-

Institution has paid out interim dividends and applied for inclusion of interim profits into the CET1. According to Article 26(2)(b) of the CRR, the institution has to demonstrate to the satisfaction of competent authority that any foreseeable charge or dividend has been deducted from the amount of those profits.

Article 2(2) of the Regulation (EU) 241/2014 states that: “Where an institution’s management body has formally taken a decision or proposed a decision to the institution’s relevant body regarding the amount of dividends to be distributed, this amount shall be deducted from the corresponding interim or year-end profits.”

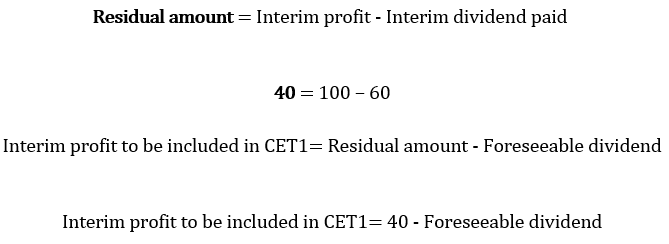

Article 2(3) of this Regulation states that: “Where interim dividends are paid, the residual amount of interim profit resulting from the calculation laid down in paragraph 2 which is to be added to Common Equity Tier 1 items shall be reduced, taking into account the rules laid down in paragraphs 2 and 4, by the amount of any foreseeable dividend which can be expected to be paid out from that residual interim profit with the final dividends for the full business year.”

Article 2(4) of this Regulation states that: “Before the management body has formally taken a decision or proposed a decision to the relevant body on the distribution of dividends, the amount of foreseeable dividends to be deducted by institutions from the interim or year-end profits shall equal the amount of interim or year-end profits multiplied by the dividend payout ratio.”

It is not clear from these Articles how exactly is the amount of interim profit to be included in Common Equity Tier 1 should be calculated.

Two calculations can be made in this context in our view:

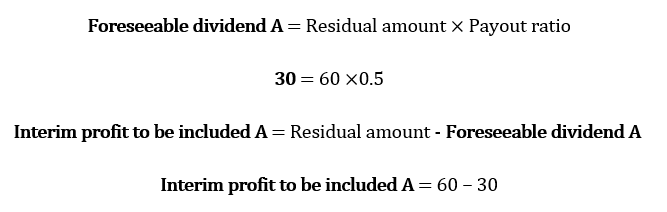

When an interim dividend is paid, the residual amount according to the Articles 2(2) and (3) of the Regulation (EU) 241/2014 (which is the maximum that theoretically can be included in CET1), is calculated as follows:

As a second step, according to the Article 2(3) of the Regulation (EU) 241/2014, the residual amount which is to be added to CET 1 items shall be reduced by the amount of any foreseeable dividend which can be expected to be paid out from that residual interim profit with the final dividends for the full business year. This will be calculated as follows:

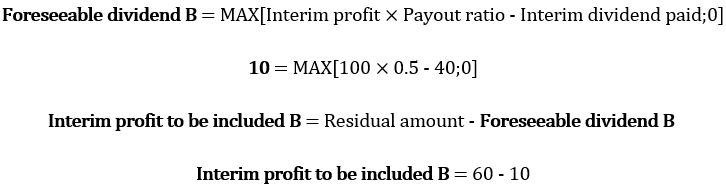

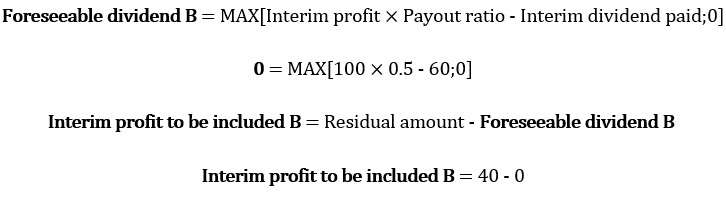

If no decision is formally taken or proposed by the institution on the final dividend (Article 2(2) of the Regulation (EU) 241/2014), foreseeable dividend is according to the Article 2(4) of the Regulation (EU) 241/2014 calculated as interim (or year-end) profits multiplied by the pay-out ratio. Taking into account, that the interim dividend was already paid, there are two possible interpretations as how to calculate a foreseeable dividend taking into account Article 2(4) of the Regulation (EU) 241/2014:

Option A:

Option B:

The two different formulas lead to two different outcomes regarding the amount of the interim profit to be included in CET1 capital.

Option A using “Foreseeable dividend A” (see previous formula):

Option B using “Foreseeable dividend B” (see previous formula):

The reasoning behind the two alternative formulas is the following.

Regulation (EU) 241/2014intends to allow the inclusion in the CET1 only of those interim profits that are net of all dividends that are paid or are foreseen to be paid out from that interim profit. In this perspective, the rules on interim dividends strike a balance between the possibility for the institution to pay out interim dividend in the course of the year and the necessity that the institution only includes a stable profit in the CET1 before the end of the financial year.

Since the board decision to distribute interim dividends cannot be considered as a “formal decision taken by the competent body” for the entire year, it is necessary to make a calculation that realistically estimates the foreseeable dividends that the institution is going to pay over the full year. Here, a correct interpretation of the Regulation (EU) 241/2014 is of major importance:

- Under Option A, the pay-out ratio for the year is applied to the residual amount (= interim profit – interim dividend) and this would result in ignoring in calculation of foreseeable dividend that some dividend has already been paid as an interim dividend and hence in a more conservative interpretation of the legal provisions. With this formula, the institution will most likely underestimate the interim profits to be included in CET1 and, at the end of the financial year, adjust upwards its CET1.

Under Option B, the pay-out ratio for the year is applied to the profits made so far. Overall, the formula allows institutions to reflect in the estimation of the foreseeable dividend the interim dividends distributed, and hence to better reflect the situation of those institutions whose profitability over the year remains as expected.

As it may be seen, the options can produce a very different effect depending on the individual cases and it is important to provide a guidance on the interpretation of the formula to promote the most correct behaviour by institutions.

Illustrative example 1: Interim dividend paid < Pay-out ratio

Interim profit: 100Interim Dividend Paid: 40

Payout ratio: 50%

Foreseeable dividend:??

Interim profit to be included into CET1:??

Option A:

Foreseeable dividend A: 30

Interim profit to be included into CET1 A: 30

Option B:

Foreseeable dividend B: 10

Interim profit to be included into CET1 B: 50

Illustrative example 2: Interim dividend paid > pay-out ratio

Interim profit: 100Interim Dividend Paid: 60

Payout ratio: 50%

Foreseeable dividend:??

Interim profit to be included into CET1:??

Option A:

Foreseeable dividend A: 20

Interim profit to be included into CET1 A: 20

Option B:

Foreseeable dividend B: 0

Interim profit to be included into CET1 B: 40

Which of the two calculations is correct, A or B?

Disclaimer

The Q&A refers to the provisions in force on the day of their publication. The EBA does not systematically review published Q&As following the amendment of legislative acts. Users of the Q&A tool should therefore check the date of publication of the Q&A and whether the provisions referred to in the answer remain the same.