. Are the instructions and templates clear to the respondents?

Question 2. Do the respondents identify any discrepancies between these templates and instructions and the calculation of the requirements set out in the underlying regulation?

Question 3. Cost of compliance with the reporting requirements: Is or are there any element(s) of this proposal for new and amended reporting requirements that you expect to trigger a particularly high, or in your view disproportionate, effort or cost of compliance? If yes, please:

▪ specify which element(s) of the proposal trigger(s) that particularly high cost of compliance,

▪ explain the nature/source of the cost (i.e. explain what makes it costly to comply with this particular element of the proposal) and specify whether the cost arises as part of the implementation, or as part of the on-going compliance with the reporting requirements,

▪ offer suggestions on alternative ways to achieve the same/a similar result with lower cost of compliance for you.

Question 4. Is the deletion of rows in template C 47.00 of Leverage ratio reporting, related to cash pool arrangement, cost reducing to institutions?

2.2.1 Aggregate exposure to shadow banking entities (C 37.00)

Question 5. Is the design for the reporting of the aggregate exposure to shadow banking entities clear enough? If you identify any issues, please specify the related instructions.

2.2.2 IRRBB

Question 6. What are the views of respondents' on the current reporting templates? Do respondents see opportunities for simplification, and if so, how could such simplification be implemented in order to reduce reporting costs?

Question 7. Do respondents consider that removing certain columns, rows, or sheets (e.g. memorandum or currency breakdown) items would reduce reporting costs? Or, would it rather create additional costs due to the necessary reporting systems adjustments?

Question 8. Where do the respondents consider that the main costs stem from?

2.2.3 Reasons for resubmission

Question 9. Which one of the options described above for the future treatment of submission metadata would be the preferred one, in terms of reporting costs?

Question 10. Do you have any specific comment or suggestion regarding the specifications envisaged for the transmission of submission metadata?

2.2.4 Voluntary reporting by small and non-complex institutions (SNCIs) and by institutions other than large institutions

Question 11. Do you have any comments on the possibility introduced in the ITS, for SNCIs and for institutions other than large institutions to report on a voluntary basis and with the same frequency, as respectively non-SNCIs and large institutions? If so, please explain.

Consultation paper and Annexes |

[1] See the EBA XBRL Filing Rules version 5.7, pages 59-61: https://www.eba.europa.eu/sites/default/files/2025-11/152cf89c-5f72-465c-9c24-15327941c084/eba_filing_rules_v5.7_2025_11_24.pdf